• President-elect Trump’s proposals, if enacted, would have significant implications for the US economic outlook over the next few years, some positive and some negative. The positive fiscal impulse from his tax reform and infrastructure proposals could provide a near-term boost to growth and, depending on the specifics, could have positive longer-run supply side effects.

• However, other proposals could lead to new restrictions on foreign trade and immigration, which could have negative implications for growth, particularly over the longer term. …

• We expect scaled-down versions of the tax reform and infrastructure policies to be enacted. We do not anticipate significant changes on immigration policy, but incremental restrictions seem likely. Mr. Trump’s monetary policy views are still unclear, but slightly more hawkish appointments appear likely at this stage. Trade policy is the greatest unknown, but we expect that Mr. Trump would follow through on at least some of the trade policies he has outlined.

• Keeping in mind that our simulations are subject to considerable uncertainty, we draw three main conclusions. First, Mr. Trump’s policies could boost growth in 2017 and 2018, but are likely to weigh on growth thereafter if trade and immigration restrictions are enacted, or if Fed policy turns more restrictive. Second, core inflation and the funds rate are likely to be higher for the next few years in almost all scenarios. Third, the risks around our base case appear asymmetric: a larger fiscal package could boost growth moderately more in the near term, but a more adverse policy mix would likely lead to a significant slowdown, higher inflation and tighter policy in subsequent years.

And on the USD:

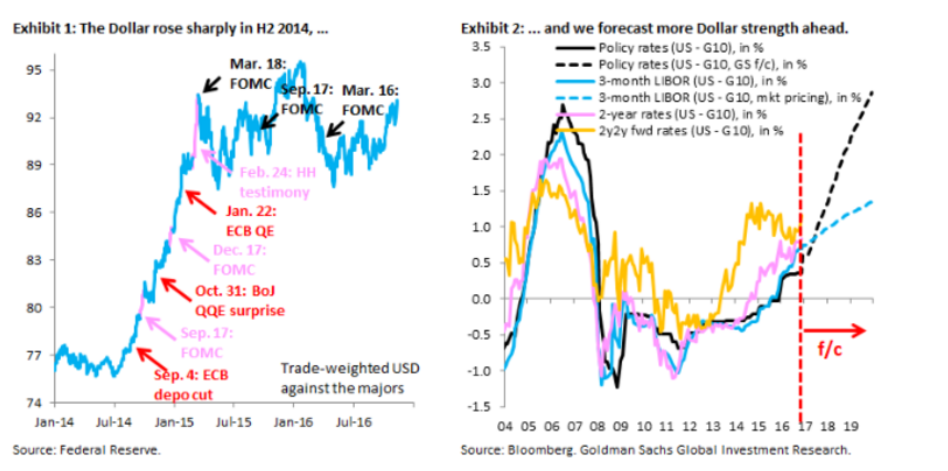

We discuss our dollar outlook in the wake of the election, with many asking if USD strength in recent days can extend. We think so and see the election as something of a “reset.

Going into the election, the Dollar fell whenever odds of a Trump victory went up, in particular on the FBI disclosure of additional Clinton emails. As early signs of a Trump victory made their way into the markets during the night from Nov. 8 – 9, the Dollar fell in line with this pattern, but reversed sharply as President-elect Trump began giving his acceptance speech, which projected a conciliatory and inclusive message. This set off a rally in risk, which has morphed into markets trading a positive growth shock to the US: Dollar up, inflation breakevens up and SPX up.

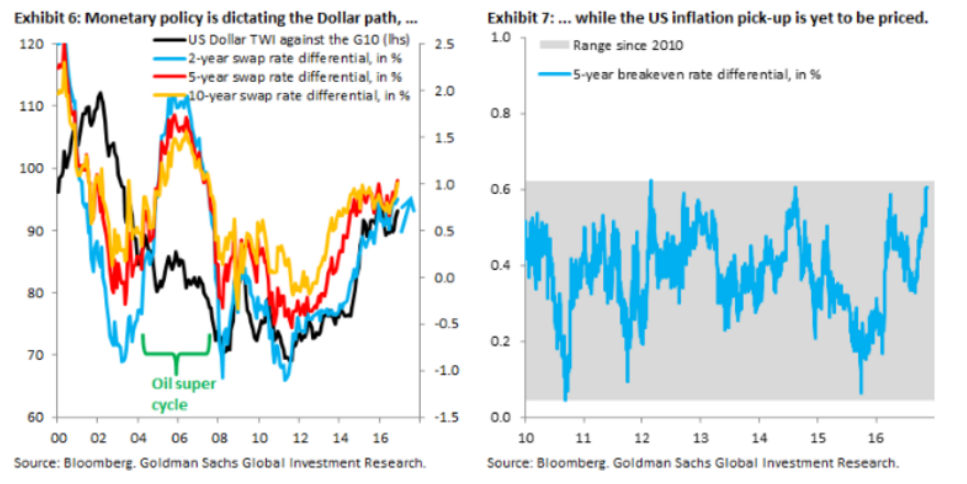

Amid substantial uncertainty, our US team has kept is growth forecast unchanged. There is upside risk from the fiscal stimulus, while there is downside risk from an escalation in protectionism. But in either case, inflation is likely to be higher than before, which is what has probably helped drive inflation breakevens up. As a result, market pricing for Fed hikes has risen sharply, with tightening priced through Sep. 2019 now 86 bps, almost a full hike more than at points before the election.

Our point here is not that risks don’t exist. Of course they do. Instead, it is that the policy mix has shifted in the direction of more inflation, which means that – given how dovish market pricing has been – there is room for the Dollar to catch up with where it should have been quite some time ago.

Our US team forecasts three hikes next year in addition to the one now likely in December. This is more than double what is priced and underpins our forecast for the Dollar to rise around 7 percent on a trade-weighted basis over that horizon.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.