From Westpac’s Elliot Clarke:

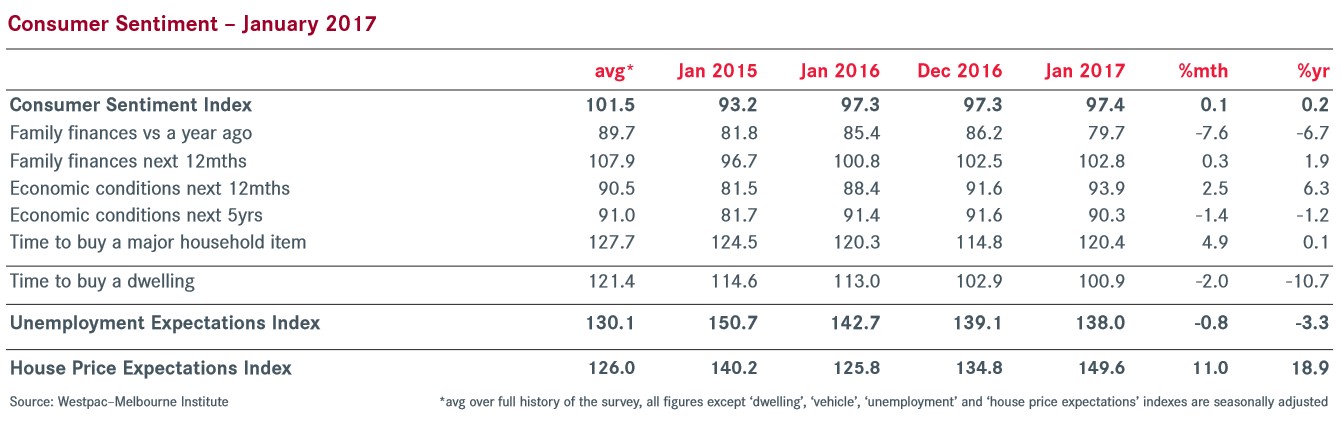

The Westpac Melbourne Institute Index of Consumer Sentiment rose by just 0.1% in January, from 97.3 in December to 97.4.

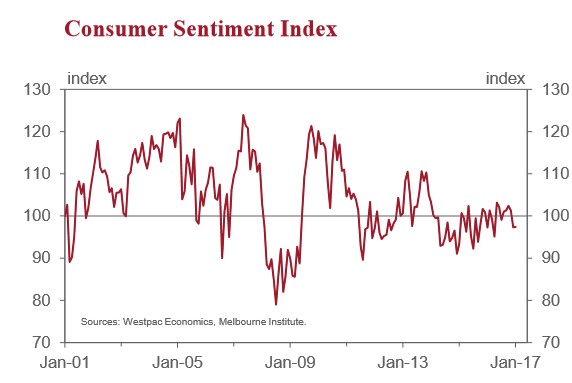

Following December’s 3.9% decline, Sentiment was little changed in January, rising just 0.1%. At 97.4, pessimists clearly outnumbered optimists for a second consecutive month in January (100 being the neutral point).

December and January are the weakest outcomes since April 2016, when the Index printed at 95.1. During the intervening seven months, the Index has averaged 101.5, aided by interest rate cuts from the RBA and, in May, a more favourable Federal Budget”.

The absence of a rebound in January is a disappointing result, particularly when one factors in the cumulative 10% gain for Australian equities over the past two months and, to a lesser extent, a nascent improvement in the pace of job creation.

On the other hand, there are likely to be lingering effects from the shock of the announcement just before the December survey that the economy contracted by 0.5%.

The components of the headline Index were volatile in January. ‘Economic conditions, next 12 months’ experienced a partial rebound from December’s 5.2% fall, rising 2.5%. However, longerterm expectations deteriorated further, the ‘economic conditions, next five years’ sub-component falling a further 1.4% in January following the 2.5% fall in December. From their respective post-Budget peaks in May 2016, the short and long-term economic conditions sub-components are down almost 8% and 10% respectively.

Views on family finances are also mixed. ‘Family finances relative to a year ago’ deteriorated materially. Having fallen 2% in December and a further 7.6% in January, this sub-component is now down 16% from its 2016 peak, seen in February. ‘Expectations of family finances over the next 12 months’ lifted by 0.3% in January. They have remained far more constructive than the backward looking perceptions, with this component down by ‘only’ 3.7% from its 2016 peak, seen in August.

Despite the marked deterioration in current perceptions of family finances, the ‘time to buy major household items’ sub-component has also held up well. A 4.9% rebound in January followed December’s 7% decline. At 120.4, this sub-component is only marginally below its post-Budget average of 122.3.

In line with the improved tone of the labour force survey, the Westpac Melbourne Institute Unemployment Expectations Index edged another 0.8% lower in January. Remember a decline in the Index indicates consumers hold a more favourable view of the labour market. Unemployment expectations have now fallen by 6% since their 2016 high in March and by nearly 12% since their most recent peak, September 2015. That said, the Index still remains above its long-run average, signalling a lingering degree of apprehension over job prospects.

Turning then to the housing market, the ‘time to buy a dwelling’ index fell 2% in January to be back near its most recent low of November 2016. But that still leaves the index around 6% above its 2016 low, reached in April. At its current level, this measure sits some 16% below its historic average.

That being said, the Westpac Melbourne Institute Index of House Price Expectations surged again in January to 149.6, its highest reading since April 2015 (152.1). NSW again led the charge in January. However, material gains were seen in house price expectations across the nation. For all states except WA, price expectations are above their respective long-run averages.

The Reserve Bank Board next meets on February 7. We expect the Board will decide to keep rates on hold. While the 0.5% contraction in the Australian economy in the September quarter would have come as a surprise and that result has undoubtedly had a lasting impact on Consumer Sentiment, we expect the Board will be more confident about the economic outlook for 2017.

A boost to the terms of trade from higher commodity prices; sustained strong conditions in the major housing markets; still positive forward indicators for jobs; a stronger global outlook; a boost to resources exports; and a significantly reduced drag from mining investment point to the Australian economy’s growth rate lifting from the current 1.8% to 3.0% in 2017, precluding any need for further rate cuts.