The AFR’s Philip Baker has penned a shocker today attempting to argue that negative gearing does not push up house prices:

If the policy of negative gearing really does push up house prices, try telling that to property investors and home owners in Perth and see what sort of reaction you get.

To profit from negative gearing, your expected capital gain must be significantly higher than the interest you have paid on your loan…

If negative gearing really does force house prices higher then, in theory, there should never be a time when prices go backwards or even tread sideways.

They should always go up.But of course they don’t…

Indeed, the major reason why house prices have gone through the roof is not negative gearing but rather our record low interest rates and the high levels of debt that borrowers have taken on…

For sure incomes haven’t changed that much but they don’t have to when interest rates fall to 4 per cent from 8 per cent like they have over the past 10 years.

When that happens borrowers can double the size of their mortgage but keep their payments as a percentage of their income at roughly the same level…

As the money got cheap, we all just borrowed more and that has pushed up house prices, not negative gearing…

But the introduction of negative gearing and the discount on capital gains tax means a whole new range of investors are now dreaming of owning more than just one property.

Change that capital gains tax and it would also slow down the amount of speculating that goes on in the property market.

Baker’s arguments around negative gearing and its partner-in-crime, the capital gains tax (CGT) discount, are a classic strawman. Nobody ever said that these tax distortions were the only forces at work in house prices, nor is there any evidence that they are still not impacting prices despite the declines in Perth.

And if these distortions are not impacting prices, then why note that “the introduction of negative gearing and the discount on capital gains tax means a whole new range of investors are now dreaming of owning more than just one property” and that reforming these “would also slow down the amount of speculating that goes on in the property market”. Surely this suggests that these distortions are pushing-up demand as well as mortgage debt and, therefore, are helping to push-up property prices?

Bakers’ claim that when mortgage rates halve “borrowers can double the size of their mortgage but keep their payments as a percentage of their income at roughly the same level” is also false because it ignores the added principal repayments.

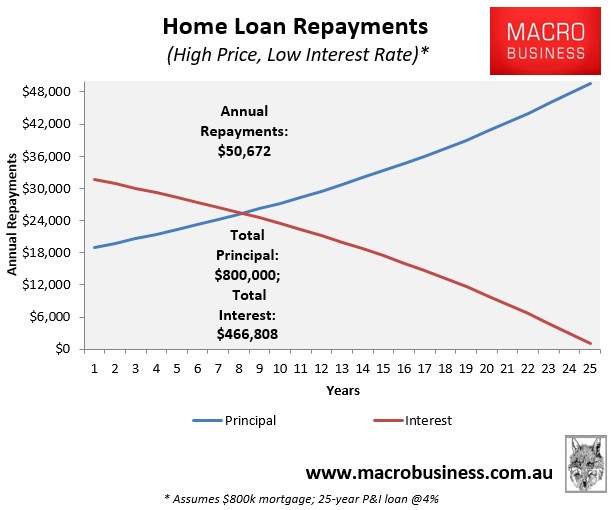

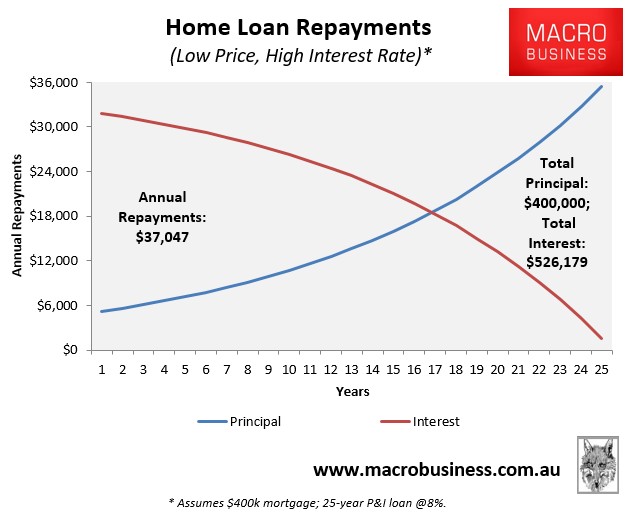

To illustrate, consider the below stylised example.

Scenario A (high price, low interest rate):

- Buyer purchases a house valued for $800,000 (assume no deposit).

- The mortgage rate is 4%, which remains the same throughout the 25 year loan-term.

Scenario B (low price, high mortgage rate):

- Buyer purchases a house valued for $400,000 (assume no deposit).

- The mortgage rate is 8%, which remains the same throughout the 25 year loan-term.

The below charts show the repayment schedules for both mortgages:

As shown above, a buyer under scenario A ends up with a far higher repayment burden. Why? Because while their initial interest repayment is the same, they are required to repay an extra $400,000 in loan principal over the 25 year term. Hence, halving the mortgage rate does not justify a doubling of home prices.

Ultimately, there are a whole bunch of factors that influence Australian house prices. These include such things as:

- Immigration levels;

- Tax policies (e.g. negative gearing and the CGT discount);

- Demand from foreign investors;

- Interest rate settings;

- Land-use and planning policies; and

- Infrastructure investment.

While Labor’s policies around negative gearing and the CGT discount are certainly no panacea, they represent a material improvement over the status quo and the Coalition’s do-nothing approach.