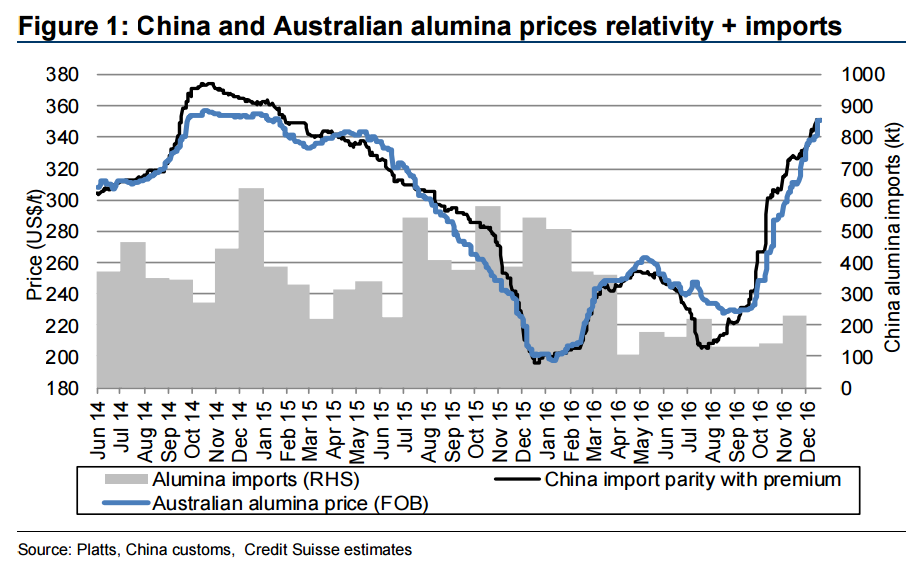

■ The alumina price has climbed to $351/t, the highest for almost two years, driven by China. However, unlike late-2014, there is no fundamental alumina shortfall in China. In fact, the buoyant price caused Chinese alumina output to surge in Oct and Nov such that China was long alumina by almost 150kt in November, a highly unusual occurrence. Figure 1: China and Australian alumina prices relativity + imports 0 100 200 300 400 500 600 700 800 900 1000 180 200 220 240 260 280 300 320 340 360 380 Jun 14 Jul 14 Aug 14 Sep 14 Oct 14 Nov 14 Dec 14 Jan 15 Feb 15 Mar 15 Apr 15 May 15 Jun 15 Jul 15 Aug 15 Sep 15 Oct 15 Nov 15 Dec 15 Jan 16 Feb 16 Mar 16 Apr 16 May 16 Jun 16 Jul 16 Aug 16 Sep 16 Oct 16 Nov 16 Dec 16 China alumina imports (kt) Price (US$/t) Alumina imports (RHS) China import parity with premium Australian alumina price (FOB) Source: Platts, China customs, Credit Suisse estimates

■ China appears to be experiencing regional tightness, rather than an overall alumina shortfall, with transport constraints restricting alumina deliveries from Shanxi refineries in particular. In addition, demand has been abnormally high as wary smelters are stocking up with alumina heading into winter when transport difficulties might worsen. And the tightness has allowed refineries to pass on cost increases from higher coal prices.

■ But the aluminium price is insufficient to support the alumina price. We estimate the high costs for coal and alumina may have raised the costs of an average Chinese smelter to around Rmb15,500/t, if it is fully exposed to market prices for inputs, from Rmb12,000/t a year ago when smelters were curtailing on losses. With the aluminium price subsiding towards Rmb12,700/t in Dec, from Nov highs, smelters may face losing Rmb3,000/t.

■ Price moderation may be driven by destocking. A similarly high alumina price began to unwind in Jan-15 despite a sizable China alumina deficit at that time, probably because smelters were in a mid-winter destock, not buying. We expect similar smelter destocking this Jan and Feb which may allow the price to ease. In our Commodities Forecasts of 7 December, we forecast the alumina price will moderate to an average of $310/t in 1Q-17.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.