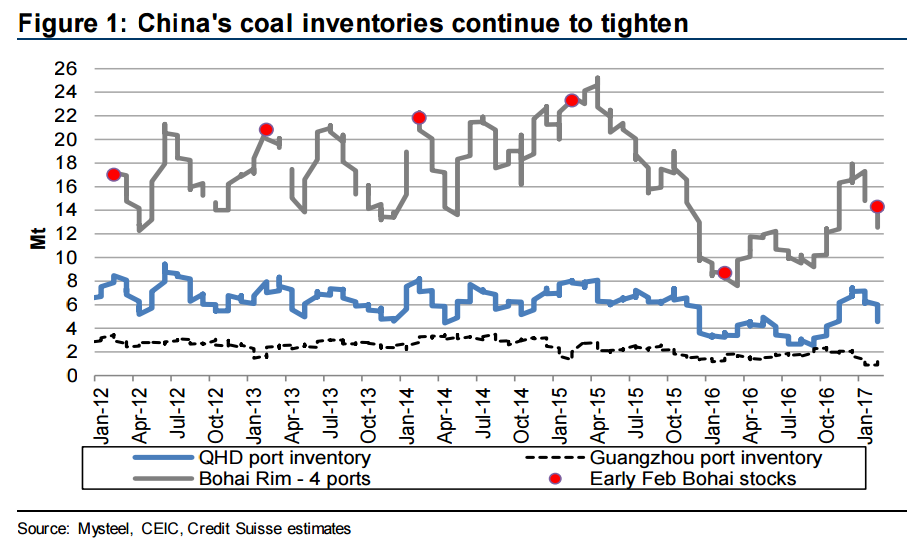

■ Newswires are alive with stories that China will reintroduce the 276 work day for coal mines from mid-March to mid-Sep, although it is yet to be confirmed by the NDRC. This despite the QHD coal price of Rmb590/t lying above the Rmb500-570/t target range, and China’s coal inventories continuing to shrink, tightening the market (figure 1).

■ Partial 276 policy. McCloskey provided details that it attributed to a source in the NDRC. Rather than the blanket 276 work-days implemented last year, this time the Government is crafting a partial policy—276 work days for all except a group of high-yielding mines, and also for regions that are particularly tight. Presumably China hopes that continuing 330 days at high volume mines will allow coal stocks to rebuild in the 2Q shoulder season, allowing the price to subside into its target range. Figure 1: China’s coal inventories continue to tighten Source: Mysteel, CEIC, Credit Suisse estimates

■ NDRC’s target range of Rmb500-570/t QHD equates to $70-$80/t Newcastle 6000kcal on an equivalent basis. The NDRC’s intent remains to hold the China coal price at a level that makes coal mines profitable without driving the need for power price rises. It is not intended to lift imports, but seaborne thermal prices should be supported by arbitrage.

■ Double benefit for met coal—276 work days plus North Korea ban: High-yielding mines that continue at 330 work days are unlikely to include coking coal, so met should feel the full impact of the work day reduction just as demand lifts for steel output in construction season. Prices should climb and seaborne coking coal’s $40/t discount compared to Shanxi should wither. In addition, China has suspended coal imports from North Korea for the year. North Korea delivered 22.5Mt of anthracite in 2016, used in China as PCI. Spot PCI linkages against HCC should strengthen.

I see no upside for China in this. Why wreck its terms of trade for no reason? Nor does it appear that the North Korean ban is as complete as this analysis suggests. At $80, seaborne coal can flood into China so I don’t see that holding, either.

Chinese coal stocks have run down a fair way, correcting prices, so we’ll see some more buying ahead. That will delay any iron ore correction while it transpires. But it is also a warning of what will happen when that restocking turns.

My own outlook is unchanged for an ongoing steady fall back to $120 for coking coal and $60 for thermal by year end.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.