I’ve long railed against the fact that the financials index (less property trusts), the XXJ, makes up over half the ASX200, with the big four banks holding over 30% by total weight. Doesn’t give you a lot of choice when developing a robust portfolio. Moreover, overdone correlation between other sectors means that when the market is going up, its usually because of these bloated financials.

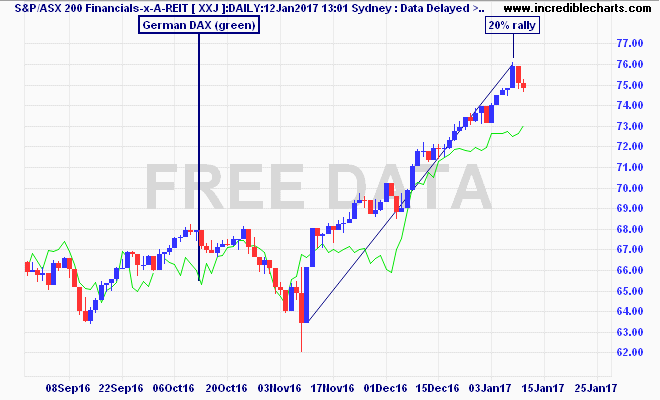

The XXJ is closely correlated to the German DAX, another financialised index, representing the exposure Aussie banks to overseas funding risk:

Since the US presidential election in November we’ve seen a13% in the ASX200, driven almost entirely by the financials, with that increase blamed on the Trump effect on US stocks, particularly US banks which are set to see the last vestiges of regulatory control thrown off them as a Republican dominated Congress is sworn in.

The real culprit is the expected inflation and higher interest ranks that should follow a big US fiscal boost, and while wholesale funding costs for local banks are expected to rise, due to their maturity profile and the slow speed at which they rise compared to what they lend – remember banks are super quick to pass on rate rises – means a fatter profit environment.

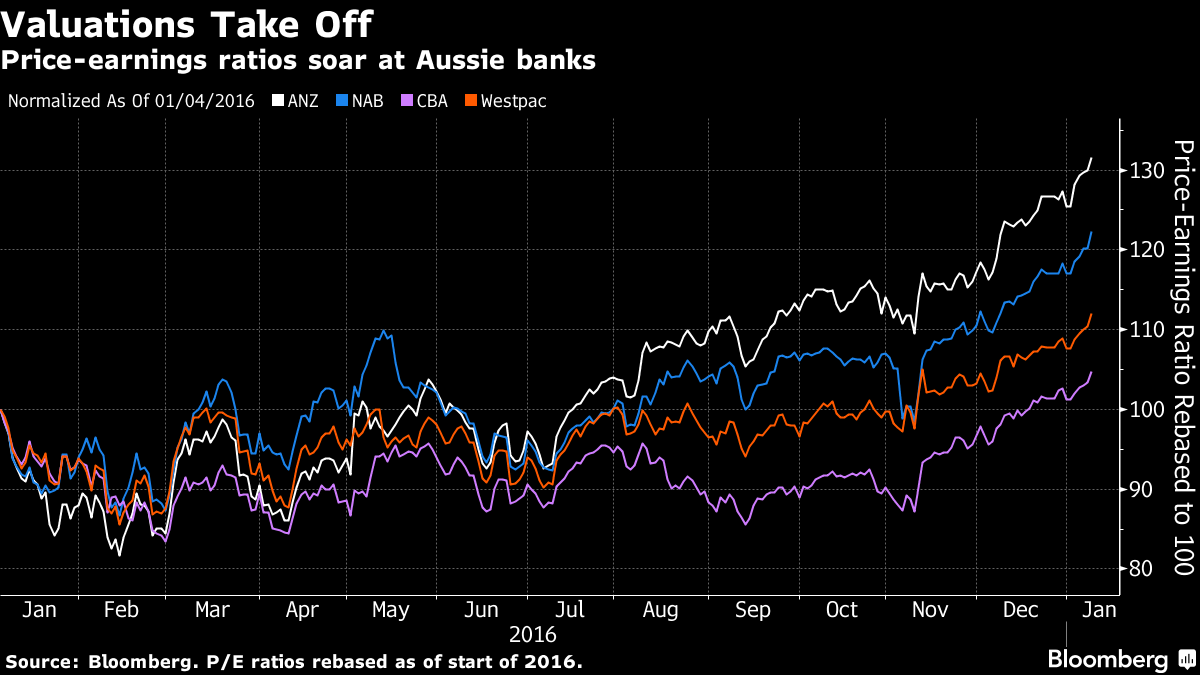

But there are concerns the rally is being fully priced in and has gone too far, too fast as valuation reach extreme levels.

From Bloomberg:

One of the fastest rallies for Australian banks in six years is prompting fund managers to stop and catch their breath.

Randal Jenneke of T. Rowe Price is pausing after moving overweight in the banking sector before the U.S. elections. “We are keen to increase our financials exposure further,” said the Sydney-based head of Australian equities at the firm, which oversees about $813 billion globally. “However, having seen some big moves in the sector recently, we prefer to wait and build our exposure in a more price-sensitive way.”

Indeed. As we move into the start of the Trumpency, its not a good time to be bailing in with all hands to buy financials, but then again with delicious dividends at hand as interest rates remain low for now, where else to go?

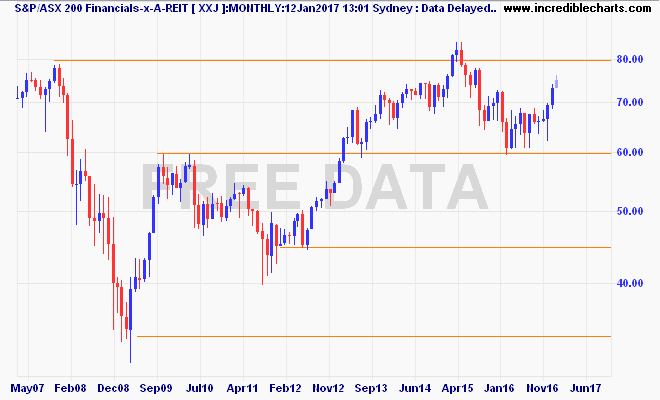

The long term chart for financials is very interesting. Two years ago, the XXJ made a new post-GFC high, finally coming back to its capital value after eight years of recovery. Since then we’ve seen a major correction and now this bounce is trying to get back to those recent highs. Technical analysis suggests that another breach – up around 8000 points for the XXJ – is a greenlight for a new bull market in financials.

1980s all over again?