By Gareth Aird, senior economist at CBA:

Key Points:

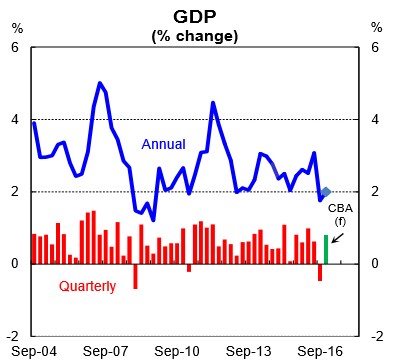

- We expect QIV GDP growth to print at 0.7%.

- Annual growth, revisions aside, should stand at 1.9%.

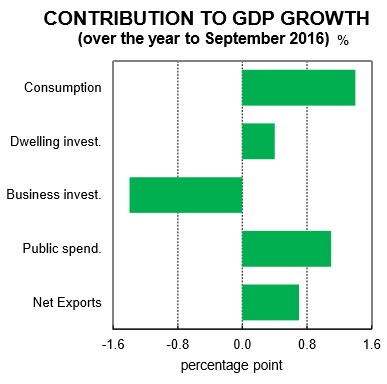

- Household consumption, dwelling investment, public spending and net exports will make positive contributions to growth.

- Business investment and inventories will make negative contributions to growth.

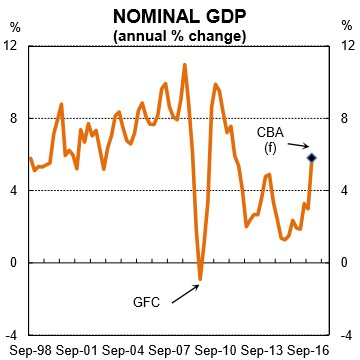

- We expect nominal GDP to lift by a sizeable 3.0% due to significantly higher export prices.

The run of major 2016 data releases comes to a close with the national accounts on Wednesday. Based on the economic information to date, we expect QIV GDP growth to print at 0.7%. If correct, the figures will show that the QIII weather related contraction in output was a temporary aberration. Our forecasts have annual growth lifting a little to 1.9%. The high probability of an upward revision to QIII means that the risk to our QIV q/q call is to the downside.

Over the past few years, the main contributions to GDP growth have come from household consumption, net exports and dwelling investment. Conversely, business investment has been a drag on growth. Most of these themes will be evident again in the QIV data. More specifically, the data is likely to show:

- a moderate increase in household consumption, supported by accommodative monetary policy, modest employment growth and discounting in the retail space;

- a lift in residential construction after the QIII weather-related fall;

- a positive contribution to growth from public investment and farm output;

- a decline in business investment driven by a fall in mining-related engineering construction partially offset by a lift in non-mining capex;

- a small positive contribution to growth from net exports following a decent rise in export volumes and more modest lift in imports.

Nominal GDP is set to post a solid lift in QIV as the fruits of rising commodity prices are reflected in higher income growth. We have forecast a quarterly increase of 3.0% which would take annual growth to its strongest pace in five years. The rise in commodity prices is also providing a boost to the public coffers courtesy of higher company tax receipts and a lift in royalties. The income spike, however, is yet to filter through to employee earnings. We suspect that it will take a few more quarters of firmer commodity prices for the benefits to spill-over to the household sector in the form of higher salaries.

Real Gross Domestic Income (GDI), which measures the purchasing power of the total incomes generated by domestic production, will grow by more than output in the quarter because of the increase in the terms of trade.

Real GDP in line with our call over QIV would be consistent with the latest RBA forecasts (published in the February SoMP). It would also be consistent with monetary policy on hold.