From Westpac:

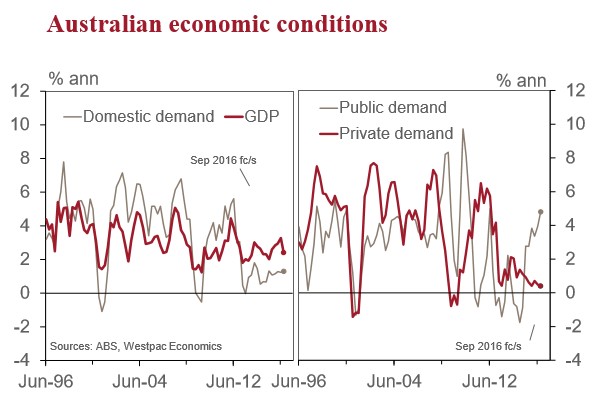

- The Australian National Accounts, to be released on Wednesday December 7, will provide an estimate of economic activity for the September quarter. • In the year to June, real GDP grew by 3.3%, an above trend pace, with trend judged to be 2.75%. Activity was supported by lower interest rates (housing) and a lower dollar (service exports). Mining’s impact was relatively neutral, with falling investment offset by rising exports.

- However, a loss of momentum was evident mid-2016. This reflects: July Federal election impact; tighter lending conditions 2015H2; sluggish employment after a hiring burst / overshoot in 2015; and consumer caution.

- The economy is likely to emerge from this soft patch. Prospects for 2017 remain constructive, supported by: recent RBA rate cuts; with the election behind us; a lift in jobs growth, with current softness overdone; higher commodity prices; and stronger US growth.

- In the June quarter, GDP increased by 0.5%. The arithmetic was: domestic demand +0.6%; inventories +0.3ppts; net exports –0.2ppts; and statistical discrepancy –0.1ppts. Of note, a one-off jump in public demand added 0.5ppts to growth in the quarter while consumer spending growth slowed to 0.4%, moderating from 0.8% in Q1.

- For the September quarter we anticipate real GDP growth of 0.2%qtr, 2.4%yr – with downside risks. The arithmetic is: domestic demand –0.3%; inventories flat; net exports +0.2ppts; and statistical discrepancy +0.2ppts. Implied here is that the Income measure of GDP will be stronger than the Expenditure measure.

- On domestic demand in Q3: home building activity dipped in the quarter; business investment contracted at a faster pace; and public demand consolidated.

- On the consumer, accounting for 55% of the economy, the national accounts provides us with an update on spending, saving and incomes. We anticipate a slight uptick in spending in Q3, +0.5% after a +0.4%, supported by a strengthening of wage incomes.

- Labour market conditions while not strong in Q3 improved on those prevailing in Q2. True employment growth was little changed, 0.3% up from 0.2%, but hours worked turned around, rebounding 0.5% after a 0.6% decline.

- National income has strengthened in 2016 as commodity prices, which trended lower over recent years, have rebounded. In Q3, the terms of trade increased by 3.5%, we estimate, after a 2.4% rise in Q2. Nominal GDP growth is a forecast 1.2%qtr, 3.6%yr, up from 2.0%yr for 2015.

- The Business Indicators survey, on Monday, will provide some partial information on official estimates of incomes for the quarter, including an update on wage incomes and profits, key inputs into our GDP(I) view.

Household consumption (0.5%): Consumer spending grew by only 0.4% in Q2, after a 3.1% increase over the previous year. Real wage incomes were soft in Q2, +0.1%. In Q3, real retail spending stalled, -0.1%, following a gain of 0.3%. We anticipate that the slowing of retail will be more than offset by spending on services, funded by a strengthening of wage incomes.

Dwelling investment (–2.0%): Home building activity declined in Q3, down by about 2%, with weakness in both new and renovations. This follows gains in 12 of the past 13 quarters. A rebound in approvals, returning to historic highs in mid-2016, will support a modest lift in activity near-term.

New business investment (–4.0%): A 2% decline in business investment accelerated to a 4% fall in Q3. Commercial building declined sharply, after being supported by running down the work pipeline. Equipment spending was cut in the quarter, reversing a modest rise in Q2. Infrastructure activity continues to contract, with the mining investment downturn nearing its end.

Public spending (0.1%): Public demand, 20% of the economy, is likely to consolidate after a 2.4% jump in Q2, the strongest quarterly gain since the fiscal stimulus package of 2009/10.

Net exports (+0.2ppt): Net exports are a key growth engine at present, with resource exports expanding on new capacity and services boosted by the lower AUD. In Q3, exports grew by a forecast 1.8%qtr, 6.5%yr with gains in coal, gold, services and rural goods. Imports rose by a forecast 1.0% in the quarter.

Private non–farm inventories (0.3%, 0.0ppt contribution): Inventory levels, which have been expanded to meet rising household demand, are expected to increase by a modest 0.3% in Q3 (with downside risks) against the backdrop of patch conditions. Volatility in mining and manufacturing inventories is a potential source of surprise quarter to quarter.

The Business Indicators survey (Mon), the Balance of Payments (Tue) and Public Demand data (Tue) will provide further clues as to the risks surrounding our forecast for GDP (published Wed).