by Chris Becker

A great lead from overnight markets generally turned the risk taps on here in Asia today, but the Yen strengthened against USD providing a headwind for Japanese stocks. Commodities were generally higher with the WTI oil price again dicing with the $54USD per barrel level as we head into another week of OPEC meetings.

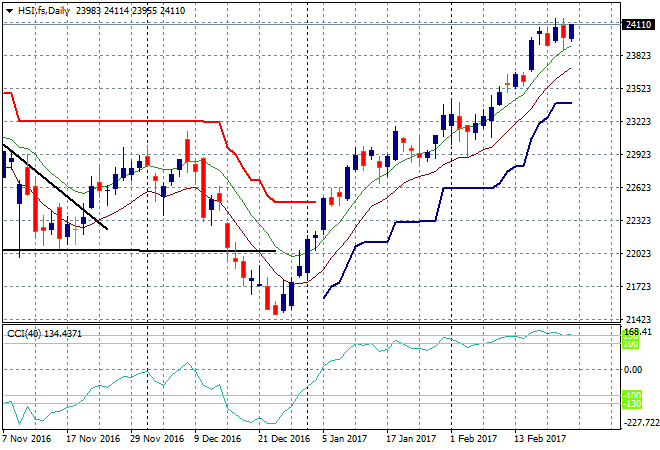

The Shanghai Composite is dead flat just after the lunch break, currently at 3250 points, trying to build on its recent pullback. The Hang Seng Index is doing much better, up 0.8% to be at 24172 points in response to positive domestic news about GDP growth:

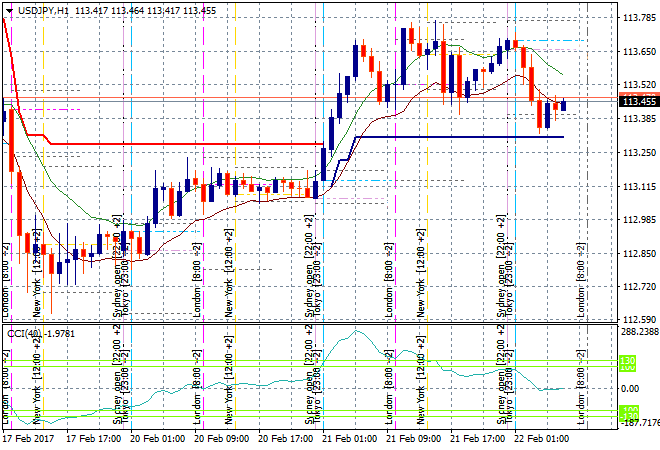

Japanese stocks are also flat today, again because of the inverse correlation with Yen, which has strengthened and taken back its losses against USD. The Nikkei therefore closed down a few points to finish at 19373 points in a muted session. The hourly chart for USDJPY shows how price has been unable to breach the 113.80 level with Yen bid up throughout the Asian session, pulling back to ATR support at 113.30 or so:

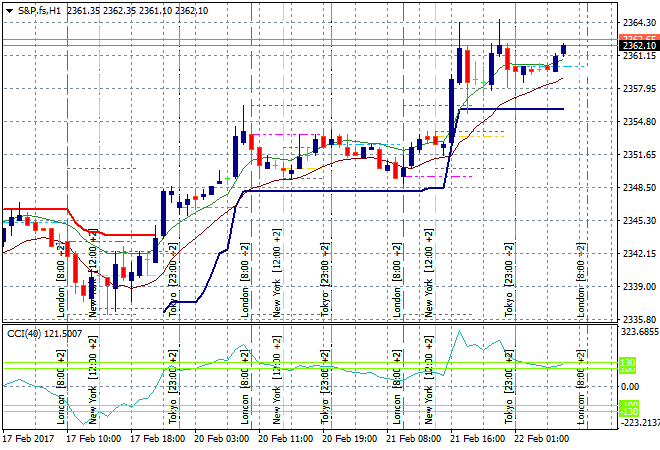

S&P futures are building in anticipation of more positive news tonight with the FOMC minutes to be released later:

The ASX200 was going nowhere until a series of solid earnings reports came out with a small surge before lunch holding on throughout the session. The market closed up 0.2% to be just above the crucial 5800 point resistance zone. Woolworths was one of the better performers, up 4.5% on its earnings report today as sales were better than expected.

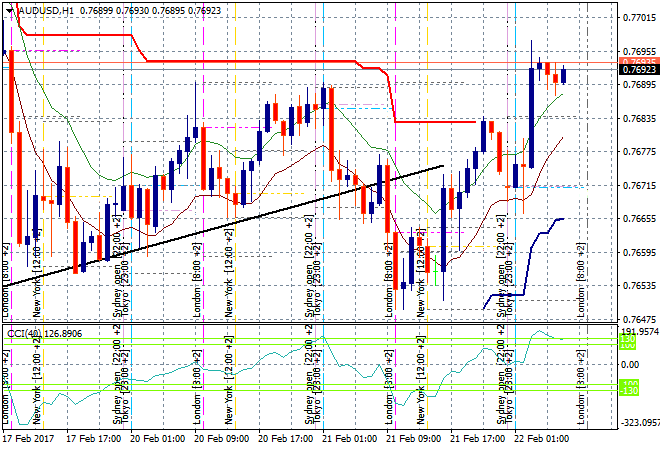

The Aussie dollar was hesistant at first out the gate but built on last night’s reversal, heading back up to but not abov the 77 handle against a seemingly stronger USD. This puts it back on trend, but I’m wary at following this going into the release of the Fed minutes tonight:

The data calendar tonight ramps up with the UK 4Q GDP print, then January CPI print for the EZ with the FOMC minutes early in the morning the big one to watch out for.