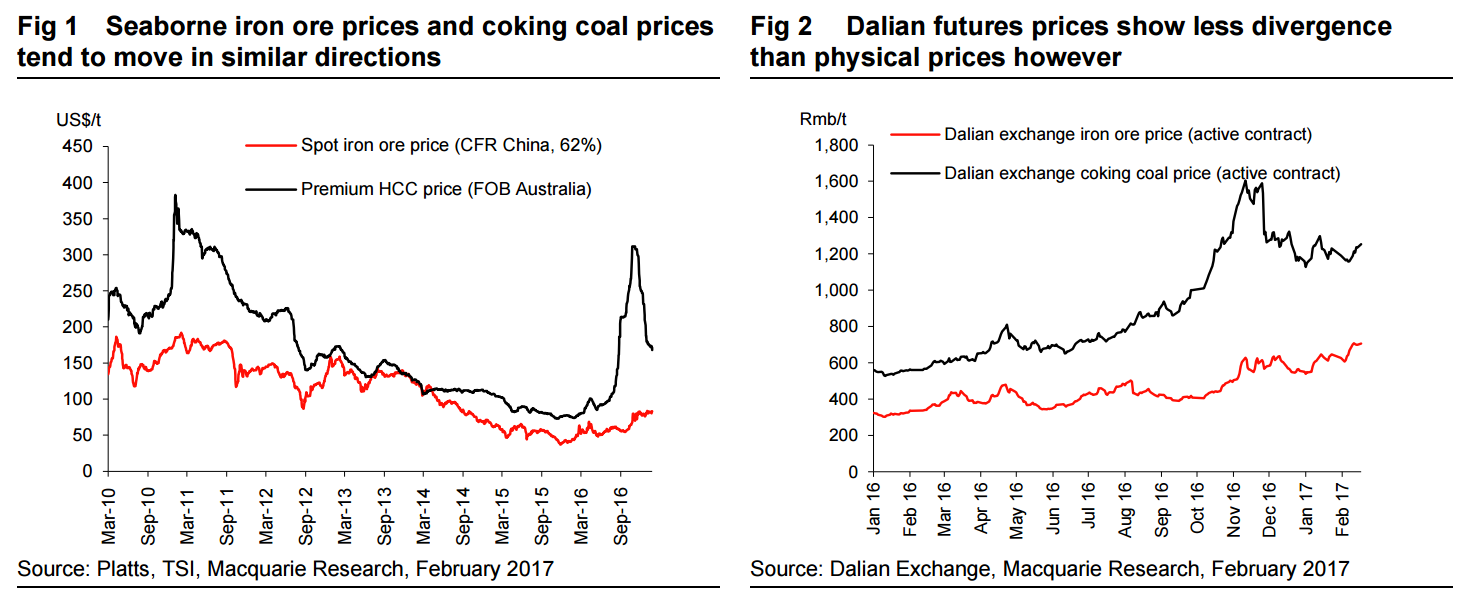

Iron ore and coking coal prices have shown much divergence in their spot physical prices in recent weeks. Year to date spot 62% Fe iron ore prices are up over 16%, while spot premium coking coal prices are down by over 32%. Given that both are almost exclusively used for steel making, then barring any major supply shocks to differentiate their markets, it should be expected that prices for both would move in similar directions. The key question to understand with these differentiated price moves then is whether one is more representative of the real fundamentals for steelmaking and thus should lead the other, or whether supply differences justify prices moving in such different directions in a sustainable manner.

Historically while prices for both major steelmaking raw materials have tended to move together, there have been periods of disconnect in prices, notably June-September 2011 (iron ore +7%, coking coal -15%), May-July 2012 (Iron ore flat, coking coal -18%) and October-December 2013 (iron ore +7%, coking coal -10%).

Interestingly in the month following the above time periods of price divergence, coking coal was proven to be the price leader, with iron ore falling sharply to catch up. Iron ore spot prices fell by 30% in October 2011, 23% in August 2013, and 9% in January 2014, though of course once prices began falling at the start of 2014 they continued to decline for the whole year, falling 47% over the year.

One key reason for the differentiated prices could come from each commodities’ different degree of reliance on China as the physical price setter. For iron ore China imports 1bn tonnes in a global 1.4bn tonne a year market, while for coking coal China only imports 50mt in a 280mt market. Indeed looking at Dalian futures prices, there has been less of a degree of disconnect in prices between the two in recent months, in part because Chinese coking coal prices never reached the high levels seen on the seaborne market, and so their decline has been less pronounced.

Of course it could be argued that the price moves that we have seen recently in coking coal are essentially a return to a more reasonable price range after being extremely elevated due to supply disruptions in 2H16. However while prices have been falling on rising supply, we would also argue that iron ore supply shows even more abundance than for coking coal.

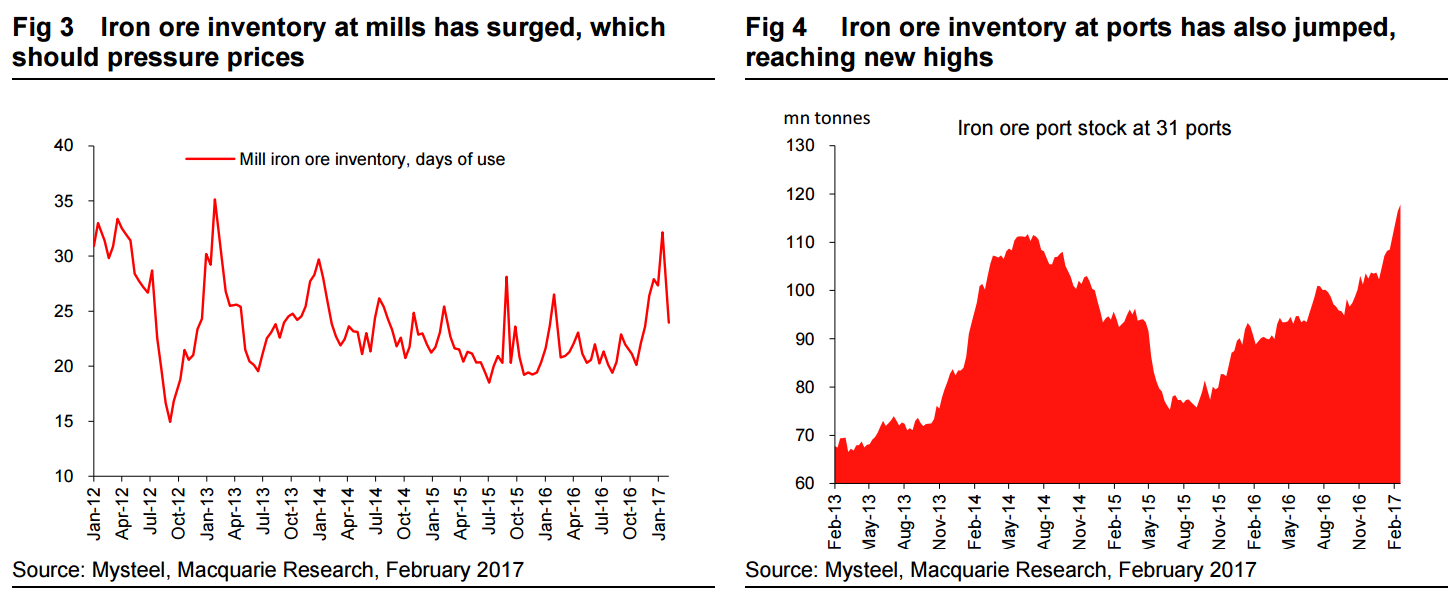

As we have written many times in recent weeks (here), the fundamentals for iron ore do not appear at all supportive of higher prices. Supply has increased sharply from both seaborne and domestic marginal mines in response to the price recovery seen over 2016, and this is most clearly evidenced by the surge in iron ore inventory at both mills and ports. Indeed the latest iron ore inventory data from Mysteel shows iron ore stocks at 45 major Chinese ports has increased to a record high of nearly 130mt, up 15mt in the seven weeks since the start of 2017 alone.

In addition to weakness in coking coal prices, other steelmaking ingredients such as manganese ore and scrap have also shown much weakness in recent months (here). Manganese ore prices have tumbled nearly 50% since the end of last year, from $9.10/mtu in December to only $4.60/mtu according to the latest Platts price assessment for 44%Mn grade ore, CFR China.

In our view supply of most steel making raw materials has become abundant in response to higher prices, but this has not stopped seaborne physical iron ore prices from showing clear divergence to other steel making ingredients since the New Year. We do not think such differences will last however.

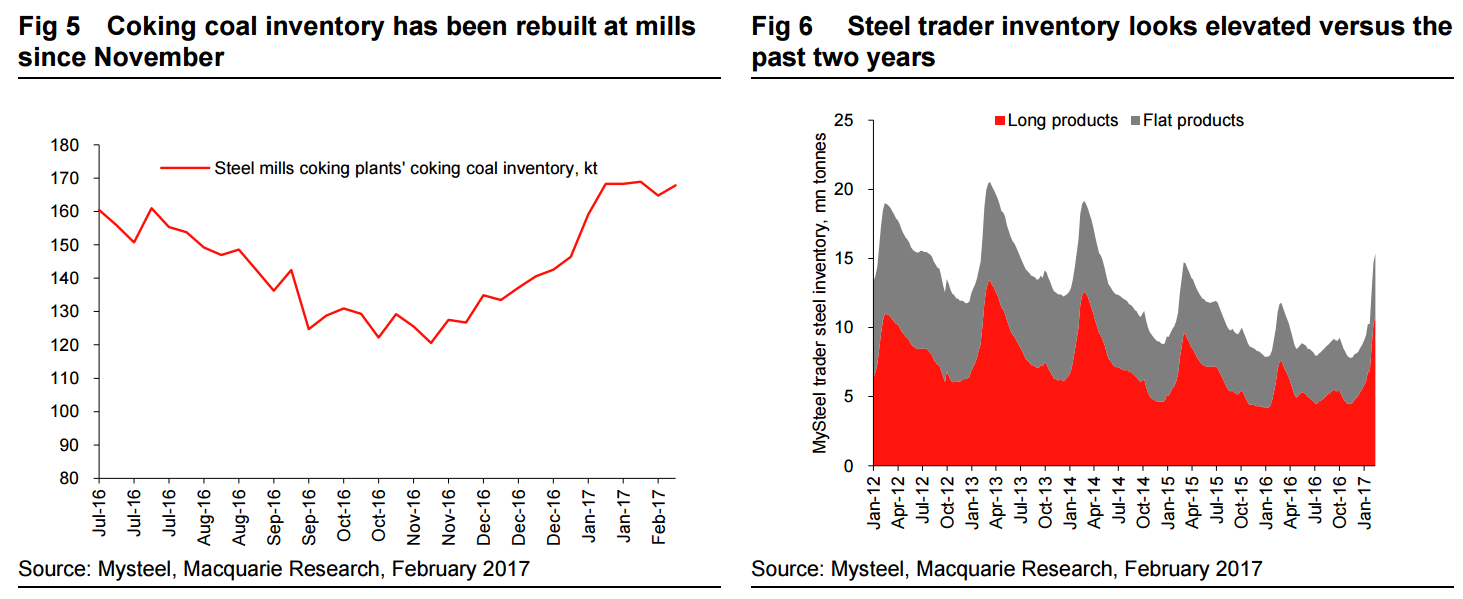

Indeed if anything we’d expect coking coal prices to see more active buying in March as fears should return to steel mills of potential supply restrictions coming back into force as the 276 days coal policy is likely to be reapplied in some form in March (here). Given how steel mills were caught short last year by the coal output restrictions, we would imagine they would look to be more cautious and build more inventory ahead of the return of any restrictions. While there is no clarity yet on how the 276 days restrictions may be reapplied, a meeting is scheduled between the coal association and major miners on 21st February, after which the coal association will submit proposals to the NDRC for further supply side reform and potential mechanisms to reapply the 276 days policy.

Iron ore prices meanwhile appear to be holding up not on any fundamental support, but have been pushed up to elevated levels purely on extremely bullish sentiment among Chinese market players towards the outlook for steel demand and prices into the traditionally strong spring construction season. While we expect Chinese steel demand to be solid (here) through 1H17 on carry through effects from last year’s infrastructure stimulus and the broad based demand traction seen over 2H16, we are fearful that steel mills and traders’ expectations for demand are now too elevated. With inventory levels high for both steel and iron ore, it is only a matter of time in our view before confidence in demand meeting elevated expectations starts to wane, and mills go into a destocking cycle for iron ore. With iron ore supply in abundance, we’d therefore expect prices to fall sharply towards a more fundamentally supported $60/t level, essentially repeating the price cycles seen in iron ore and coking coal over 2011, 2012 and 2013 as mentioned earlier.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.