The Grattan Institute has released a report calling on the Federal Government to implement a 15% fee on student loans in a bid to rein-in escalating student loan costs and make the university funding system sustainable.

Below is the overview of the report along with some key charts:

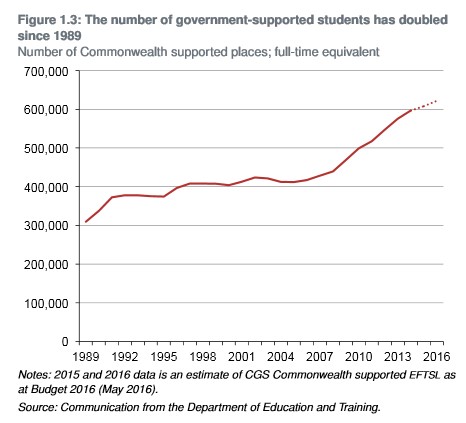

Introduced in 1989, HELP has greatly expanded access to tertiary education. Students can finance their education by taking out HELP loans. By requiring students to contribute financially, the government can spread its limited resources across more students.

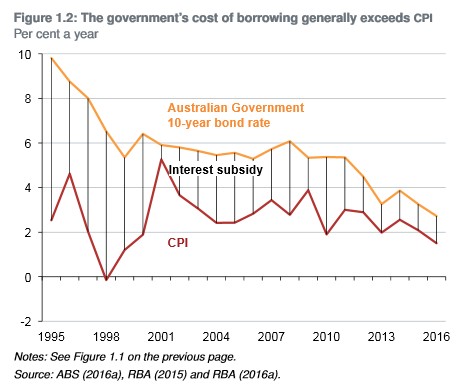

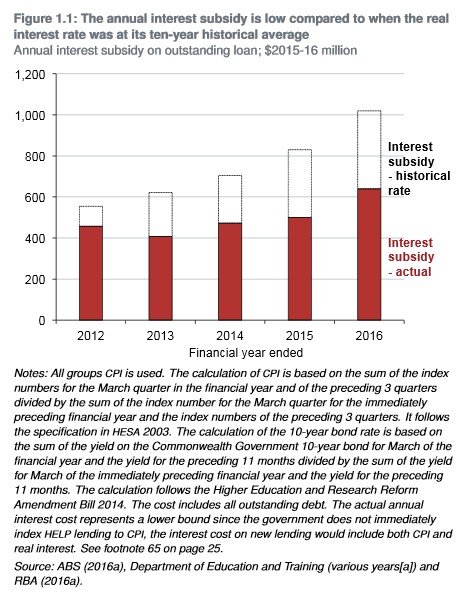

But financing these loans is costly for taxpayers. Every year the government pays the difference between the CPI interest it charges students and the cost of its own borrowing to finance government debt. Women receive 17 per cent of their original borrowing in interest subsidies while men receive 16 per cent on average.

As of mid-2016, total HELP debt is about $52 billion.

Interest costs will escalate as total HELP debt grows and interest rates increase. The government currently pays a low interest rate on its debt, but this could increase by 60 per cent if real interest rates return to their average over the last ten years.

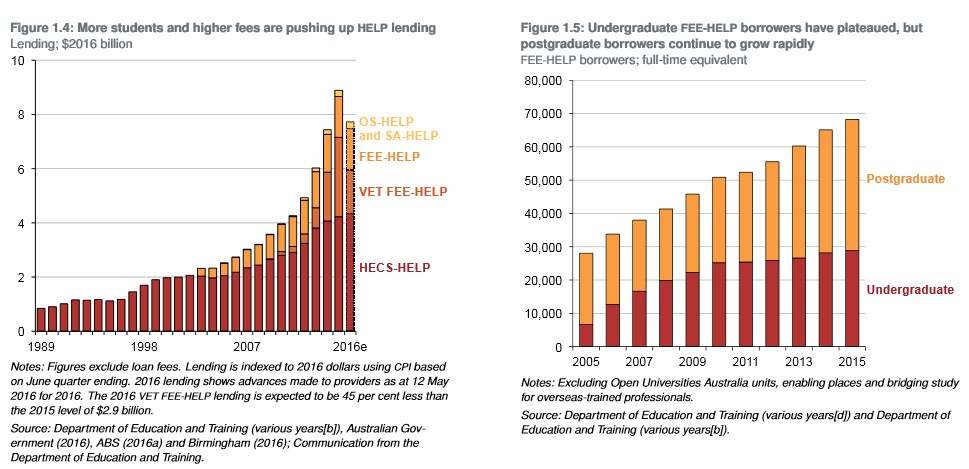

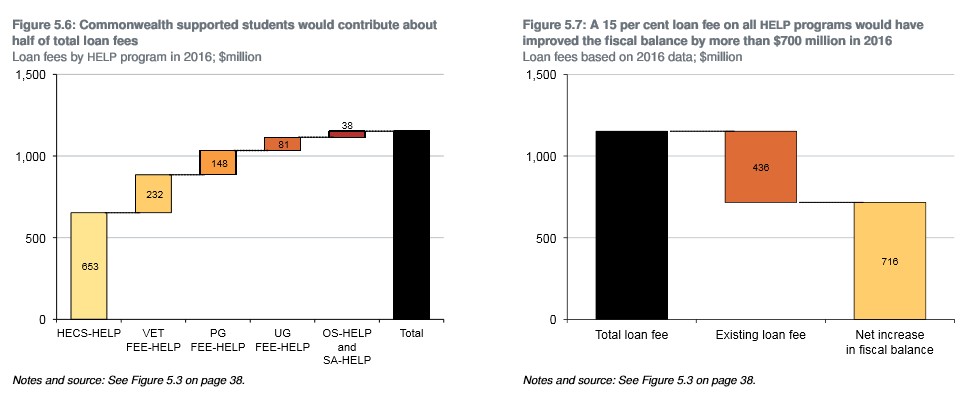

The government could recover most of its interest costs by charging loan fees on all new HELP lending. Loan fees would be added to borrowers’ outstanding balance. A universal 15 per cent loan fee would have saved $700 million in 2016.

The universal loan fee would replace existing loan fees. Full-fee vocational education and undergraduate students pay loan fees of 20 and 25 per cent respectively while postgraduate and government-supported students do not. These loan fee differences among students are unfair and lack a policy rationale.

Loan fees preserve HELP’s policy goals. Cash-poor students can continue to borrow with no upfront charges. Low-income graduates would continue to repay nothing until their income reaches the HELP threshold, which is currently $54,869. For repaying HELP debtors, loan fees would extend the repayment period for the median employed graduate by about a year but leave annual repayments unchanged. As a result, loan fees would have little impact on access to higher education Loan fees would improve the targeting of interest subsidies.

At the moment, while low-income HELP debtors receive the highest subsidies, affluent graduates still receive about 10 per cent of their original borrowing in subsidies. Their earnings average more than $120,000 a year. The case for subsidising them is weak.

With a universal 15 per cent loan fee, high-income graduates who repay quickly would more than cover their interest costs. They would cross-subsidise the cost of low-income graduates who repay more slowly.

Loan fees are progressive compared to previous proposals to charge real interest rates on HELP loans. If real interest rates are charged, debtors taking breaks from work or earning low incomes pay more interest than high-income earners with the same original debt. With loan fees, interest charges vary with the amount borrowed but not with how long it takes to repay.

Both the current and the previous government have tried to reduce higher education spending. But any savings need to be consistent with educational and social goals. Loan fees would contribute to budget repair, but leave per student university funding unchanged, reduce pressure to cap student numbers, avoid upfront charges, and preserve protections for low-income graduates.

While this proposal would help to rein-in soaring university costs, it does not overcome the fundamental problem: that Australia’s universities have turned into ‘degree factories’, whereby they teach as many students as possible to accumulate Commonwealth government funding through HELP/HECS debts.

Advertisement

This ‘churn’ approach to university has seen the dramatic lowering of entrance scores, suggesting that every person and their dog can now enroll for a degree, devaluing their worth in the process.

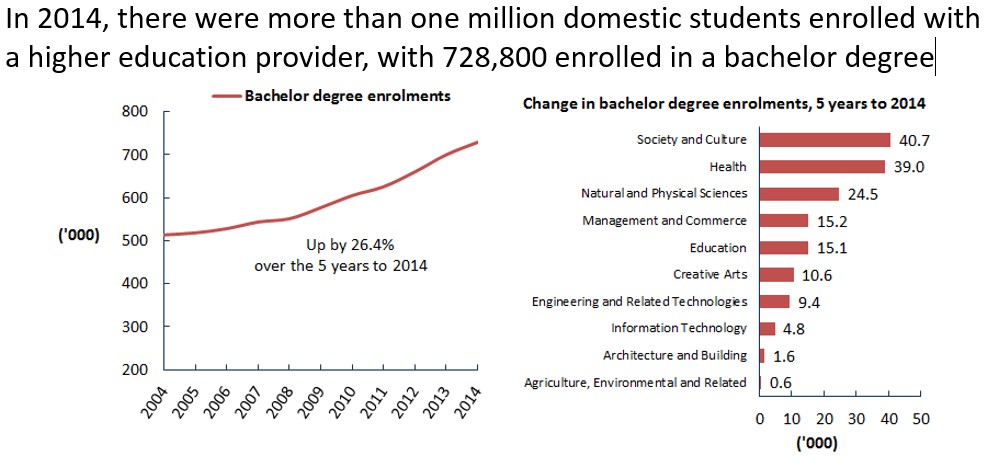

The latest Department of Employment’s skills shortages report showed there were a record 1 million domestic students enrolled with a higher education provider, 730,000 of which were enrolled in bachelor degrees:

Advertisement

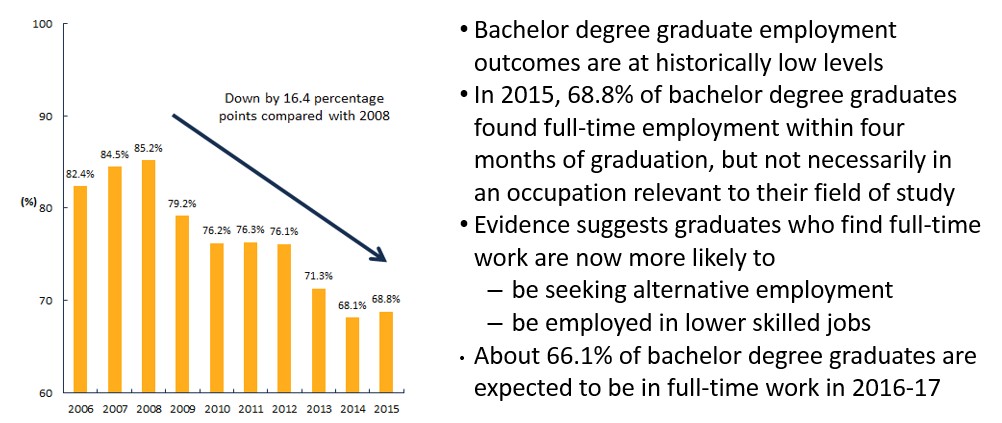

However, bachelor degree graduate employment outcomes are falling and are at “historically low levels”:

Clearly, there are problems with Australia’s demand-driven university system, which has grown in cost but is delivering poorer outcomes.

Advertisement

This view was reinforced by the Productivity Commission’s (PC) final Migrant Intake into Australia report, released in September, which contained some worrying data highlighting the deterioration of university graduate outcomes, whereby achieving stable and well-paid employment has become increasingly illusive:

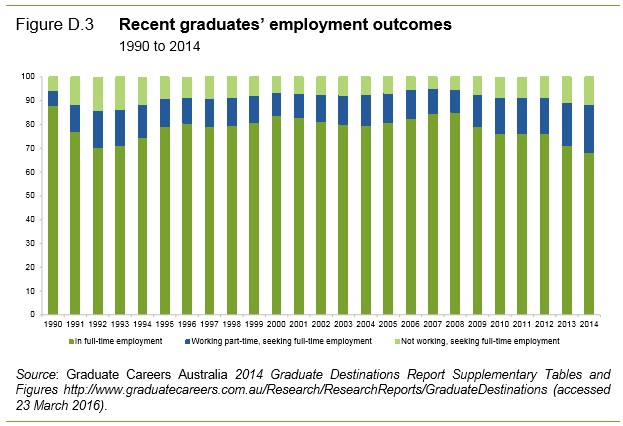

Education does not guarantee employment, and evidence suggests that it is becoming harder for recent graduates to find a job on completion of their education (Reserve Bank of Australia 2015). For example, the share of higher education graduates in full-time employment four months after graduation fell from 85.2 per cent in 2008 to 68.1 per cent by 2014 (figure D.3).

The 17 percentage point fall in the share of recent graduates in full-time employment from 2008 to 2014 has been matched by an 11 percentage point increase in the share of recent graduates in part-time employment and a 6 percentage point increase in the share of recent graduates not working.

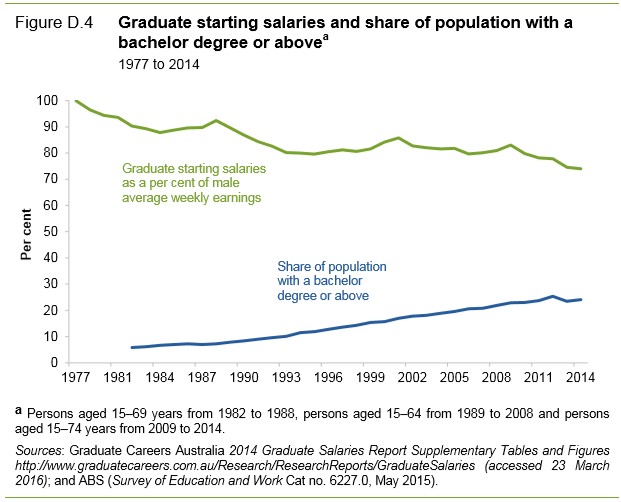

Graduate starting salaries have grown more slowly than average earnings over a long period. In 1977, median starting salaries were equal to male average weekly earnings. By 2014, median starting salaries had fallen to 74 per cent of male average weekly earnings (figure D.4). This has coincided with an increase in the share of the population with bachelor degrees, from 5.8 per cent of the population in 1982 to 24.1 per cent in 2014.

As the supply of people with tertiary qualifications has increased, the market return on a qualification may have decreased…

A recent report from the National Institute of Labour Studies at Flinders University also showed that between 2008 and 2014, the proportion of new university graduates in full-time employment dropped from 56.4% to 41.7%.

Advertisement

In short, Australia’s university system is churning-out far more graduates than the economy requires, suggesting the policy response should focus on better rationing university places.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.