From Bartho yesterday:

A central criticism of the surge in LNG exports as a consequence of more than $US200 billion of investment in new export plants in recent years, including the $US75bn or so invested in the three coal seam gas-to-LNG plants at Gladstone in Queensland, is that it has driven up domestic gas prices and dried up domestic supply even as global LNG prices have plummeted.

The worst-case-scenario that critics of the plants, and proponents of domestic gas reservation policies, have outlined is that they undermine the economics of local industry while pumping the gas into increasingly oversupplied offshore markets. That thesis is supported by the initial entry, and future potential, of the US into the markets for LNG.

Shell, after its $90bn acquisition of BG Group, is now one of the key players in the LNG sector. It published a quite upbeat assessment of the state and outlook for the market overnight.

Contrary to a lot of the gloomier expectations, it says the global market for LNG was balanced in 2016 despite a big increase in new supply dominated by Australian producers, who added about 15 million tonnes of supply to their pre-existing volumes of just under 30 million tonnes.

The increased supply — about a third of the new capacity that is in the pipeline — was, however, absorbed by greater-than-anticipated increases in demand from Asia and the Middle East and the emergence of new importing markets: Colombia, Egypt, Jamaica, Jordan, Pakistan and Poland.

Shell is bullish about the outlook, forecasting a continuing growth in demand. By 2020, it says, the size of the global trade in LNG will have grown by about 50 per cent compared with the volumes in 2014. Global demand for gas will grow at about two per cent a year between 2015 and 2030 but LNG demand is projected to grow at between four per cent and five per cent.

While the market will have to absorb the rest of the investment bulge that occurred before the oil price — and new investment in future production by the oil and gas industry — crashed in mid-2014, it believes more investment will be needed to meet the growth in demand it sees post-2020, most of it from Asia.

…Whether or not there is another big wave of LNG investment in Australia might depend on the current Federal Government review of the Petroleum Resource Rent Tax. Proceeds from the PRRT have fallen dramatically as a result of the combination of the collapse in oil prices and the profits-based tax that applies, or doesn’t, during the start-up phase of new projects.

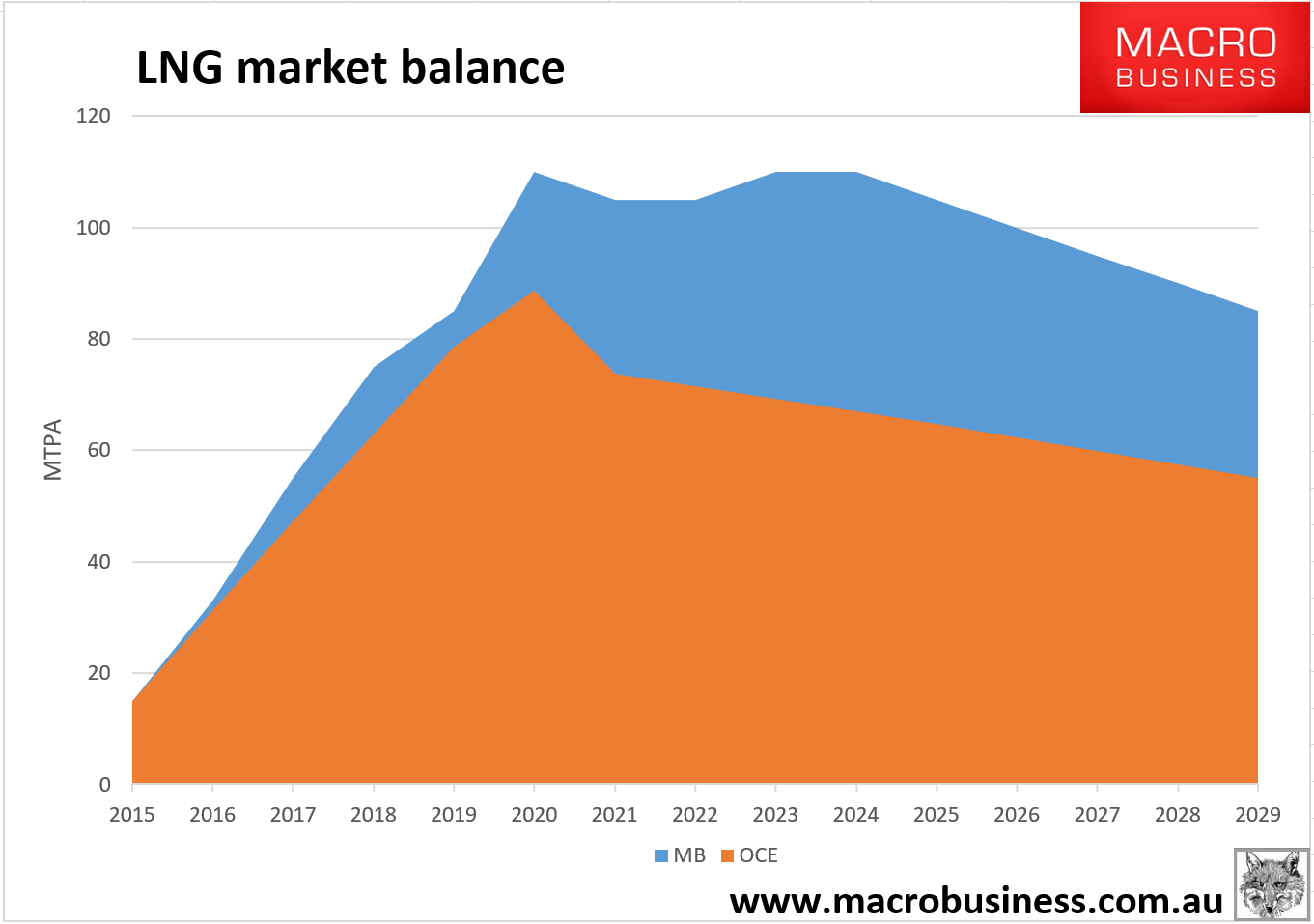

In a word: rubbish. Shell’s demand outlook is exactly the same as the Office of the Chief Economist:

On a straight market balance chart it looks like this:

It is an endless and monstrous glut. My own outlook is worse because I see Japanese demand falling faster, China using more piped gas from Russia and India fading as the rising new customer. But even using the Shell and the OCE outlook there is no motive to develop more Aussie gas for another decade at least and when it does come it will begin with value adding to brown fields and an additional train at Gorgon not any new plants in the east.

No, Australia either extracts value now or the gas currently being produced is being thrown away.

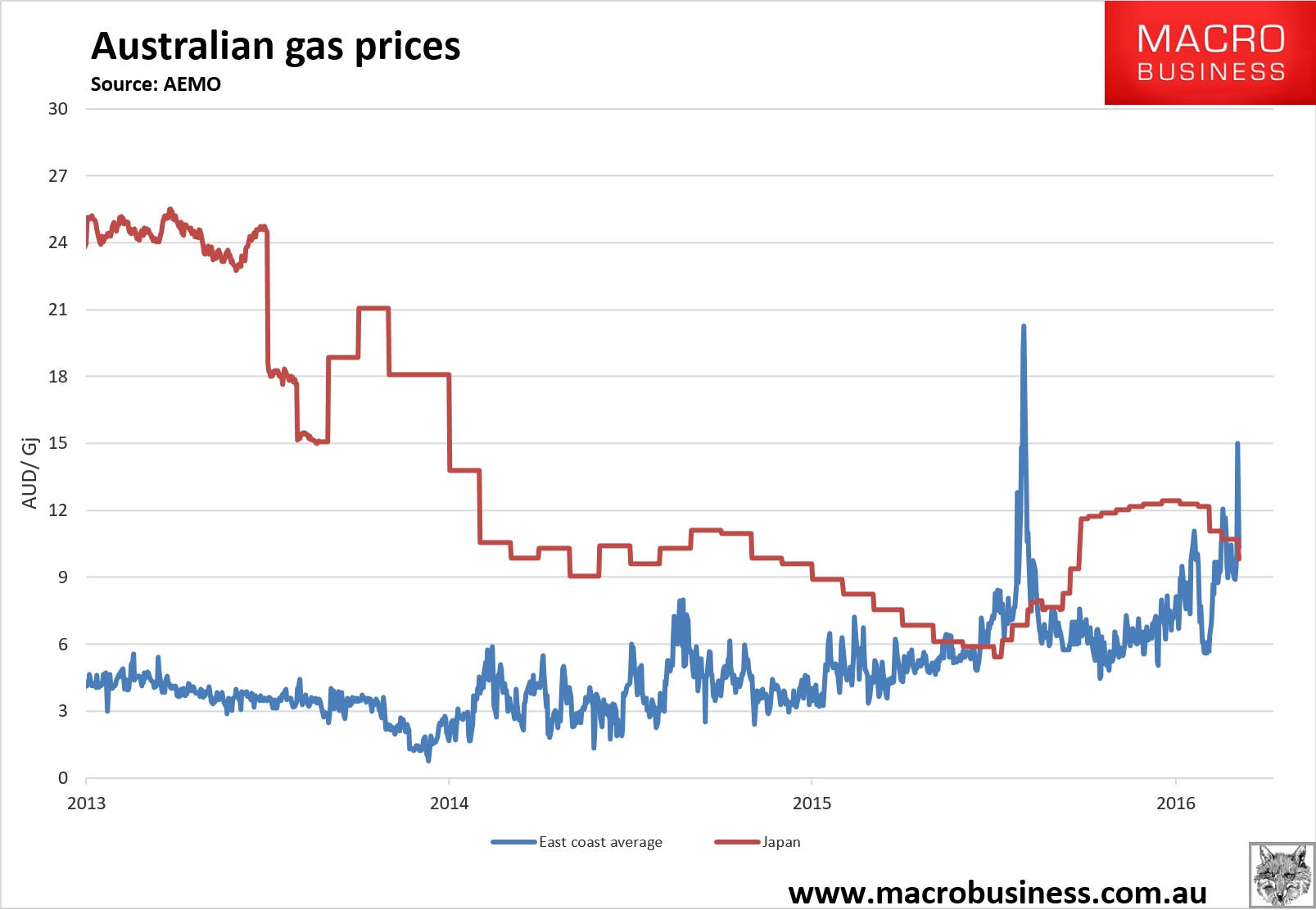

Shell is simply playing for time and aiming to shoot down the PRRT tax review. Moreover, it is currently squatting on the Arrow leases in QLD, which constitute 17% of east coast gas reserves, as it gouges the local market to its heart’s content resulting in us paying more for our own gas than the Japanese:

To resolve this price gouge, the federal and state governments could apply “use it or lose it” policy to terrestrial leases with tight deadlines. This is hardly controversial. The same rules already apply in maritime gas though they poorly designed and easily gamed, as Woodside has recently done with Browse. Coupled with domestic reservation this would introduce a new gas player to the market and develop Arrow for domestic distribution quick smart.

My own view remains that one more player won’t be enough so I’d rather see the government take back the lease if Shell won’t develop it for local use. A public player operating on mandated rates of return would benchmark prices for everyone and end this mess.