The Chinese property cycle is starting to turn, mid-17 headwinds on the way

A key part of the 2016 recovery in metals demand has been the relative strength in the Chinese property market contributing to a more commodity-friendly growth environment. However, all good things much come to an end, and as per notes from our China economics and property team published today, we feel the cycle is at a turning point.

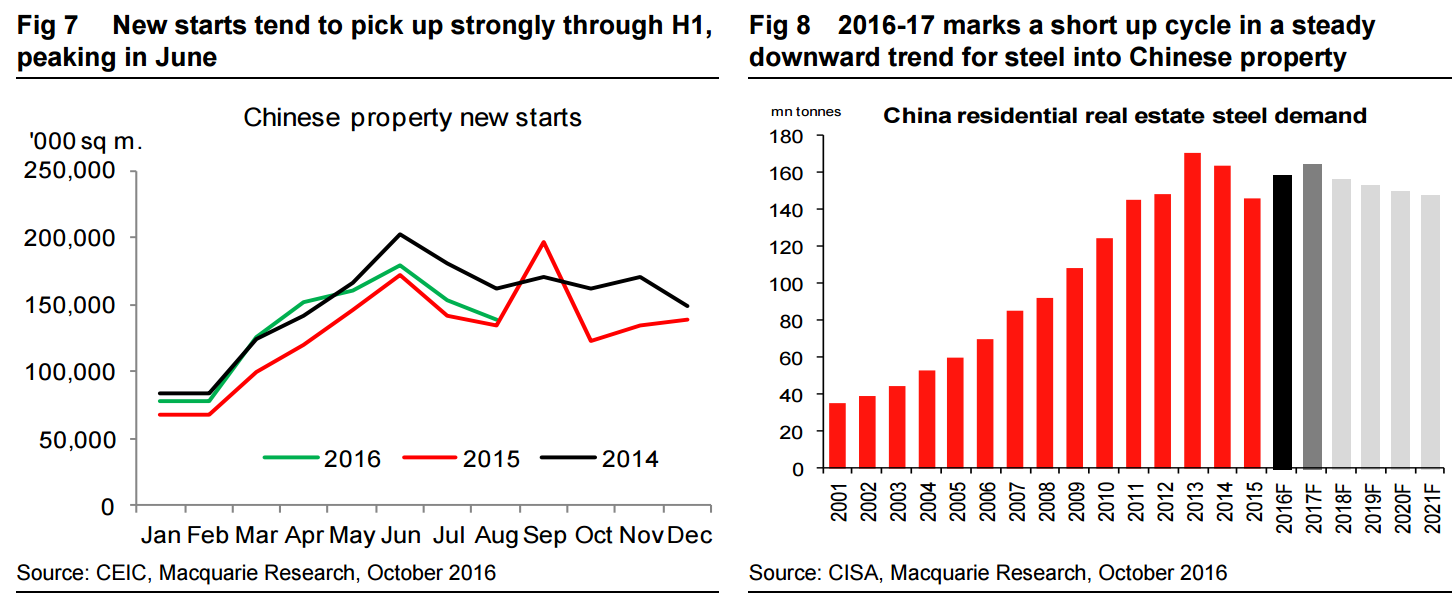

While we expect sales volumes to fall by 10% next year, we still expect some positive momentum in starts for H1 2017 owing to cashed up developers and a need to underpin growth, supporting sequential metals demand out of Chinese New Year. However, this tailwind is likely to be fading into mid-year.

This reinforces our view that we are in a window of opportunity for metals and bulk commodity producers. And the turn in the property cycle shows this window is starting to close. How management teams react to this environment in terms of medium-term strategy will be a key differentiator for what could be a more difficult 2018. Key questions around China property and metals/bulks markets

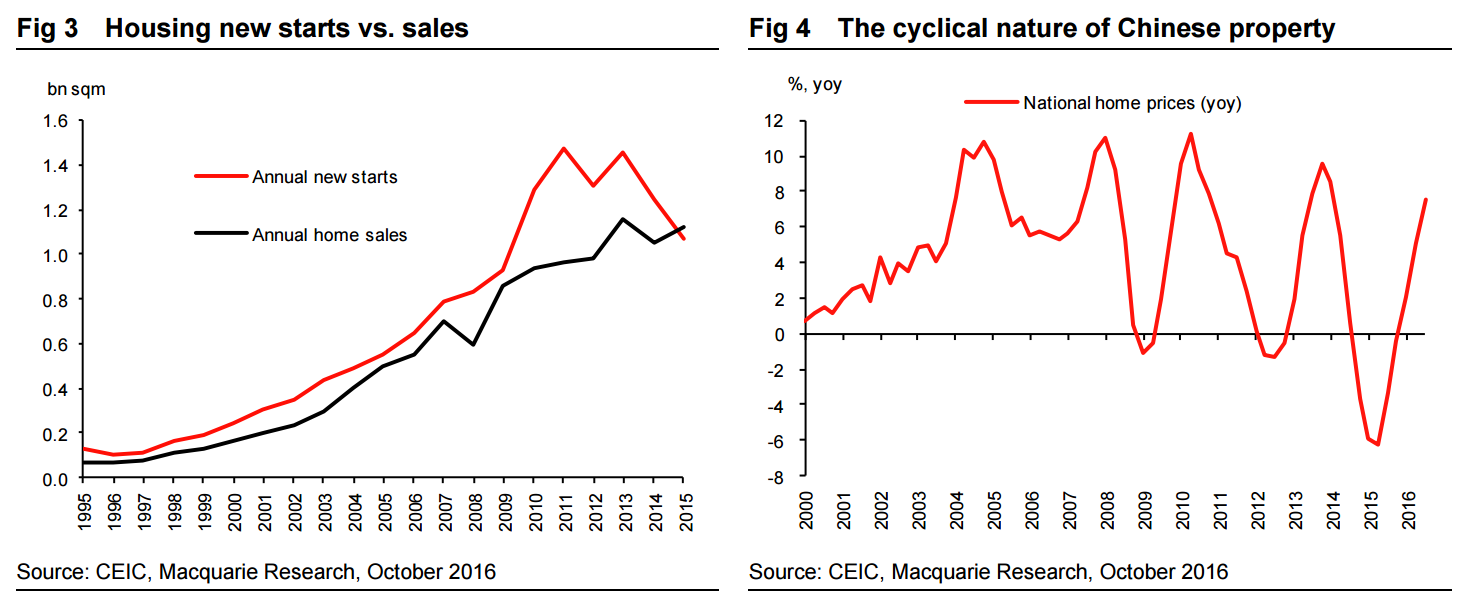

How has the construction market helped commodity demand? China’s renewed fixed asset investment push has been core to the demand improvement. Every RMB spent in infrastructure and construction in China is more commodity intensive than one spent elsewhere in the economy. The construction market has responded strongly to the surge in sales, with a 12% YoY gain in new starts following on from higher-than-expected sales (even than our +15% target for 2016).

Is the housing market vastly overbuilt? No. Our China economist Larry Hu believes the main problem is a supply/demand mismatch, not overinvestment. In other words, areas with high demand have inadequate housing supply, while areas with low demand remain in oversupply. This stems from decisions made 3-4 years ago when the State Council basically got the urbanisation pattern wrong. The expectation was that migration to Tier 3-4 provincial hubs would accelerate at the expense of Tier 1-2 cities, hence investment was focused on these regions. In fact, the opposite occurred, with urbanisation to Tier-1 cities outpacing growth in availability.

How large is China’s housing stock, and how will this change? We estimate that the housing stock was 19bn sqm as at end-2015. Given a current urban population of 767mn, China’s per capita living space was 25 sqm in 2015. China’s urbanisation rate was 56% in 2015. Assuming an increase to 65% by 2026, this implies the urban population would increase by 170mn over the next ten years. With 25 sqm per person, this means 4.3bn sqm extra demand. Meanwhile, within the 19bn sqm of housing stock, around 3.7bn was built before 2000, when China’s property market began to take off. So the quality of these buildings is quite low. Assuming that half of this will be demolished in the next decade means 1.9bn sqm from replenishment demand. With a 65% urbanization rate in 2026, the total urban population in that year would be 937mn. If the average living space rises to 30 sqm, this means demand for another 4.7bn sqm.

Adding the three together, total demand would equal 10.8bn sqm for the next decade. In comparison, total residential housing sales could be around 1.5bn sqm in 2016. Based on these numbers, it seems that the boom days for the sector are gone, noting that the 26% growth in residential housing sales seen so far in 2016 has largely been due to the frontloading of future demand to the present. Moreover, new demand is most likely tilted toward high-tier cities, where the land supply is declining.

Why are lower land sales a problem? Land sales tend to precede new starts by six months and new starts tend to be 6-12 months ahead of project launch and sales. Weak residential land sales in 2014 and 2015, down 32% and 20% respectively, were due to cautious developers uncertain about market recovery. During 2015, starts were smaller than sales, and land sales were much smaller than starts. Unless there is a sharp drop in property sales, there is a growing chance of a shortage of property in higher tier Chinese cities on an eighteen month view, according to our China property team.

Can the government keep propping up sales? We do not believe government initiatives can stimulate a new independent category of growth from low-tier cities, meaning if top-tier cities slow down in sales, the rest of the market will likely follow. However, the Chinese government has enough policy tools to fine-tune the housing market. For example, by lowering the down-payment ratio or mortgage rates further, which proved effective in past cycles. It could also ease credit, which is useful in turning the housing market around if it becomes too much of a drag on growth.

What is the implication for key property metrics 2017? Our expectation is for property sales to fall 10% YoY in 2017, from a very high 2016 base, with this part of the cycle now turning. Starts will still see slightly positive growth over the year as a whole, with a reasonable H1 giving way to a weaker H2 owing to the lag on the cycle. Given the significant gap between starts and sales this year, this still implies a property destock over 2017 as a whole, just at a slower pace than seen this year. Completions are also likely to be slightly down YoY.

And what is the implication for metals demand? We expect the Chinese government to prolong its more commodity-intensive phase of growth through the political transition in 2017. New construction starts will still accelerate out of Chinese New Year, and when supported by ongoing strength in infrastructure will still see decent YoY apparent demand growth from China for industrial metals in H1 2017 (helped by a low base). Into H2 however, the construction sector is likely to one more prove negative for steel (and its raw materials) while rates of base metal demand growth will slow. As such, we see a relatively short window of opportunity for commodity prices and commodity producers before the demand tailwind fades. And, given the slowing urbanisation rate, the property sector is likely to be an ongoing headwind to steel demand – we see steel into residential property in 2020 at a level ~15% below 2013’s peak.

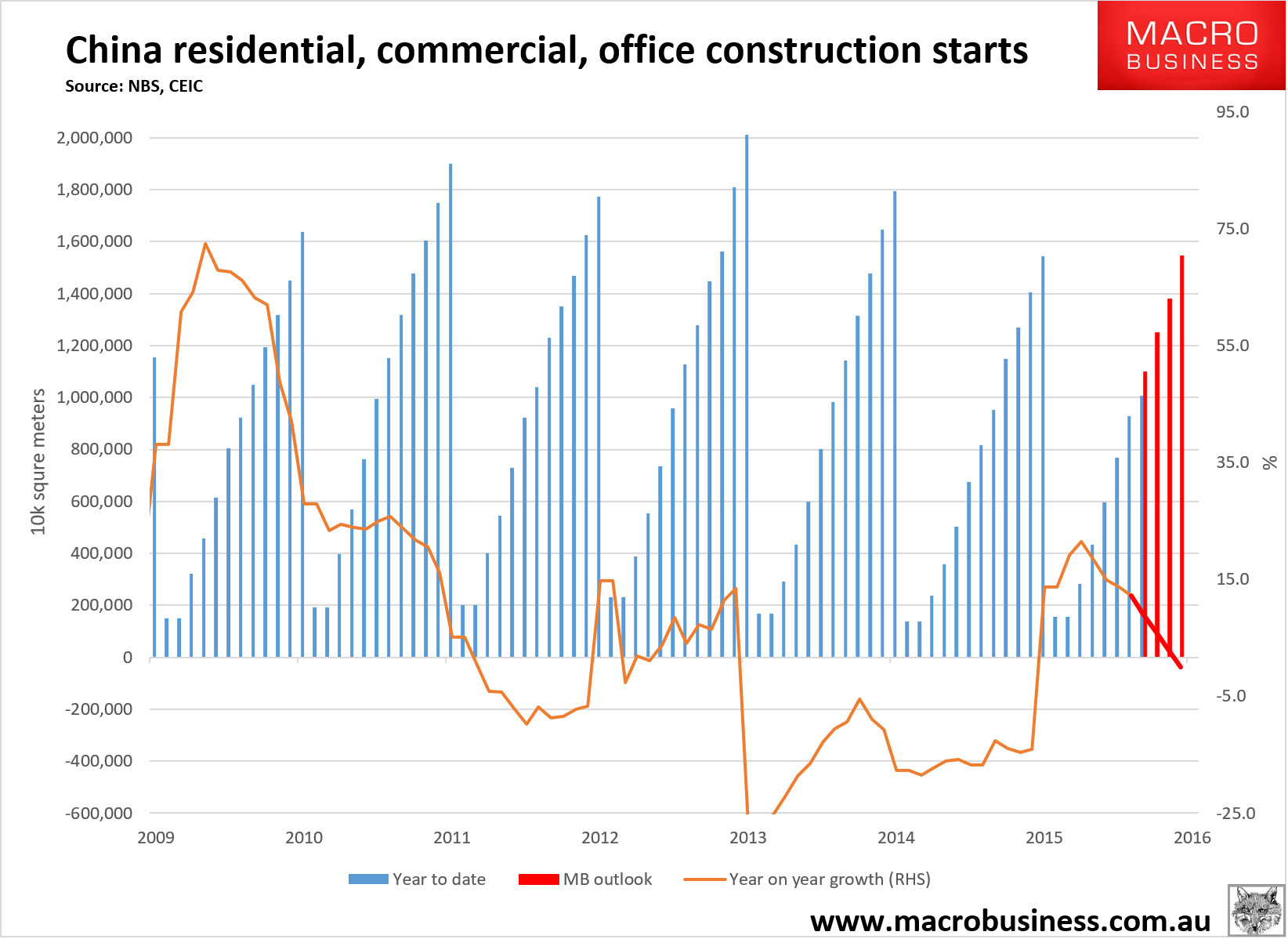

Hmmm, I see this happening six months earlier:

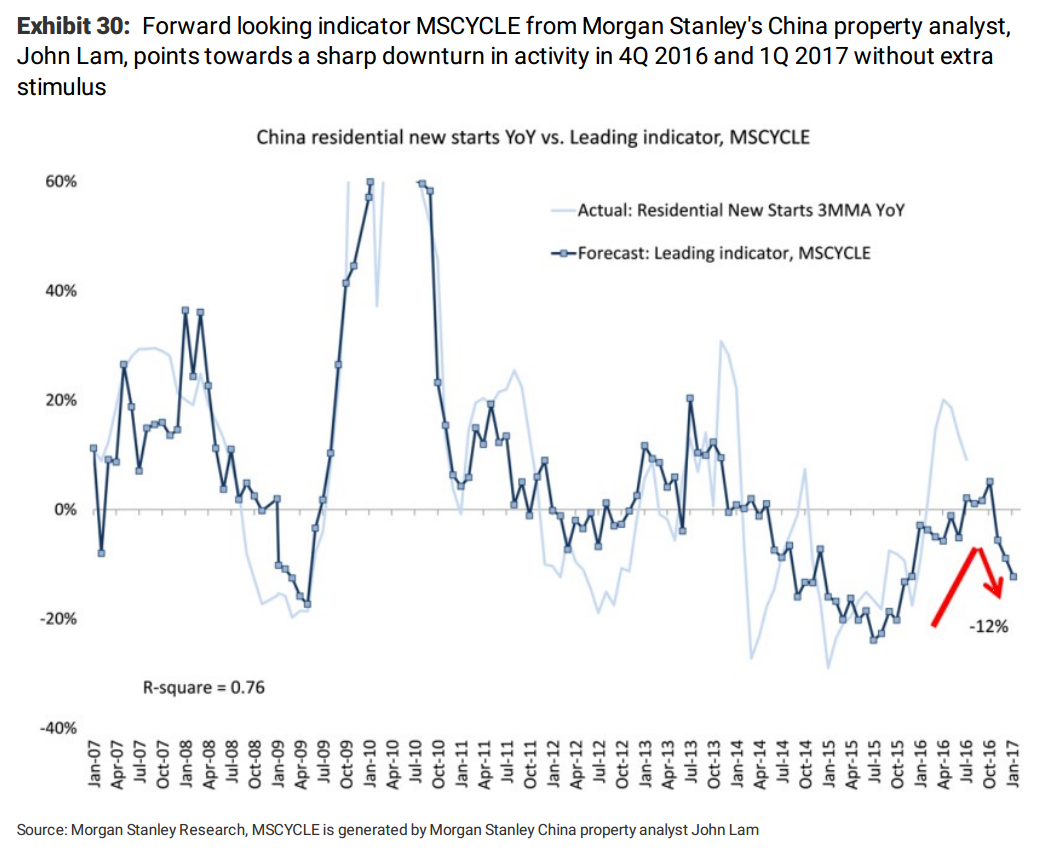

It is already apparent in the Morgan Stanley leading indicator:

Advertisement

Tomorrow’s data update may help. Either way it is coming.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.