by Chris Becker

The sudden resignation of US National Security Advisor Michael Flynn has pushed the USD down, combined with the higher than expected Chinese CPI print with Asian markets slipping as confidence faltered over the dual macro impact. Locally the surprisingly good NAB business conditions survey combined with the lower USD sent the Aussie dollar higher but the correlation with other bourses kept local stocks from advancing.

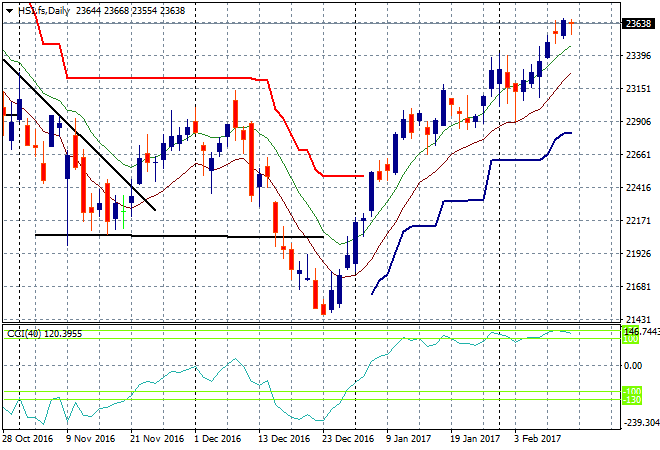

The Shanghai Composite is down a little over 0.3% to be just above 3200 points, holding on to its recent breakout. The Hang Seng Index is dead flat which is a good thing given how overbought the market has been in recent sessions, so a pullback to 23400 or so is likely here:

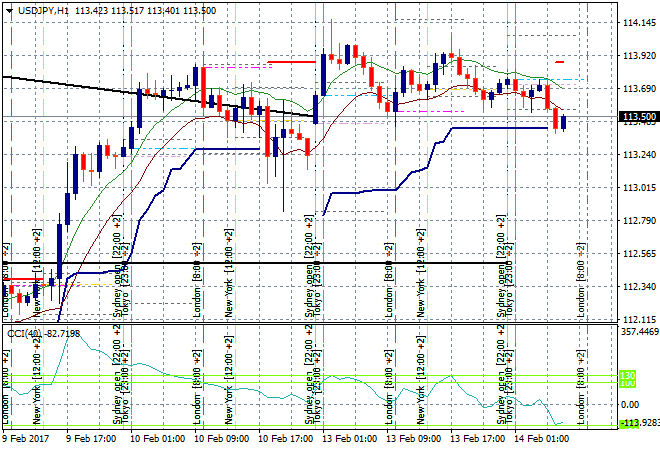

Japanese stocks are off as the falling USD means a higher Yen, bad news for the inversely correlated market with the Nikkei falling half a percent to be at 19355 points. The hourly chart for USDJPY shows how the 114 handle is proving too heavy a resistance level and this latest macro impact is seeing Yen bid and the pair fall below ATR support, but not yet below the downtrend line of the daily highs:

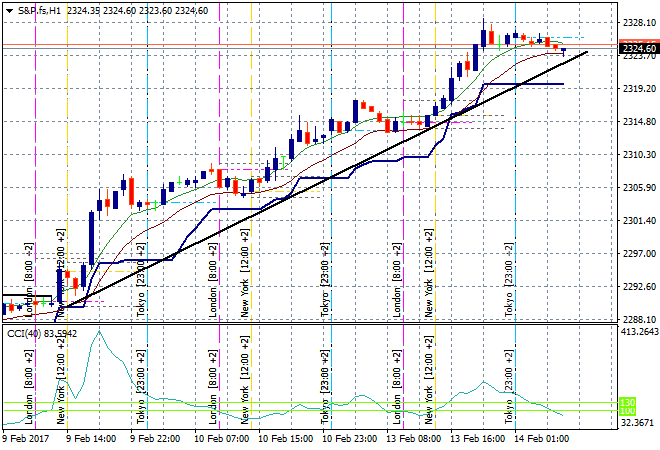

S&P futures have come back a little from their exuberant highs but we’ll have to wait and see how London reacts to this news first- watch that trendline very closely!

The ASX200 jumped out of the gates, up almost 40 points or 0.6% at the open as the NAB print buoyed concerns over a bank inquiry but this lead was sold off all day on the higher Aussie dollar and lack of risk taking in other Asian bourses. The market eventually closed a few points down at 5755.

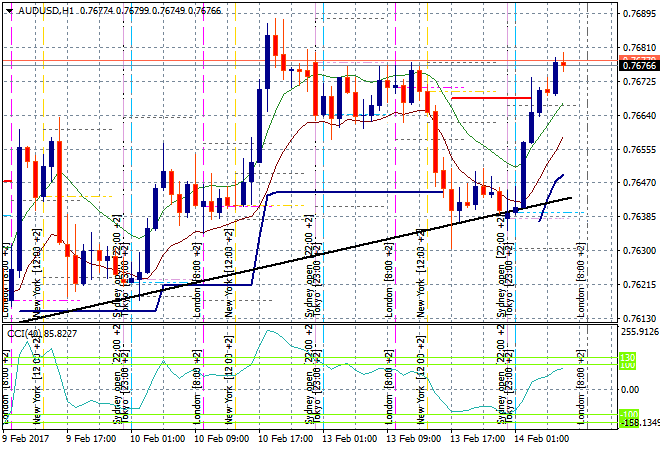

The Aussie dollar surged higher from the Sydney open on the resignation news, the Chinese CPI and the NAB print, heading straight up to but not above the Friday high at the 76.80 level. This looks somewhat overdone but I’m watching this area closely, particularly if the USD buyers come back strongly later tonight:

The data calendar tonight includes preliminary 4Q GDP data for the EZ, Germany and Italy, the January CPI print for the UK and the very closely watched German ZEW business survey. In the ‘States its Janet Yellen to appear before the Senate Banking panel for what will probably be a soft affair.