by Chris Becker

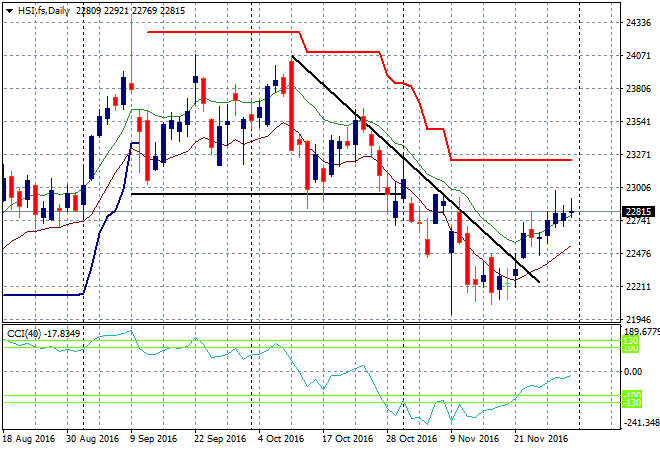

Asia stock markets could not translate a positive, yet weak lead from US stocks to something substantial today with falls across the region as Japanese industrial production output unexpectedly slumped. The Shanghai Composite is down nearly 1% after lunch as market regulators tried to stamp down the speculative edge (read: entire edifice) that has crept in. The Hang Seng in comparison is up 0.3% to 22814 points with the daily chart slowly sneaking up to resistance around the 23000 point level:

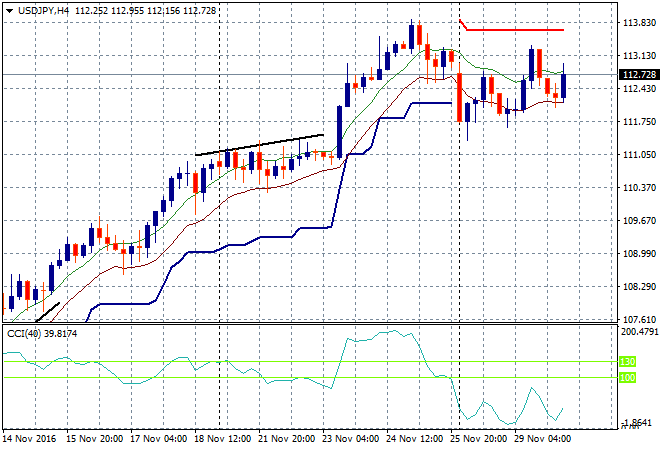

In Japan, share markets have finished stagnant with the Nikkei putting in a scratch session to finish at 18308 points, as the USDJPY bounced back above the 112 handle, finding some temporary support here going into the London session. I’m watching the intraweek high just above the 113.10 area for signs of a return to favour for USD:

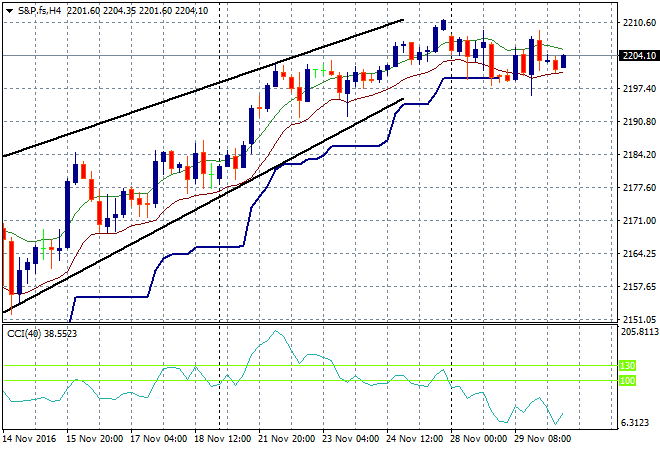

S&P Futures are steady as the US markets consolidate post the epic Trump run, with support firm at the 2200 point level:

The ASX200 fell 17 points or 0.3% to 5440 points led by the decline in iron ore miners, particularly Fortescue and BHP, down 5% and 4% respectively as Dalian prices fall limit down.

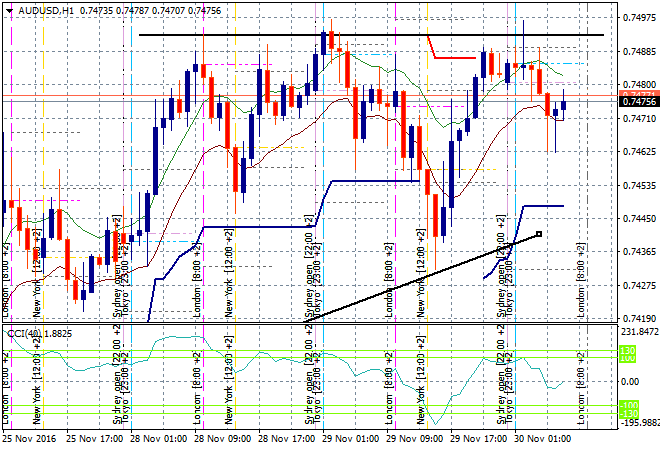

The Aussie dollar is hitting a wall against the 75 cent level in USD, steadying at 74.50 going into the more voluminous session overnight:

The data calendar tonight is pretty full of red flags starting with the Bank of England financial stability report that will push Pound around significantly, followed by German unemployment and EZ wide CPI prints later in the evening – both Euro sensitive. Before the US session, Mario Draghi is having an important speech in Madrid and then we get US personal consumption expenditure – i.e the fragile centre of the US economy!

To finish the night, the oil sheiks from OPEC give their final press conference from Vienna…