by Chris Becker

A strengthening USD is the main highlight during a muted session in Asia today, with the release of the RBA minutes locally the only major catalyst on the calendar. Commodities were generally higher with iron ore up nearly 4%, gold slipping slightly while oil still wants to break free as the WTI contract dices with the $54USD per barrel level again.

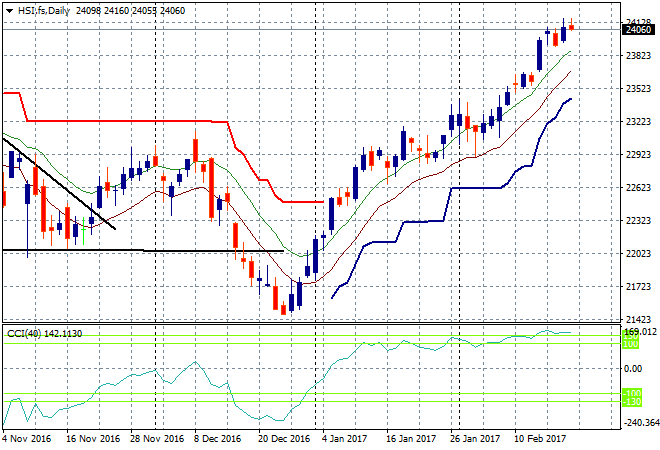

The Shanghai Composite is up slightly after the lunch break to be at 3247 points, still building once more after its recent pullback. The Hang Seng Index is in reverse however, down 0.3% as its rally begins to run out of puff, sligding back to be just above 24000 points:

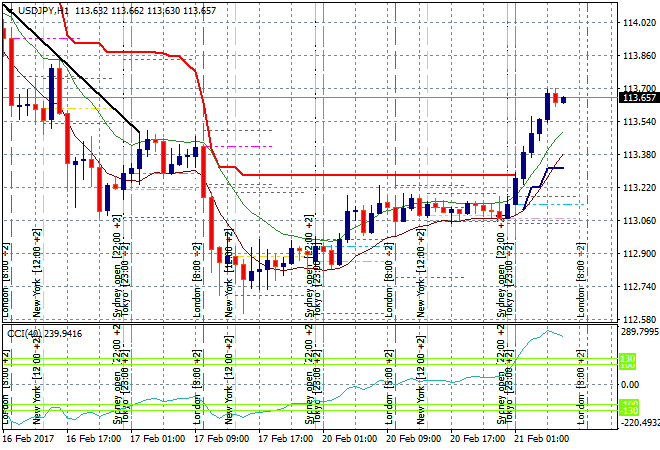

Japanese stocks are the outperformers today, all because of a significantly weaker Yen against USD. The Nikkei closed up 0.7% higher to finish at 19392 points in a solid session. The hourly chart for USDJPY shows how ATR resistance at the 113.35 zone has been swept aside in a rally since the Tokyo open that has run out of puff here at 113.70, in reaction to some solid domestic data. This seems too far too fast according to my preferred momentum indicator, so watch for a pullback:

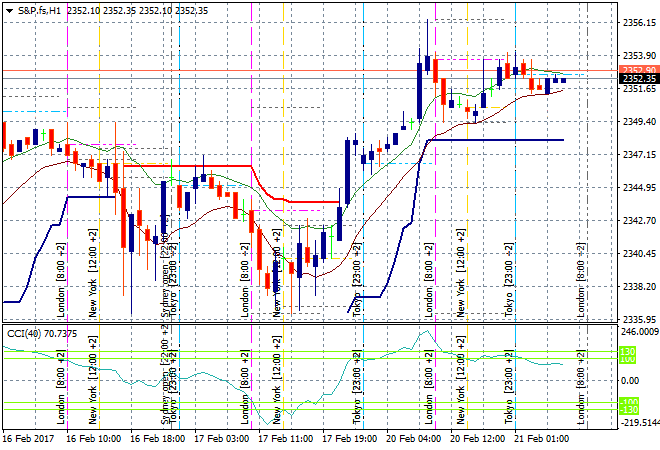

S&P futures are steady in anticipation of the reopening of US markets following the long weekend. There shouldn’t be much to shake it up tonight saving BOE Governor Mark Carney’s speech to the UK parliament:

The ASX200 eked out a poor scratch session again, closing below the closely watched 5800 point level as earnings reports continued to weigh. It was Monaldephous time to shine, the mining services contractor launching nearly 12% on a sliding earnings report but one that contained a “positive outlook”. Worleyparsons continued to tumble though, down another 5% today.

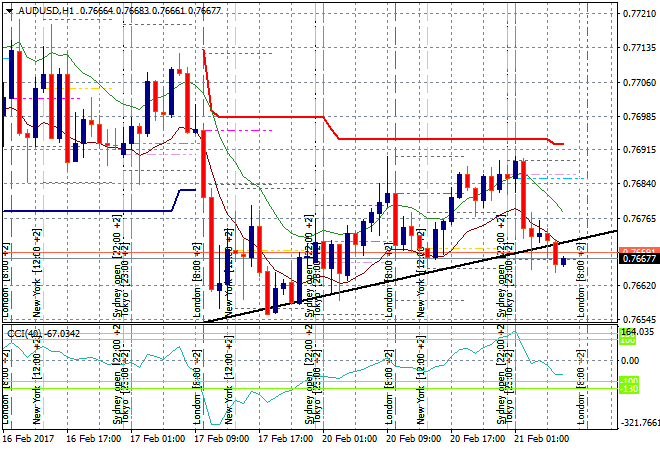

The Aussie dollar couldn’t face the strong USD today and fell immediately on release of the RBA minutes, heading below its daily uptrend line and yesterday’s intraday low. As we head into the London session, the area to watch is 76.50 for signs of a breakdown:

The data calendar is again relatively quiet tonight, apart from Mark Carney’s speech to UK parliament and a brace of US preliminary PMI data.