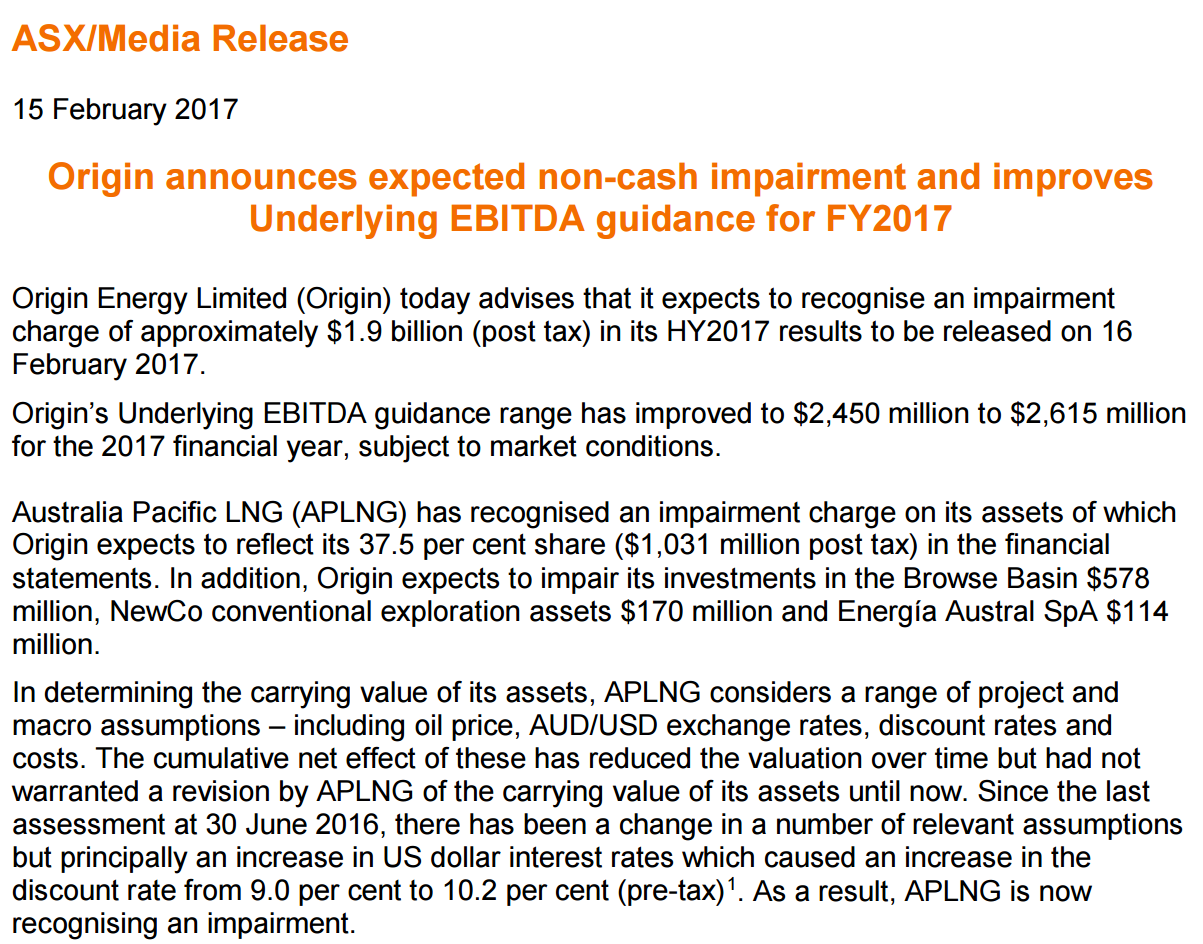

From ORG today:

I’ve lost track of how much value is gone now. But, given the plants are worthless you can be sure that there’s more ahead. Of course, as the asset’s value keeps falling, so the debt load keeps rising, and so the pain spreads, via Credit Suisse:

■ Lawrie Tremaine to join as CFO As somewhat of a surprise to us, Origin has announced the appointment of Lawrie Tremaine as CFO upon serving out his notice at Woodside. Lawrie has run an extremely prudent, even conservative, balance sheet at Woodside and is without doubt a highly capable CFO. Perhaps the decision to move raises as many questions about Woodside as it does Origin, but there are certainly a few for Origin.

■ If the past is a guide this is not a CFO that will like the balance sheet It is not remotely lost on us that Lawrie is a CFO who decided in February 2016 to fully underwrite Woodside’s dividend to protect its balance sheet. At this stage Woodside’s net debt was <25% of its market cap and gearing was 23%. He joins Origin where net debt is currently ~100% of market cap and a tightrope is being walked on an investment grade credit rating. Whilst we entirely support the strategic decision to get rid of the conventional oil business it might only reduce debt by ~A$1bn and it loses $400mn+ of near-term EBITDA. We struggle to see how a conservative CFO like Lawrie would not want to see a stronger capital structure, with equity the obvious solution. As a CFO, your balance sheet is your reputation.

■ Interesting to hire an E&P guy when selling conventional E&P Whilst again we believe that this is a strong, senior hire as CFO, choosing someone from the E&P sector is interesting when the conventional E&P business is set to leave the portfolio. Whilst Origin is currently not putting Ironbark and Poseidon in the NewCo structure, both of which are conceptually feed gas for LNG projects, we sincerely hope this is not an indication it is going to up exposure again in LNG. Origin is not the logical owner of either of those assets in our minds, nor is that the kind of risk that new Origin should take.

■ Time to pull the trigger We by no means see raising equity as negative for Origin. To be frank (excuse the pun), we think Origin is a more investable business, for a wider range of investors, when the debt issue is taken off the table. We look forward to getting a bit more clarity on some of these points at results on Thursday, 16 February.

Downgraded to “underperform”. No shit!