Today’s housing finance data for November, released by the Australian Bureau of Statistics (ABS), posted big seasonally adjusted rises in both owner-occupied and investor finance commitments, with the overall trend in mortgage growth also starting to rise.

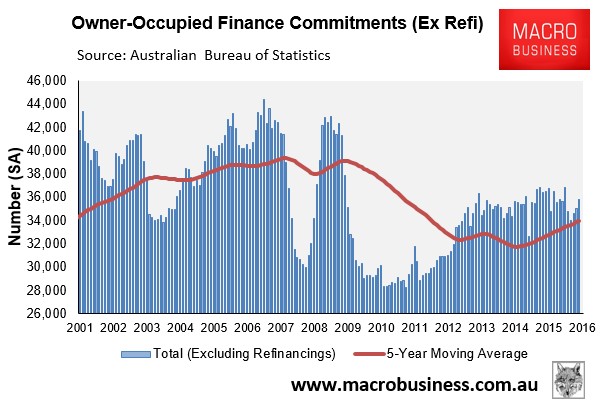

According to the ABS, the total number of owner-occupier finance commitments (excluding refinancings) rose by a seasonally adjusted 2.1% over the month but was down 2.0% over the year:

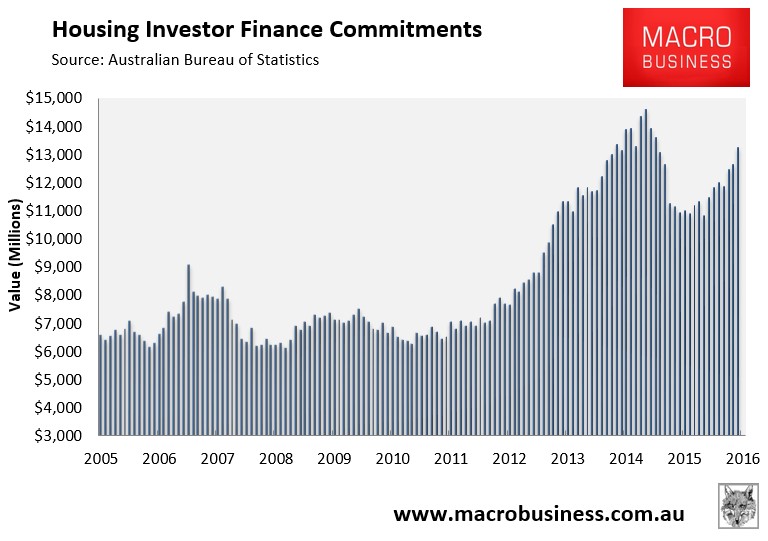

In comparison, the value of investor finance commitments surged 4.9% in November and was up by 21.4% over the year (see next chart).

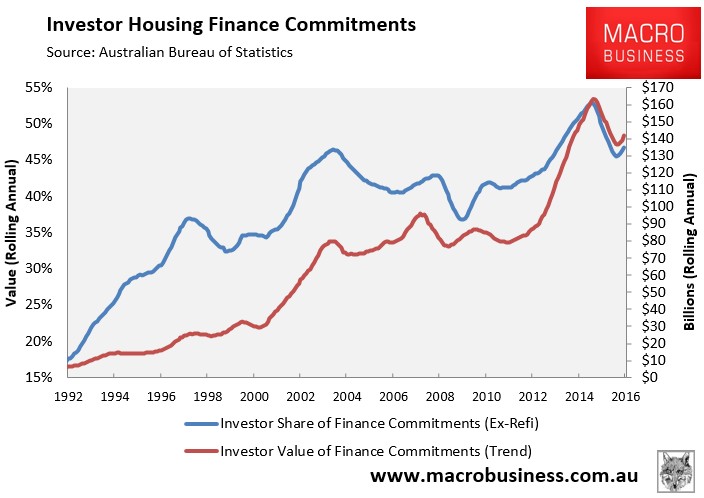

The annual share of total loans going to investors (excluding refinancings) rose by 0.5% to 46.8% in November, but was still down significantly from the peak of 52.9% recorded in July 2015:

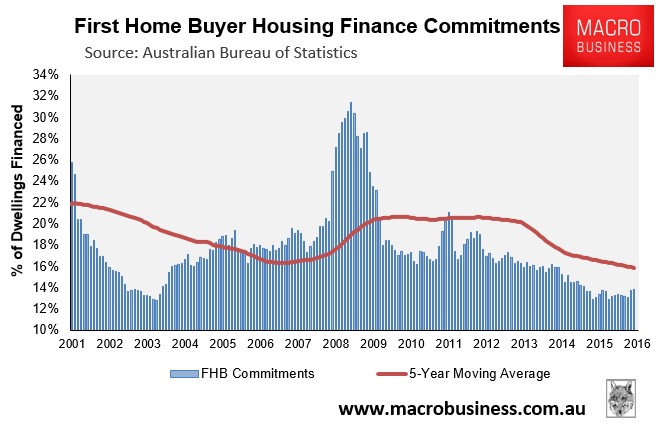

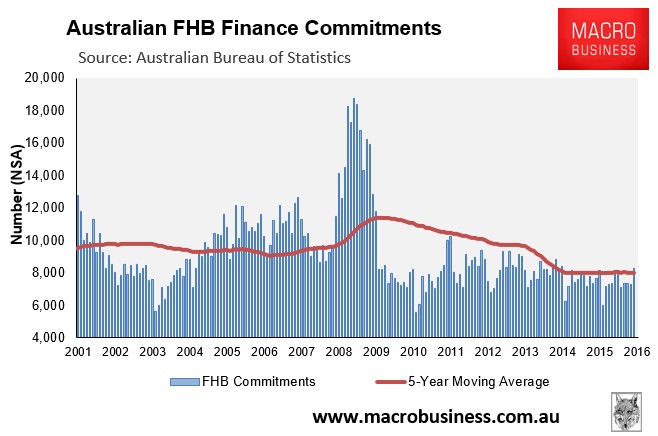

First home buyer (FHB) owner-occupied demand also surged in November. It rose by 13.4% over the month to be up 7.9% year-on-year, but still represented just 13.8% share of total owner-occupied finance commitments (see below charts).

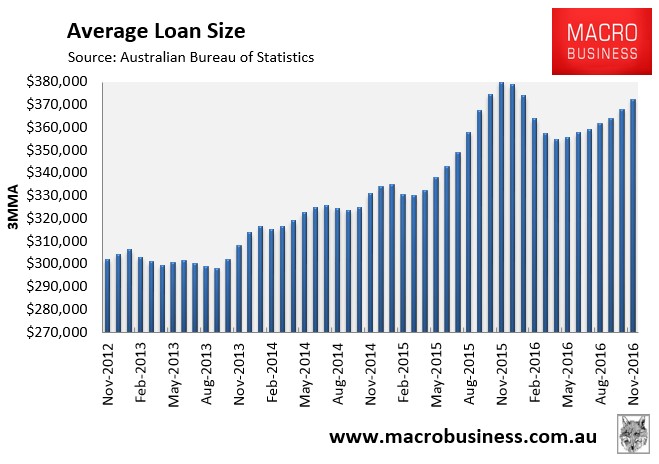

Meanwhile, the average loan size rose in November, up 1.0% over the month, but was still down by 1.6% over the year. The trend continues to recover, however, following the sharp falls at the start of last year:

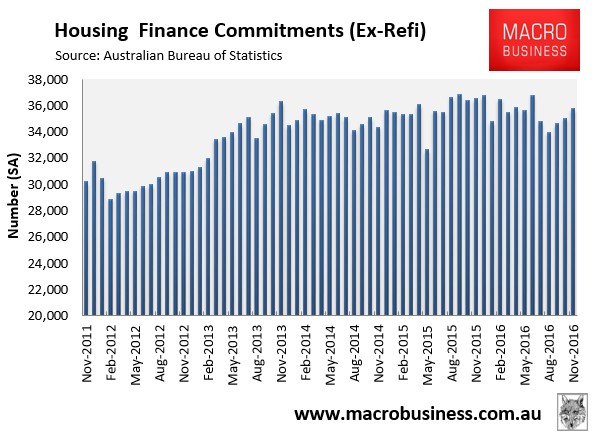

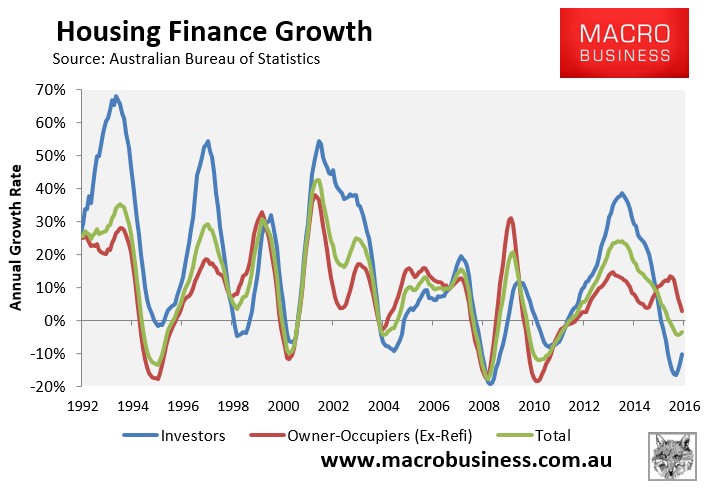

Finally, the below chart shows that falling growth in owner-occupied housing demand is now being more than offset by rebounding investor demand, causing overall growth of housing finance (excluding refinancings) to rise once again:

Back in December 2016, David Murray – the former CEO of the Commonwealth Bank and head of the Financial System Review – appeared on Switzer TV and likened the Australian housing market to the 1600’s Dutch Tulip Bubble. Murray also warned that “something needs to be done about it in a regulatory sense and the RBA and APRA need to stay on it”.

Let’s hope the latest round of investor mortgage frothiness is acted upon by APRA. Although I wouldn’t hold my breath.

unconventionaleconomist@hotmail.com