by Chris Becker

Another volatile day in Asia with no lead from US overnight, as stocks fell across most of the region, excepting Hong Kong, while safe haven currencies like Yen and gold were bid higher due to more political fallout. Tonight we’ll see a “hard Brexit” line taken from Theresa May, plus a return to US trading desks, and their reaction to the weekend news.

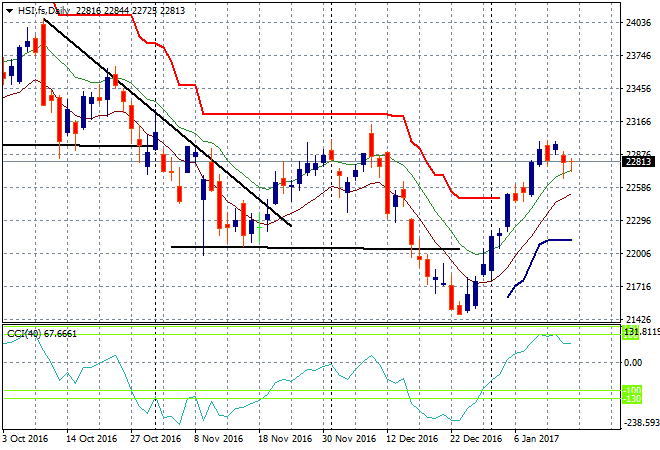

The Shanghai Composite sold off immediately again, currently down 0.5% to 3087 points as it continues to head straight down to terminal support at 3000 in a collapse of confidence. The Hang Seng is pushing the other way, up 0.4% and hanging on as it returns from its lunch break. I’m still watching the high moving average on the daily chart to come under threat here:

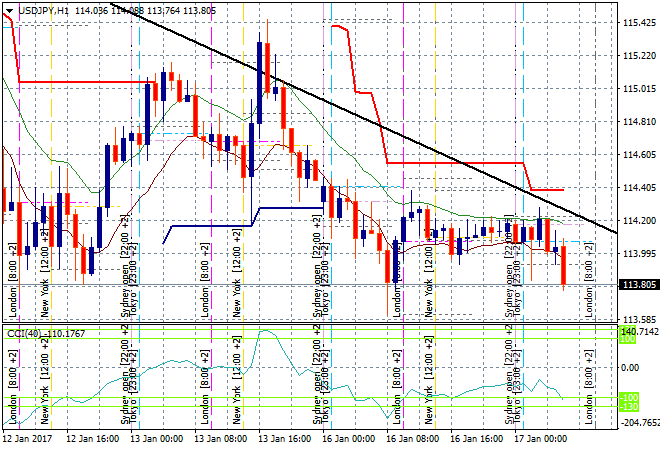

Stocks are negative in Japan with the Nikkei retreating another 1%, down below 19000 points for the first time since Xmas. The USDJPY is the culprit again as it remains on its downtrend this time extending right through the 114 handle in the last hour or so.A further bid on Yen from tonights May speech as traders dump the Pound is likely:

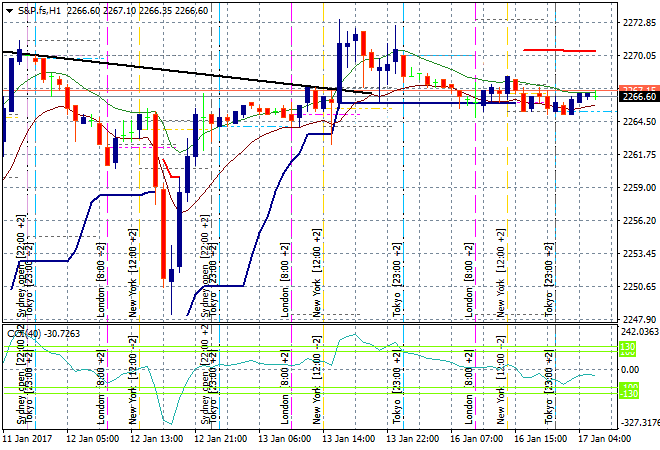

S&P Futures are flat again, dithering around ATR rolling support on the hourly chart. Trump’s weekend comments may add some volatility (how many times will I have to repeat that phrase!) going into the London open:

The ASX200 had a bad day playing catchup, down nearly 1% and closing just below 5700 points in a broad selloff. Only Newcrest Mining (read: the gold index) and Woodside had gains among the top 50 stocks, due to gold and oil prices while BHP was steady compared to the other iron ore majors.

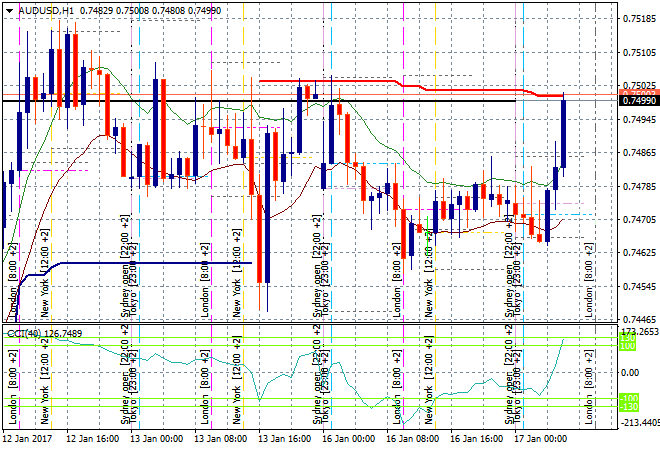

The Aussie dollar is surging going into the London open as City traders dump Pound for the safe harbor locally, zooming back up to the 75 handle against USD (and 1.60 on the GBPAUD cross) Notice this level needs to be exceeded properly in the coming sessions as its turning into quite stiff resistance:

The data calendar tonight will focus squarely on the “hard” Brexit speech forthcoming from UK PM Theresa May that will have currency markets reeling, but we also get UK CPI for December, plus the closely watched German ZEW survey around the same time. Thankfully nothing but the Tweeting Trumpster to worry about on US markets as they come back from the long weekend.