So has the dollar lost its power to move base metal prices? We think three points are worth highlighting.

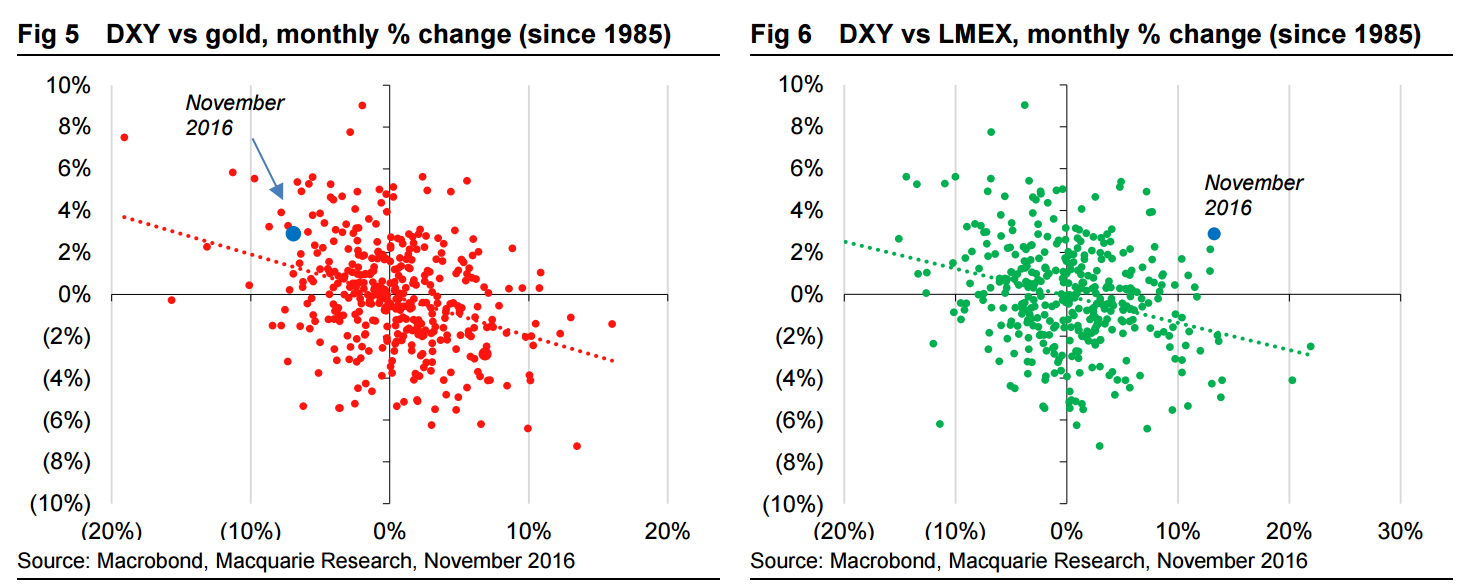

First, the value of the dollar is only one factor of many that drive metal prices. It is the yardstick by which we are measuring them, and changes in the yardstick matter, but so do a myriad of supply and demand issues. In this case clearly those are so strong they have pushed the price of metals higher, even allowing for the stronger dollar. This makes the rally even more impressive, as it means metal prices in currencies other than the dollar have rallied even harder. For example, since the US election on 8 November the LMEX index has risen 9% to its highest since May 2015, but in euros it is up 14% to its highest since January 2013.

Second, these even larger moves in other currencies have consequences for supply and demand in non-US dollar areas. Such areas are of growing importance in base metals markets given the Chinese yuan is no longer so fixed to the dollar. Indeed the price in that currency has risen by a larger amount, 11%. These consequences should be negative in that prices facing consumers and incentivising producers are even higher than a focus on the dollar price shows. However, at least in the short term, this is mitigated by the relatively low price elasticity of supply and demand in base metals (although we note copper scrap supply has been rising lately, and that Chinese battery makers have recently been said to be refusing to buy lead at recent high prices, according to Chinese consultancy SMM). Furthermore, the falling yuan might even have been positive – it seems the fear of continuing devaluation is helping the investment case for base metals demand as a hedge against further devaluation.

Third, to the extent the US dollar does still matter we would stress the importance of focusing on why it is rising. Often that works to increase the negative correlation between metal prices and the dollar, in that the dollar is a risk-off currency that benefits when things are going wrong, and commodities, with the exception of gold, tend to do better when things are going better. But at present the dollar is enjoying a risk-on rally, as investors bet that the new administration will increase US GDP growth, with a greater focus on commodity-using infrastructure. While this is not so positive for other countries, the most negative aspects of Trump’s electoral promises, such as protectionism, have been downplayed. Similarly, while this time last year the Chinese yuan’s fall was seen as an indicator of a slowing economy, at present investors are seeing it as giving a welcome boost to Chinese industry.

So in conclusion, the strength of the dollar remains a very important issue for metal prices. For gold and silver, for which dollar-area demand is a smaller proportion of the total and which do not benefit from a risk-on move, it continues to be a major headwind. In base metals it historically has had less of an impact given the significant share of production and consumption that originates in the US and China, insulating much of the market from FX moves. This should be less helpful now China’s currency is weakening against the dollar, pushing local prices higher. But even in dollars base metal prices have rallied, testament we think to the strength of the underlying bullish forces (even if short term) and that these particular FX moves have been more friendly than normal – the dollar’s rally encompassing a risk-on move and the yuan’s fall encouraging investment. Even so, we would caution that if you think prices look overextended in dollar terms, they are even more so in other currencies.

In a word, bullshit. The only conclusion to draw from that top right chart is that we’re traversing a several sigma event that is going to snap back. The commodities rally began with China’s coal policy blunder. Then it infected iron ore. Then it widened into a comprehensive futures market bubble. Now it is going to burst as China tightens on it all.

Most commodities remain in fundamental oversupply, some extremely such as iron ore and thermal coal, and once Chinese regulators frighten Banana Man out of the futures market that will reassert itself.

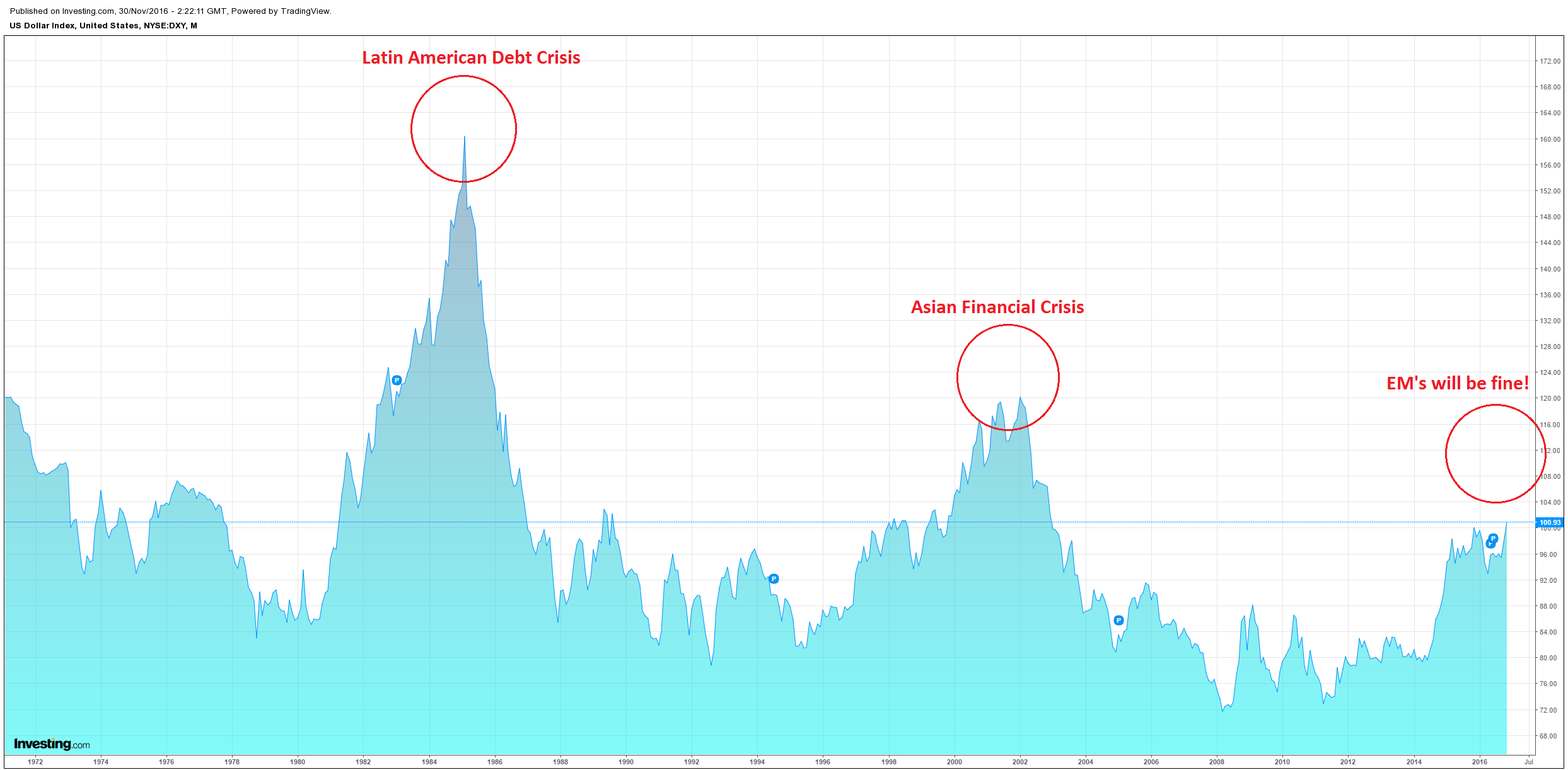

As for the USD rising, it is also bid when US growth outstrips the world, and when that happens it has a habit of blowing USD-funded and commodity-consuming emerging markets sky high:

Advertisement

I remain of the view that this is a commodity bear market rally that will reverse as China tightens and the USD runs riot over the top of it.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.