Some pretty cool stuff here from Deutsche’s Tim Baker and Joseph Kim:

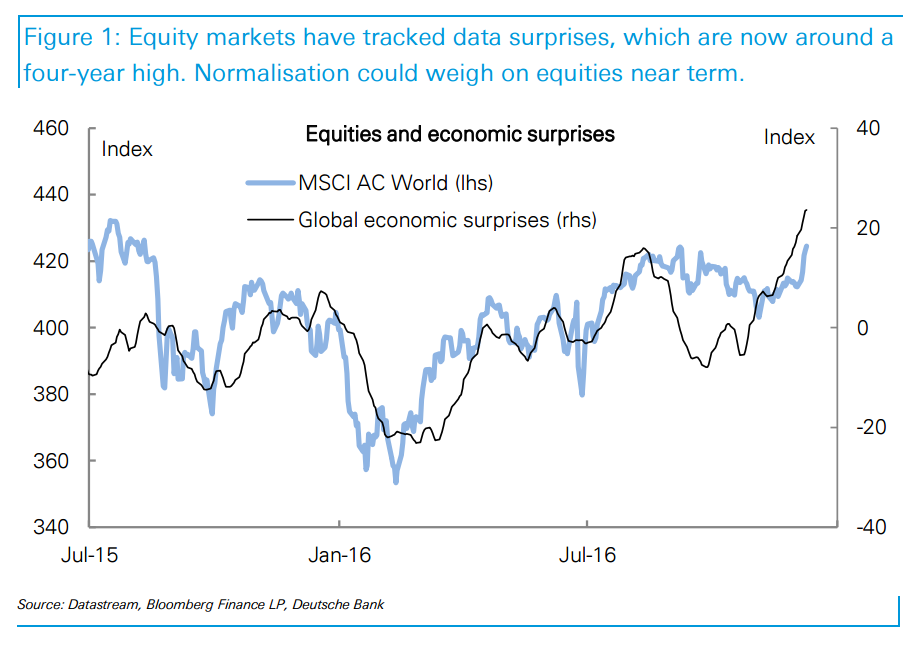

Equity markets have tracked data surprises over the past year. With data surprises now around a four-year high, there’s risk that normalization could undermine equities. (Chart 1).

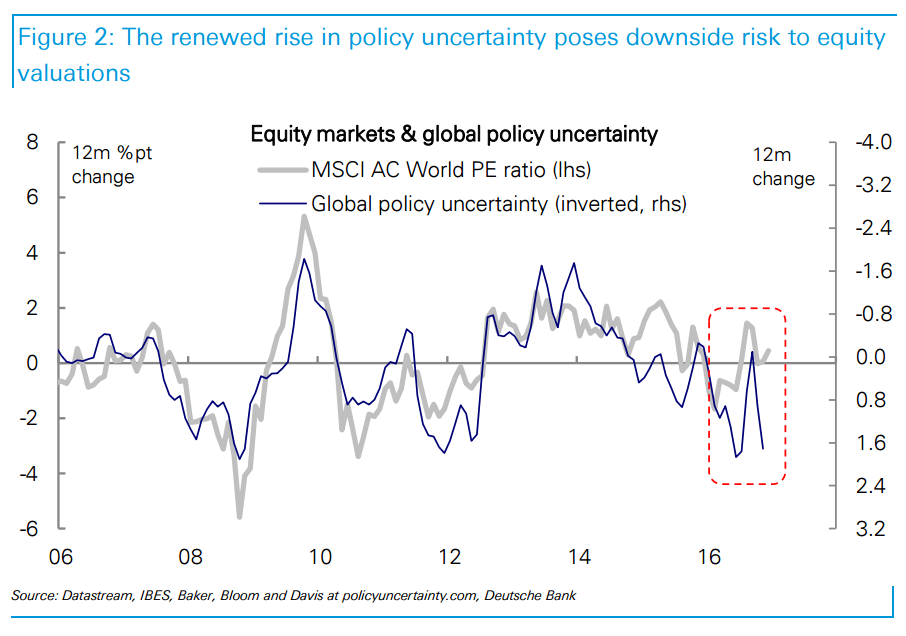

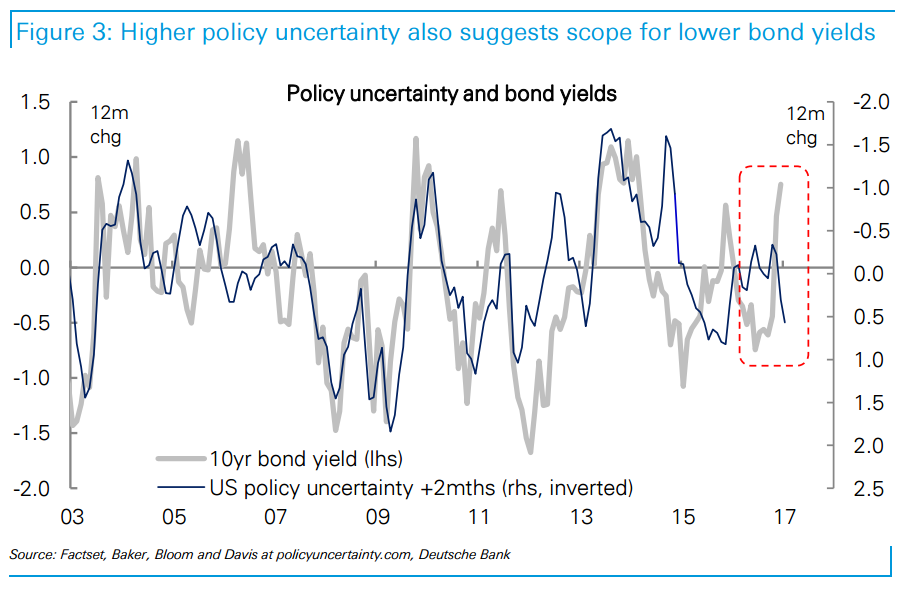

The renewed rise in policy uncertainty poses downside risk for PE ratios and for bond yields. (Charts 2 and 3).

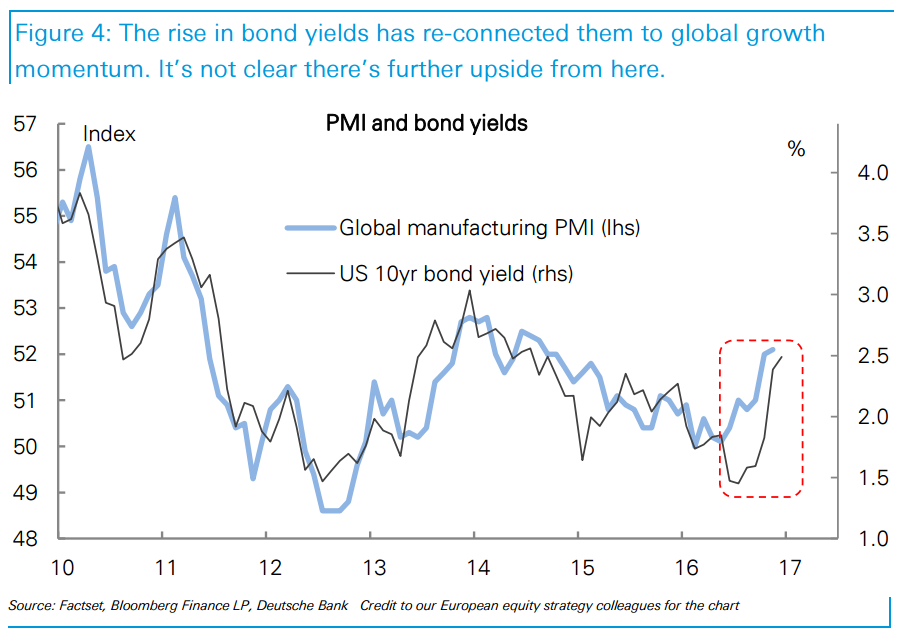

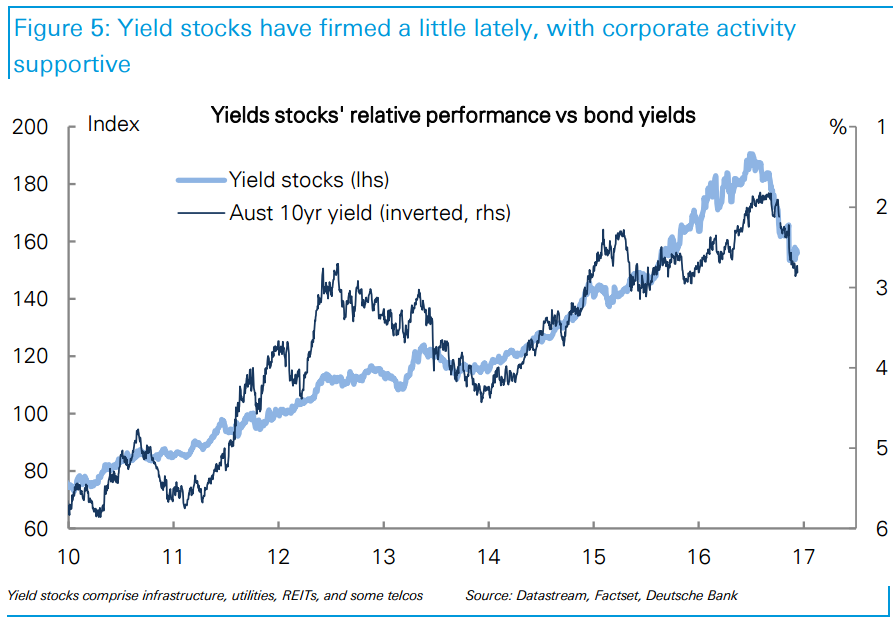

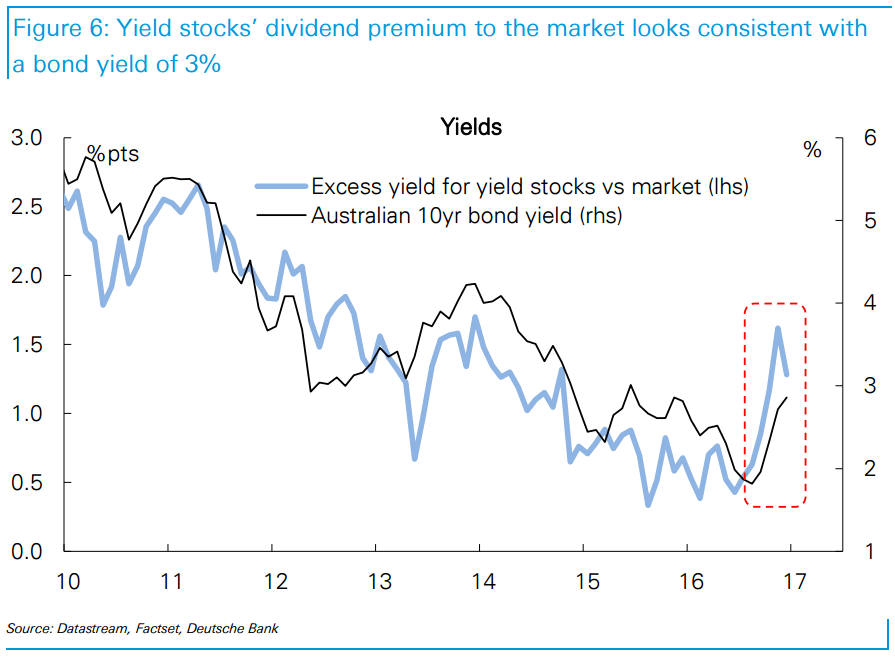

After the recent rally, bond yields now look broadly in-line with global growth momentum. Yield stocks are off their lows, though still look priced for an Australian bond yield at 3%, which seems excessive. (Charts 4, 5 & 6).

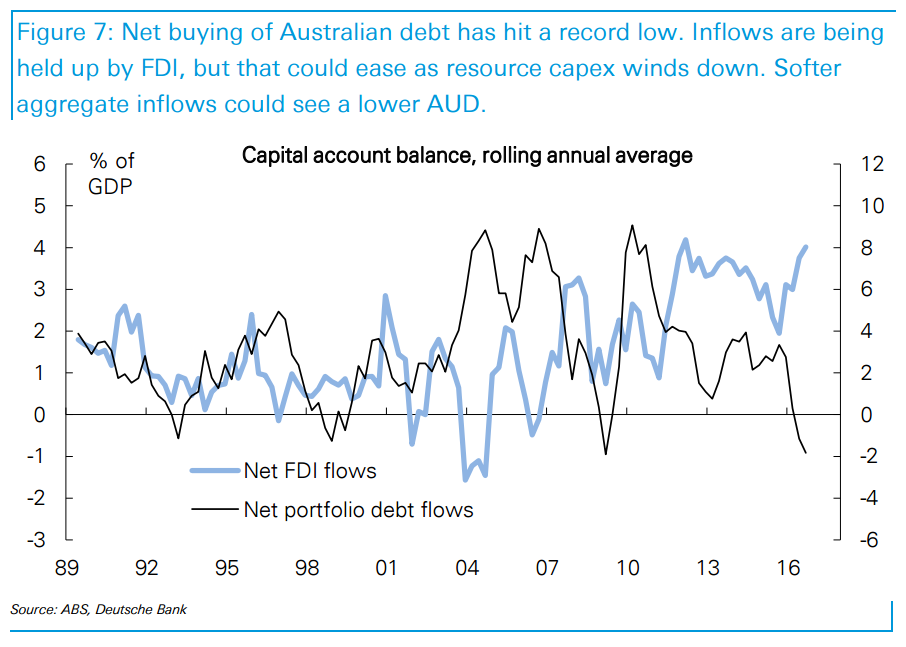

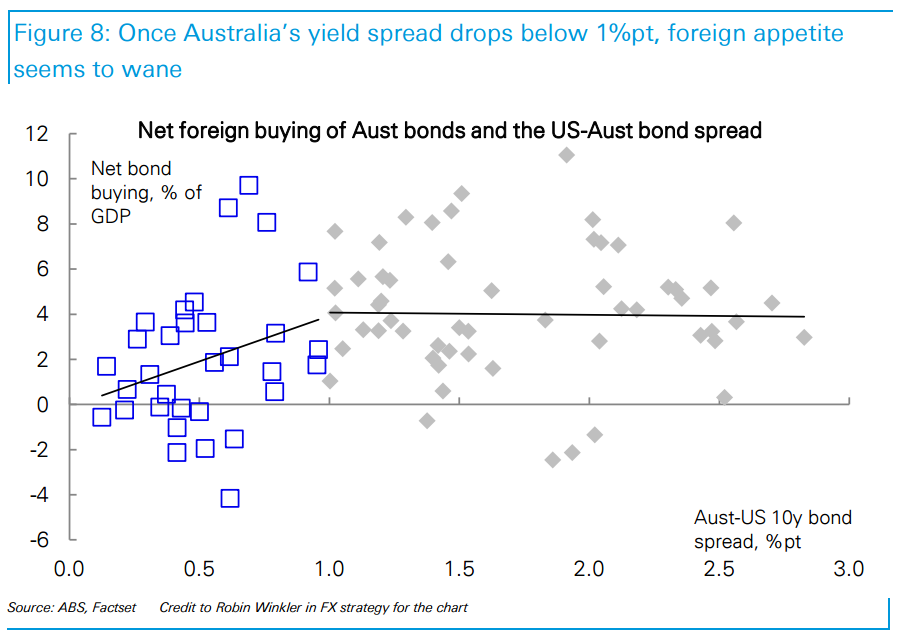

The shrinking rate differential has led to net foreign buying of Australian debt hitting a record low. FDI is holding up, but seems bound to soften as resource capex winds down. Softer aggregate inflows could weigh on the AUD – we prefer stocks with USD exposure. (eg, Aristocrat, Amcor, Macquarie). (Charts 7 & 8).

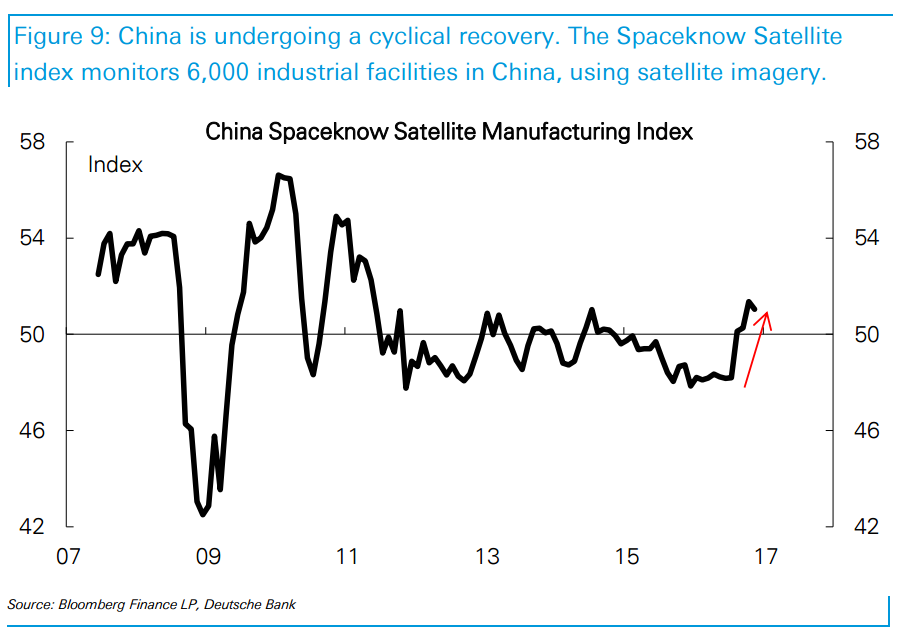

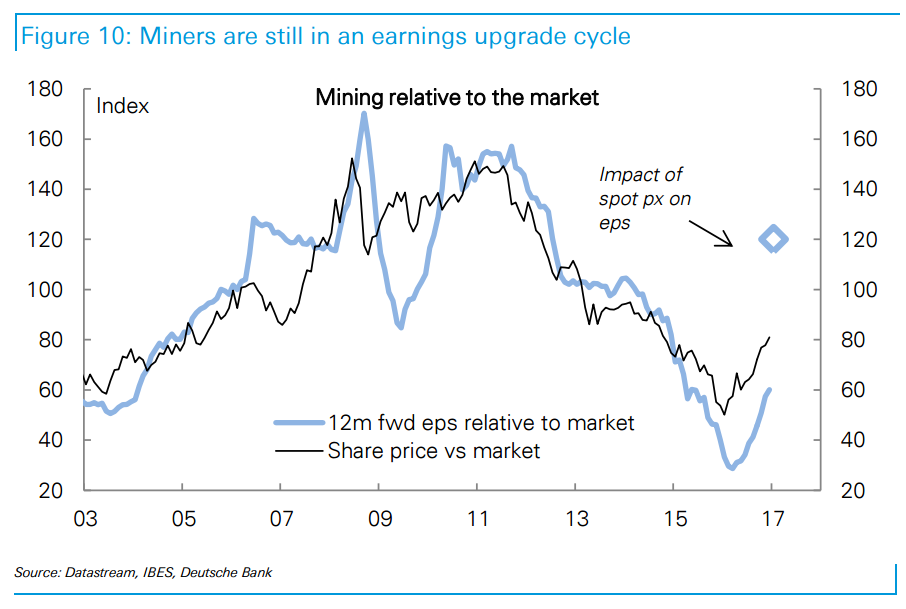

The China Spaceknow Satellite Index (which uses satellite imagery to gauge industrial activity) points to a solid cyclical recovery since mid-year. This is supporting commodity prices, keeping miners in an earnings upgrade cycle. (Charts 9 & 10).

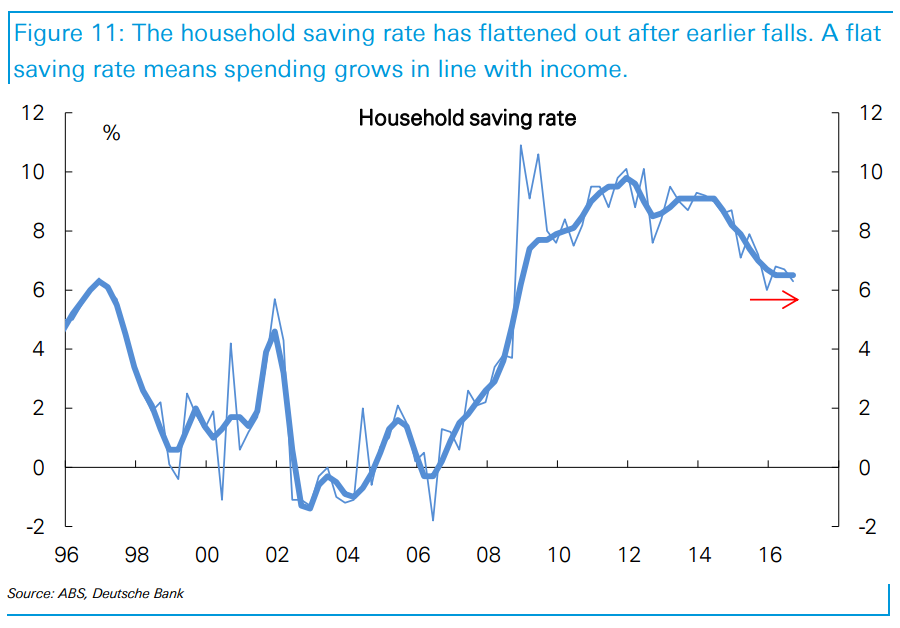

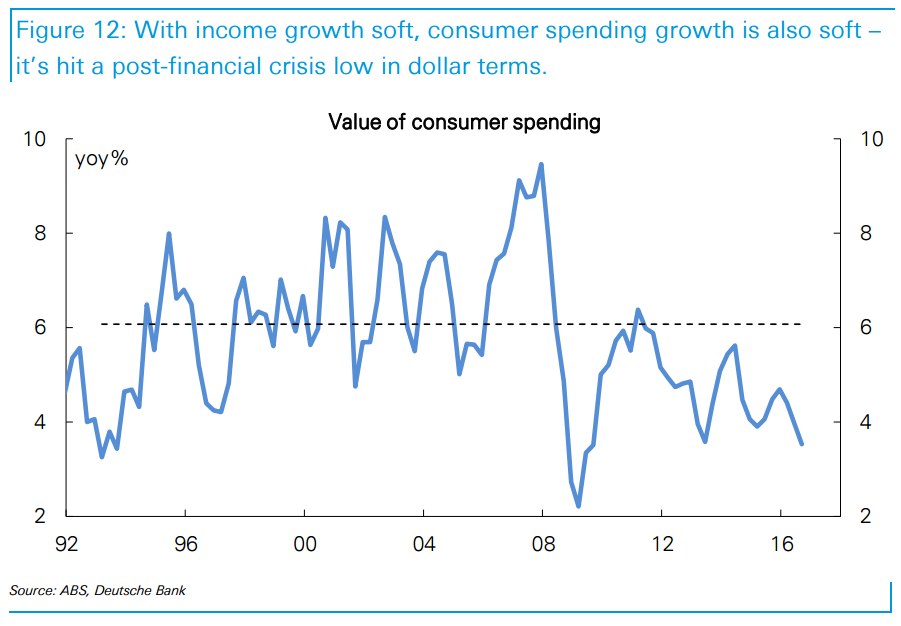

The household saving rate fell in 2014/15, providing a boost to spending growth. But saving has flattened out this year, meaning spending grows in line with incomes (which are growing softly). Spending growth in dollar terms is now the lowest since the financial crisis, making us cautious on consumer exposure through the Christmas period. (Charts 11 & 12).

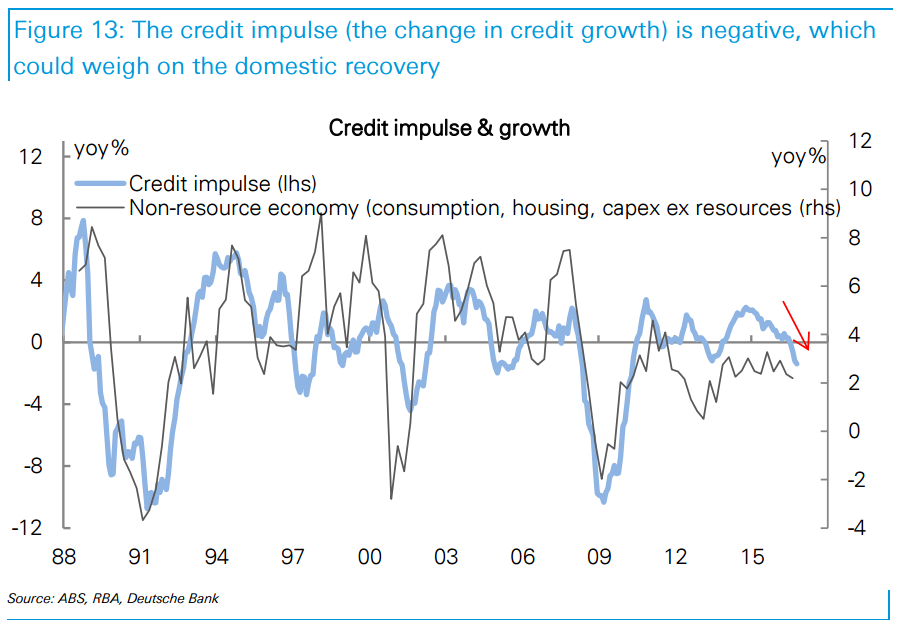

The credit impulse (the change in credit growth) is negative, weighing on the domestic recovery. We expect the RBA to cut in 2017 to support growth. (DB economists forecast a cut in May). (Chart 13).

Excellent. The only point I’d add is China will slow in 2017 and miners turn down in 2017.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.