by Chris Becker

As the Executive Orders come through, markets are reacting to an increasingly protectionist tone from Trump’s administration, still waiting on any news surrounding infrastructure spending or other stimulus measures as the USD falls across the board. Stocks in Asia were generally positive with bonds rising locally amid big leaps in iron ore prices and other commodities due to USD weakness.

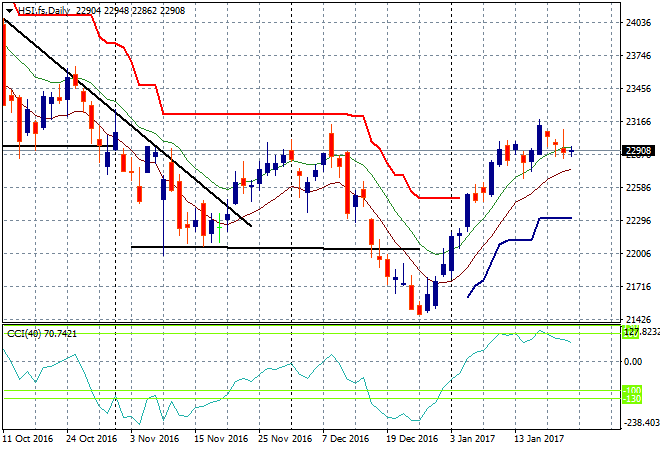

The Shanghai Composite is up 0.3% to 3145 points after returning from its long lunch break, still struggling to move higher than its artificial support level at 3100. The Hang Seng is up the same amount, but remains stalled on the daily chart after a mild selloff late last week. I’m watching the 23000 point level for a proper breakout to resume the uptrend:

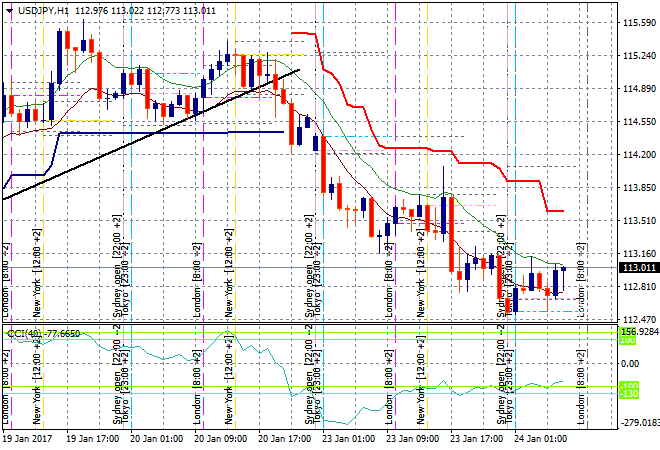

Japanese stocks remain under pressure with the Nikkei down 0.25% in the wake of a much stronger Yen. The hourly chart for USDJPY shows a deceleration in the strengthening trend, as it hovers around the 113 handle, which equates to weekly support, so watch that level closely:

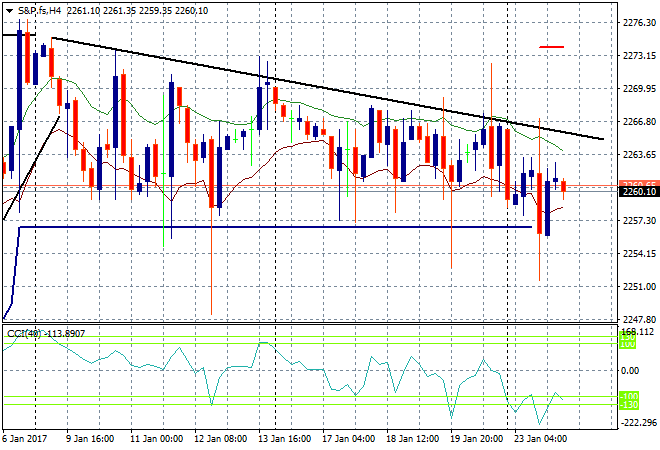

S&P Futures are looking a bit sick here with a series or lower highs and a break below ATR support last night not turning into anything comfortable to go long with. The market is still hanging on any sort of non-rhetorical substantive plan coming from the new administration:

The ASX200 is finally back, rising nearly 1% to 5650 points driven by the big miners as iron ore prices surged in late trade.

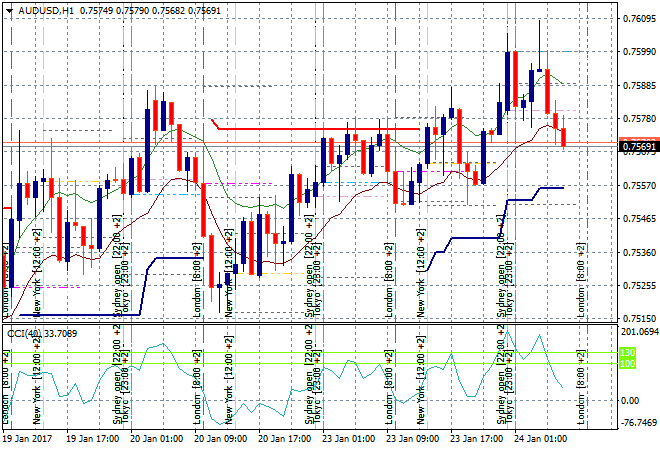

The Aussie dollar is being sold off whenever it hits the 76 handle against USD and is back down to 75.70 or so this afternoon as we go into the London open. I’m watching the low moving average at 75.60 to hold here for another attempt tonight:

The data calendar has one major thing to watch out for in Europe – the UK supreme court ruling on more Brexit machinations – withe some US home sales data later on.