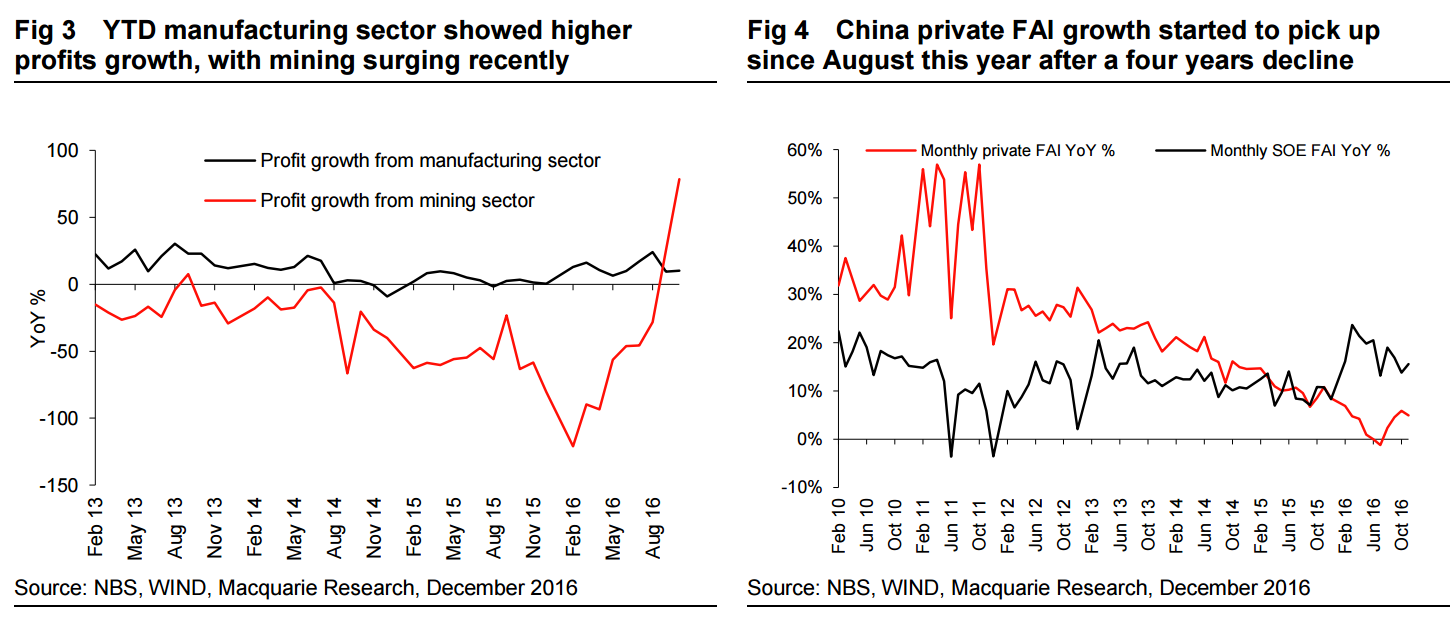

Indeed the biggest change in November FAI came from manufacturing. Investment from the manufacturing sector only increased by 3.1% YoY in the first 10 months and 2.8% YoY in October, but jumped by 8.4% YoY in November. This improved investment from the manufacturing sector was helped by their increased profitability after the recovery in producer price inflation (PPI), with manufacturing total profit growing by 13.2% YoY in the first 10 months of the year according to NBS, compared with a small growth of 2.8% YoY for the full year 2015. The other big sector, mining, continued to have negative FAI growth in November.

In addition to improved manufacturing FAI, we noticed that private FAI as a whole has grown by about 5% YoY growth since September. The private FAI growth bottomed in July when it dropped to -1.2% YoY, and has risen since. Private FAI accounts for 61.5% of China total FAI, based on the official statistics, although total FAI remains largely driven by SOE investment that increased by 15.5% YoY in November. A steady recovery in private FAI is positive for the outlook of economy growth given its importance in the economic system, but as this strengthens we believe the government may feel a greater inclination to slow public sector investment to prevent the economy from overheating.

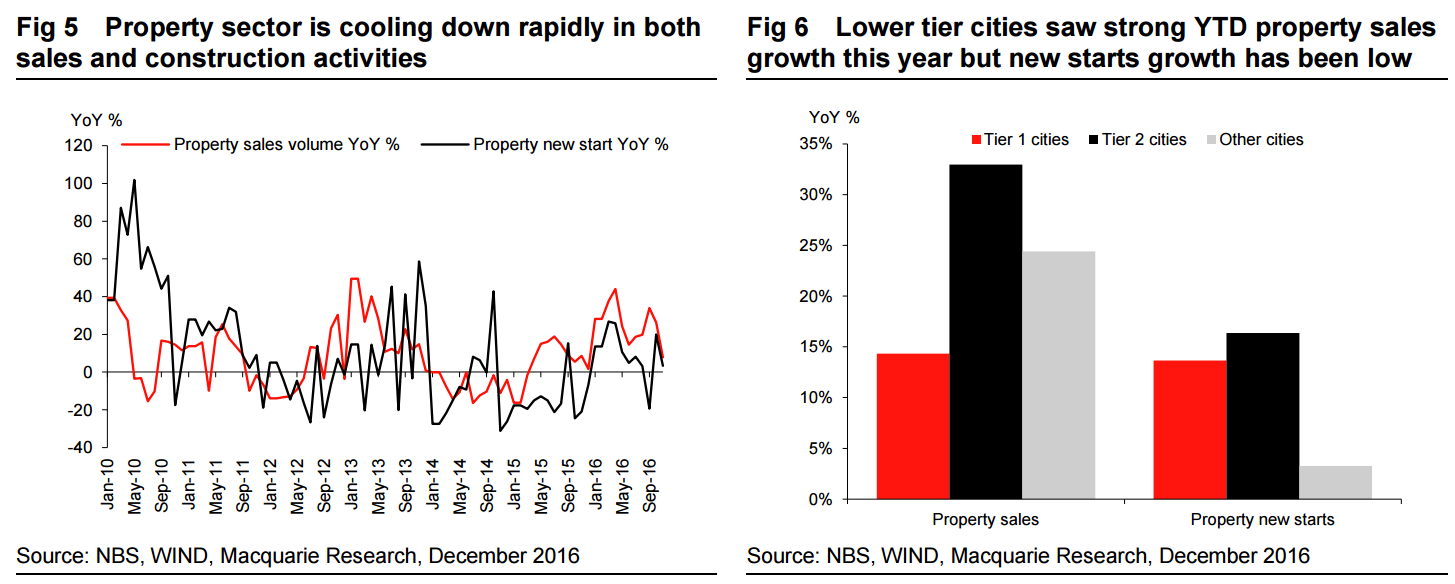

In contrast to the positive signals from manufacturing and other private industry, more concerning for commodity demand, especially bulks such as steel and cement, is the potentially faster cooling in the property market. Unlike previous months when we saw property construction activities slow but sales remained strong, in November property sales growth showed a big deceleration, down from 26.4% YoY in October to 7.9% YoY. Along with fading sales momentum, floor space new starts only increased by 3.3% YoY in November, down from the 8% YoY growth in Jan-Oct and 20% YoY in October, and property investment also recorded a milder growth of 5.7% YoY in November, falling from 13.4% YoY in October.

Of course it is important to note that some of this slowdown can be attributed to higher base effects given the property market turned upwards in 4Q15. But it is also not surprising to see property sales cool down given a series of tightening measures which were announced since late September in over 20 Chinese cities. Nevertheless the slowdown is sharper than market expectations and our property analyst believes sales will likely to remain weak and may worsen in Jan-Feb, which is the traditional off-season. So far property tightening measures have been mainly announced by tier 1 and 2 cities, accounting for 40% of national total property sales and also new starts (based on our estimation). For the remaining 60% from lower tier cities their property sales have been quite strong in Jan-Oct, rising by over 24% YoY YTD, but their new starts only increased 3.3% YoY over the same period given their generally higher inventory levels from the beginning of the year, versus 13.7% YoY growth in tier 1 cities new starts and 16.4% in tier 2 cities for the first 10 months.

The implication of such divergence in sales and construction activities (new starts) by city tiers is that even if national property sales continue to grow next year thanks to the bigger share of sales from lower tier cities, construction activities growth should slow down more than sales given the growth has been mainly driven by higher tier cities which are suffering from tightening policies. Such a slowdown would be negative for materials that are more intensively used in the early stages of property projects like steel, but for aluminium and copper the demand from property sector may be able to sustain for longer into 2017 as developers need to finish their projects which are already under construction in order to fulfil their pre-sale contracts.

Chinese steel production to slow at the margin in 2017. I’m thinking roughly of a reversal of this year’s 1omt output jump.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.