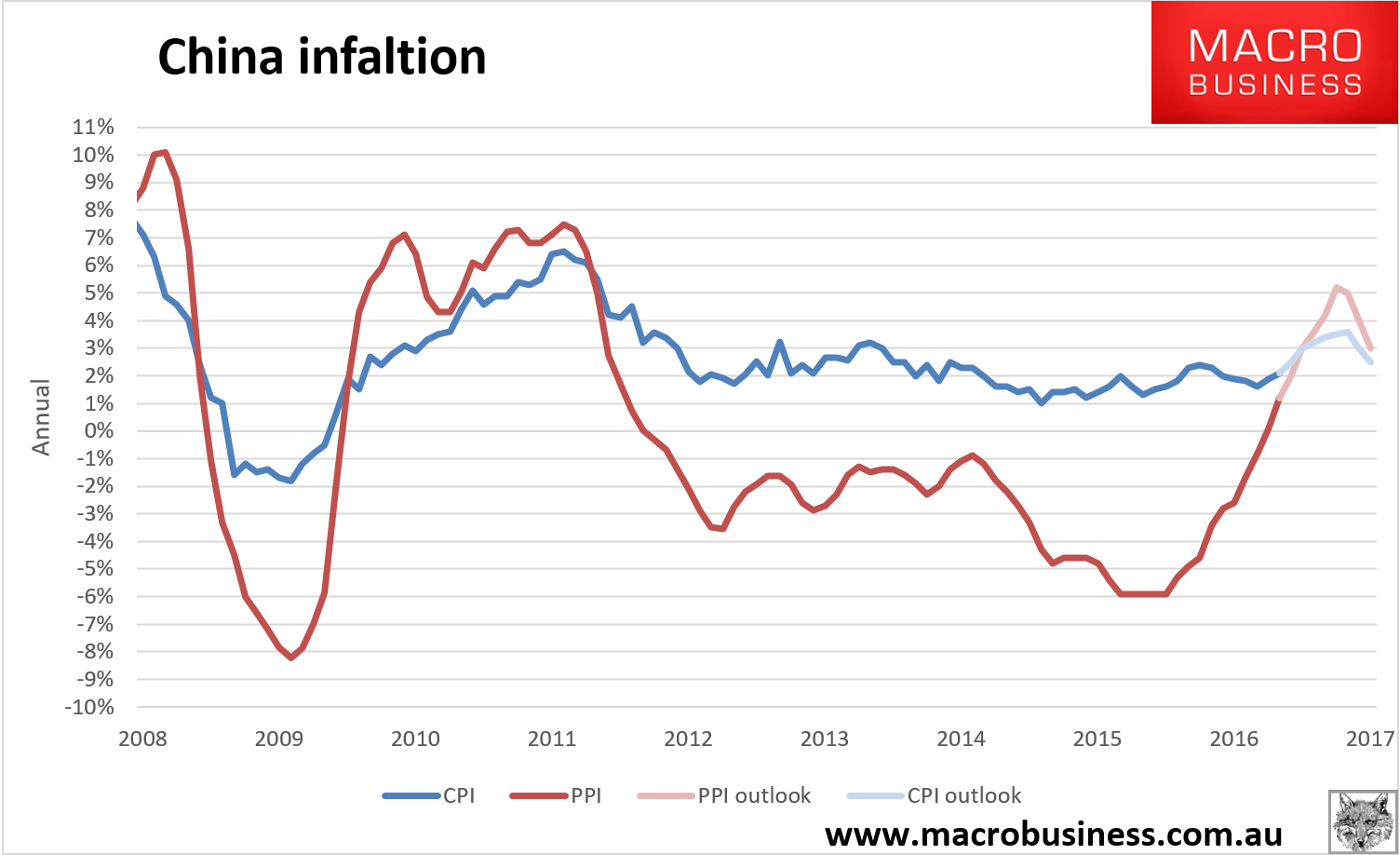

China’s key inflation gauge consumer price index grew at its fastest pace in six months in October as food prices rose, while factory prices beat market expectations to accelerate to a 55-month high, fanning concerns of inflation.

The October CPI data ended previous drops in the past five-consecutive months starting from 2.3 percent in April, when the CPI hit its highest level since July 2014, according to the National Bureau of Statistics (NBS)on Wednesday.

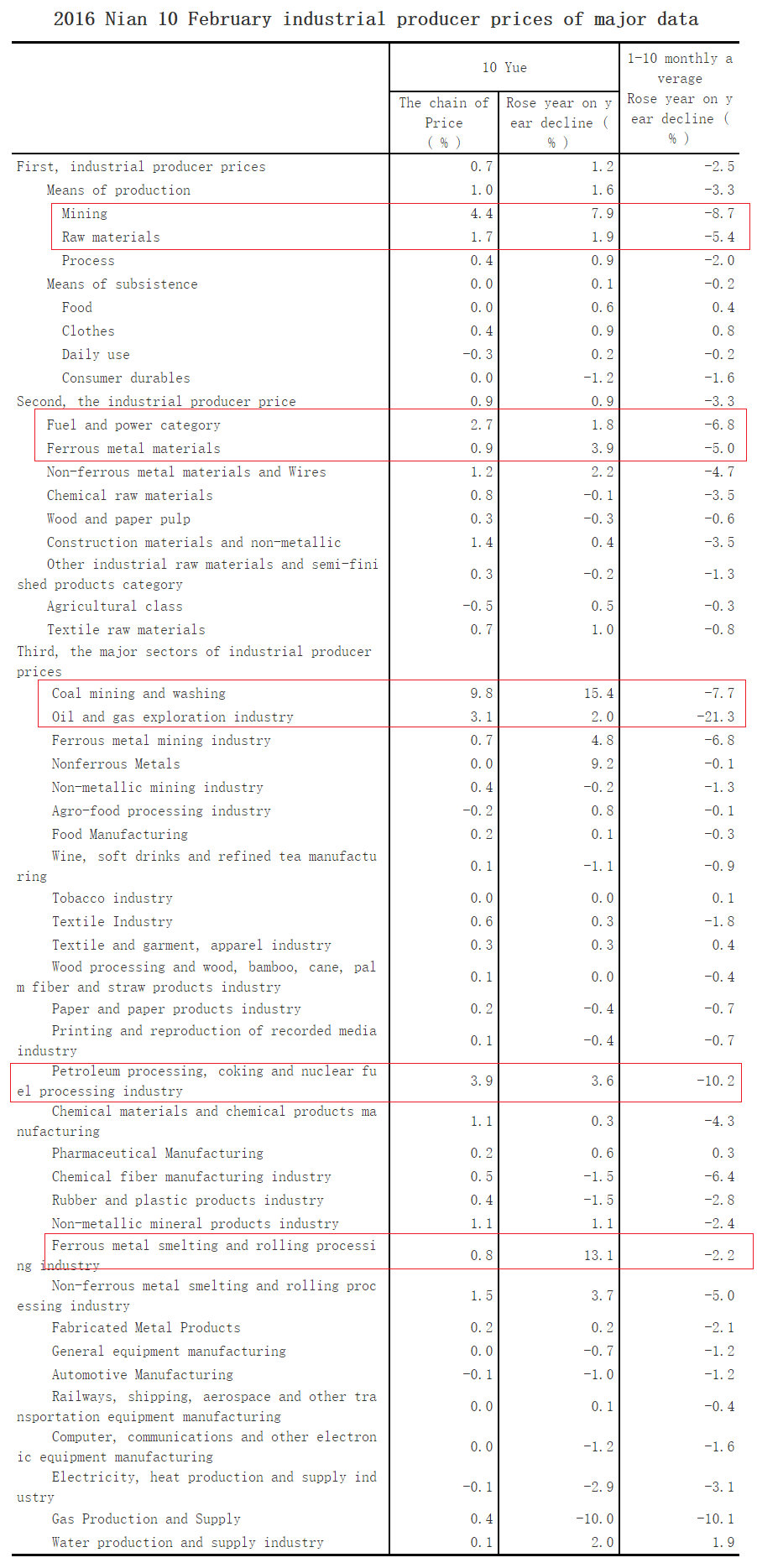

The producer price index (PPI) rose 1.2 percent year on year, the fastest pace since December 2011 after negative growth for the previous 54 months by rising 0.1 percent in September.

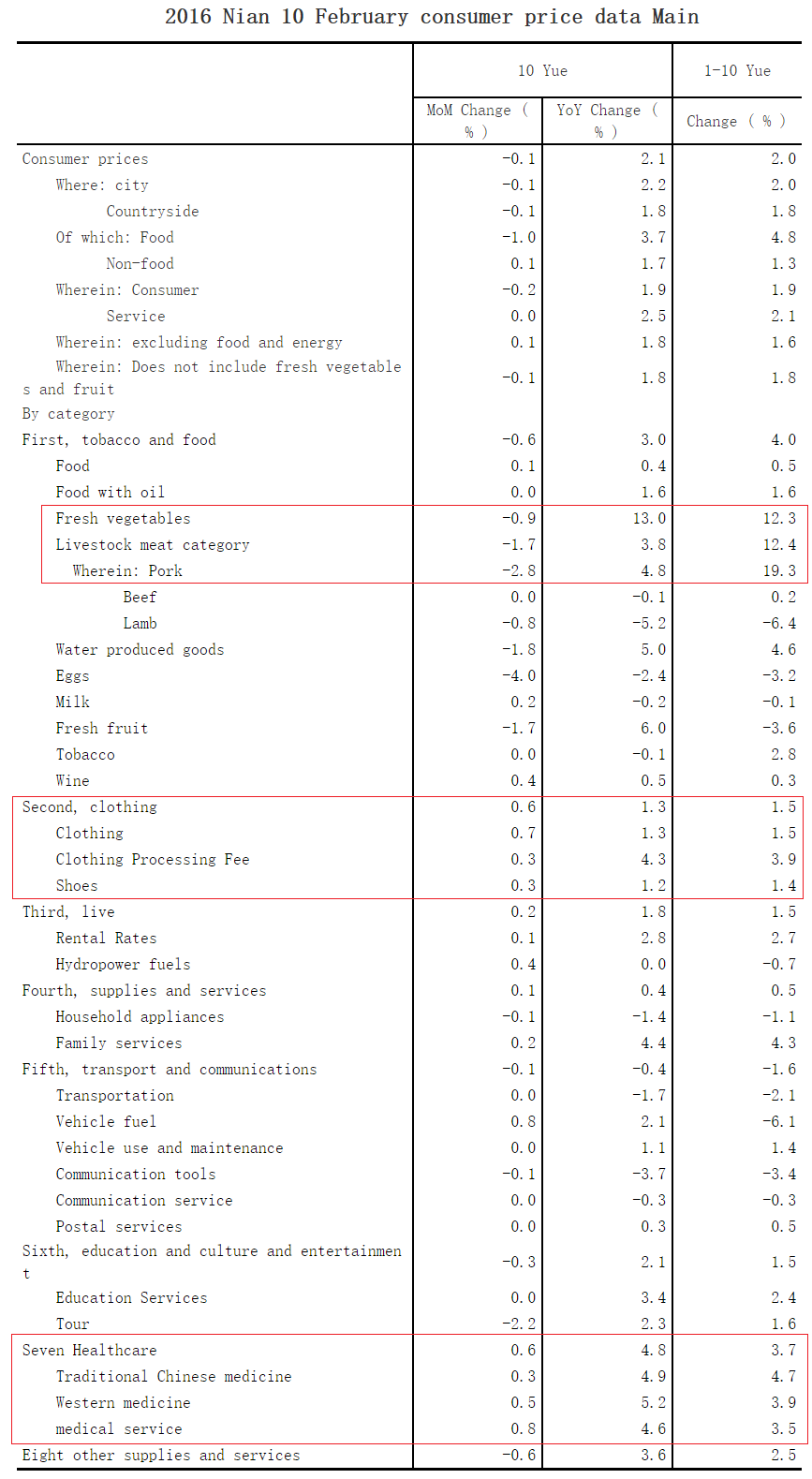

In addition to the lower comparison base of last year, food prices rises fueled faster consumer inflation in October. Food prices rose 3.7 percent, compared with a 3.2 percent gain the previous month.

The recent soaring garlic price is a case in point. The whole sale and retail price of garlic surged by 90 percent and 67.9 percent in October year on year, while month-on-month growth was over 6 percent and about 5 percent respectively.

Meanwhile, the acceleration in PPI growth is closely linked to higher prices in some key industries like coal mining and washing, according to a NBS statement.

Prices in the coal mining and washing industries increased 15.4 percent year on year, the highest since July 2012, while ferrous metals metallurgy and rolling saw a price increase of 13.1 percent over the previous year.

The Bohai-Rim Steam-Coal Price Index, a gauge of coal prices in north China’s major ports, rose to 607 yuan per tonne last week, the 18th-consecutive rise and over 60 percent up from the start of the year.

The rising CPI and PPI, evidenced by garlic and coal prices jumps, raised concerns of short-term high inflation.

The price of pork, a key consumer price driver, could rebound in the future after falling since June and factors including rising prices of coal and steel might lead to continuous rises in PPI, according to Deng Haiqing, chief economist with JZ Securities.

However, Shi Dalong, analyst with Suning Finance Research Institute, said it was to early to be predicting inflation.

Shi pointed out that the vegetable shortage and other agriculture produce price rises could be due to natural disasters and speculative investors while China’s overcapacity cut campaign contributed to coal price hikes.

There would be some short-term inflationary pressure, but as property and car purchase demands fall due to policy changes, the overall price level would run within a proper range, Shi added.

Advertisement

A very good article that perfectly captures the dynamics. Energy and steel are driving the inflation burst:

And food in the CPI:

Advertisement

The price rises are narrow but they are in such fundamental inputs into the Chinese economic machine that you do not know where the inflation will burst out over time. Hence this, from Bloomie:

China’s once again trying to restrain its commodity traders following a spike in prices from coal to rubber, six months after the government stepped in to deflate a speculative bubble.

The Shanghai Futures Exchange urged investors to trade rationally and maintain market stability amid an increase in volatility of some contracts. The bourse increased fees for steel and rubber futures Tuesday, while Zhengzhou Commodity Exchange raised charges for thermal coal for the fourth time in less than three weeks and Dalian Commodity Exchange hiked transaction fees for coking coal and coke. Separately, the publisher of a key coal benchmark suspended two price indexes.

…Separately, Shanxi-based Sxcoal.com suspended publication of two of its indexes because they were deemed to be incomplete or not rigorous enough and causing “unnecessary” swings in prices. Sxcoal.com temporarily paused publication of its CCI5500 and CCI5000 indexes, which track benchmark thermal coal prices at the port of Qinhuangdao, the company said in a statement on its website on Tuesday. The indexes have been reflecting “partial” spot transactions, which was causing price volatility, the publisher said.

…“It shows that the government is determined to rein in coal prices and one of its measures is to curb speculative activity on the futures market,” Yu Jie, a Shanghai-based analyst with Galaxy Futures, said by phone. “In the near future, the thermal coal contract probably wouldn’t rise above the high reached on Monday.”

Zhengzhou will adjust transaction fees for same-day trading on thermal coal contracts to 30 yuan ($4.42), effective from Tuesday night trading, the exchange said in a statement on its website. It will charge an additional 30 yuan per contract on transactions with trading volume exceeding a certain level, starting from night trading on Nov. 11. Dalian will raise coking coal futures margin requirements by 11 percent, it said in a statement.

Yet coking coal and iron ore future are limit up again overnight. It is spreading into other base metals. The trade is being driven by the falling yuan as local speculators that can no longer get their money out owing to capital controls are piling into US dollar related assets at home. They are clearly spooked that the yuan will fall even faster with Trump in the White House, probably with good reason. Recall recent Goldman thoughts:

Advertisement

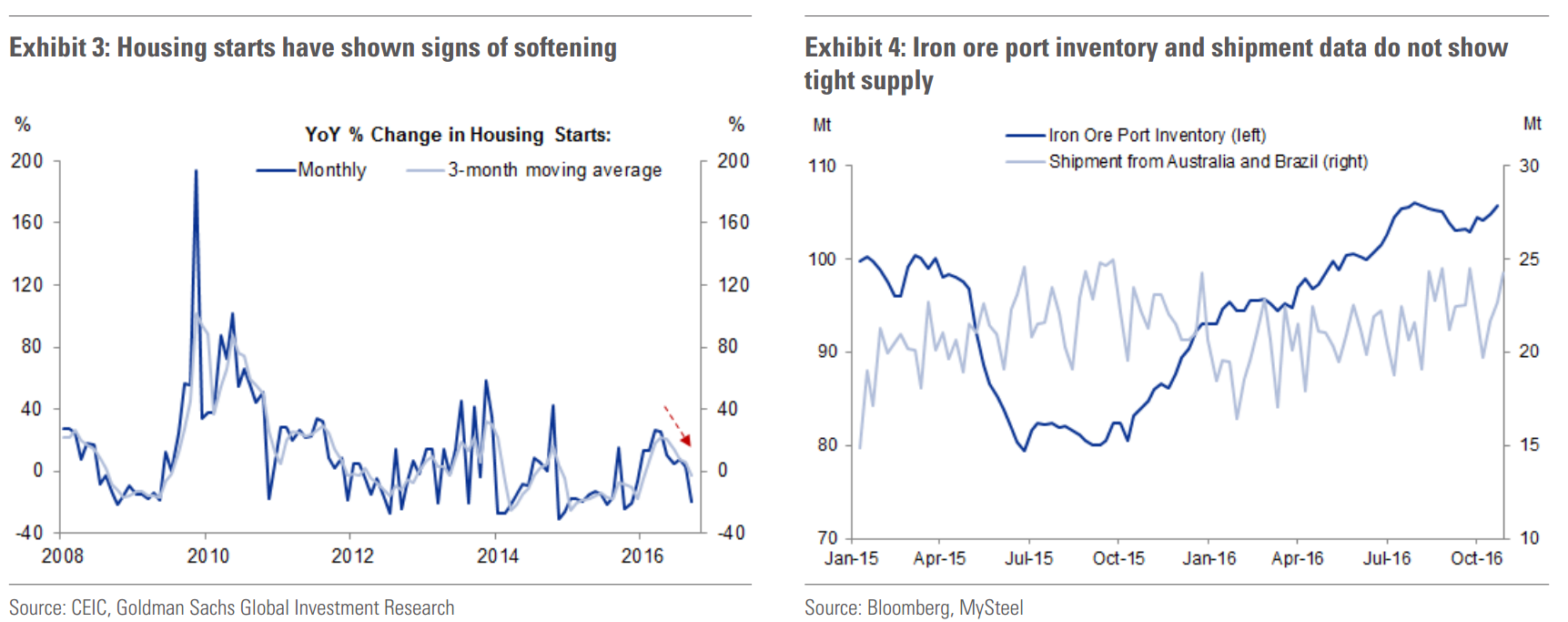

There are reasons why iron ore may be the first in line to benefit from onshore investment flows into commodities amidst renewed CNY depreciation. For example, the iron ore futures curve is almost always backwardated, making long iron ore a positive-carry trade. To the extent that a higher $/CNY also leads to a weaker local currency on a trade-weighted basis, iron ore may benefit from potentially higher Chinese steel exports. Additionally, rebar and iron ore are the most traded commodities in the onshore futures exchanges. Exhibit 8 shows the positive correlation between iron ore futures trading volumes and the $/CNY in recent months. By our estimates, about 60% of the iron ore price rally in October can be explained by the CNY depreciation.

In summary, contrary to the market chatter and media report on higher coal prices driving higher iron ore prices, we think that $/CNY has played a more important role. Going forward, we see further room for CNY depreciation given the high likelihood of Fed hiking in December. With ample onshore money supply chasing a limited menu of accessible dollar-linked assets, continued CNY depreciation means that iron ore prices may stay above what the fundamental demand and supply suggest in coming months.

Chinese hedge funds are providing margin finance for leveraged bets on the country’s booming commodity futures market, in an echo of the practices that led to last year’s stock market boom and bust.

…Rising commodity prices have in turn fuelled speculation in the futures markets. Trading volume in front month coking coal futures in Dalian hit 7.6m in October, the third-largest month on record behind March and April, when China was first gripped by a commodities frenzy.

Commodity trading has surged in China as retail investors, rich individuals and wealth managers use the sector as a quick and easy way to place leveraged bets on the domestic economy or government reforms.

The surge in speculation activity has rattled global commodity markets, causing a sharp run-up in the price of raw materials such as steel and iron ore futures. That has astonished western trading houses and analysts accustomed to following the fundamentals of supply and demand.

Some hedge funds are using structured investment products to provide margin loans to investors looking to ride the futures boom. Hedge funds generally buy the senior tranche, which promises a fixed return. Punters buy the equity tranche, which pays fixed returns to the senior tranche as interest on the margin loan. After the interest is paid, punters keep any additional profits from the futures trade.

A hedge fund manager in Shanghai said: “These are hedge funds looking for fixed returns. They’re not familiar with commodities, so [this] strategy looks good to them. Someone else takes the big risk.”

But this form of margin lending, known in Chinese as peizi, mirrors the type of shadow bank-style margin financing that helped fuel the Chinese stock market boom last year. Once the market turned, margin calls amplified losses as investors were forced to liquidate their holdings to repay loans.

Regulated margin lending through securities brokerages for stock market investment caps leverage at Rmb2 of borrowed funds for every Rmb1 of the investor’s own money. The 21st century Business Herald reported on Wednesday that peizi for commodity futures investment can reach as high as 4:1.

An official at the National Development and Reform Commission, China’s top economic planner, told state media this week that recent increases in coal prices are “irrational”, citing speculation as one explanation.

A trader at a futures brokerage in Shanghai said: “The speculative element in the market is very big right now. End users and those trying to do hedging are getting killed.”

Advertisement

This is the wildest bubble that I’ve seen in bulk commodities in my decade-long coverage of such. With the Trump ascendancy and a strong USD, LA Nina building to inhibit supply, and China still short of coking coal there is no reason for it to stop.

Authorities will have to keep tightening until it bursts. If not they risk having to pull the handbrake on the entire economy a little later.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.