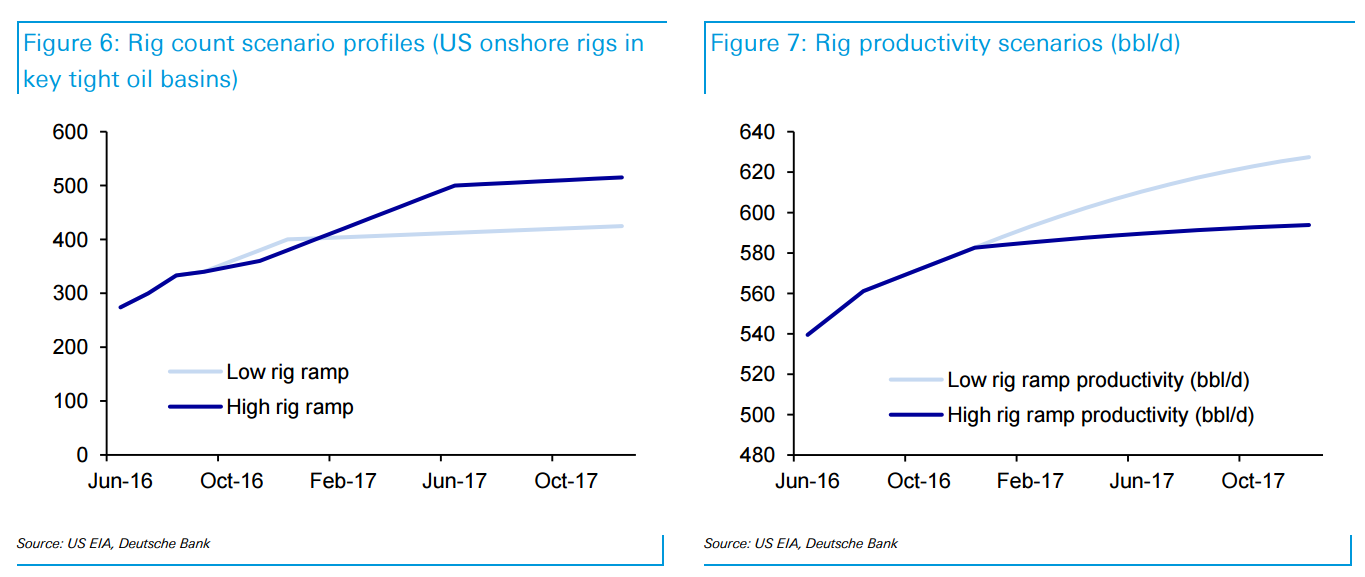

As a response to a both (i) a stronger oil-price environment and just as importantly (ii) a more reliably stronger oil-price environment, we believe a steeper increase is likely in US onshore rig activity in 2017 than we previously assumed. While our previous assumption (+5 rigs per week) have proven too aggressive relative to the recent slow-down, a resumption of this rate of increase now appears likely at some point. In our revised base-case scenario, we assume that additions currently running at +10 per month double to +20 per month from December 2016 through June 2017 and then level out. We also assume that rig productivity growth slows almost to a plateau instead of rising along the current trajectory as the effect of high-grading reverses.

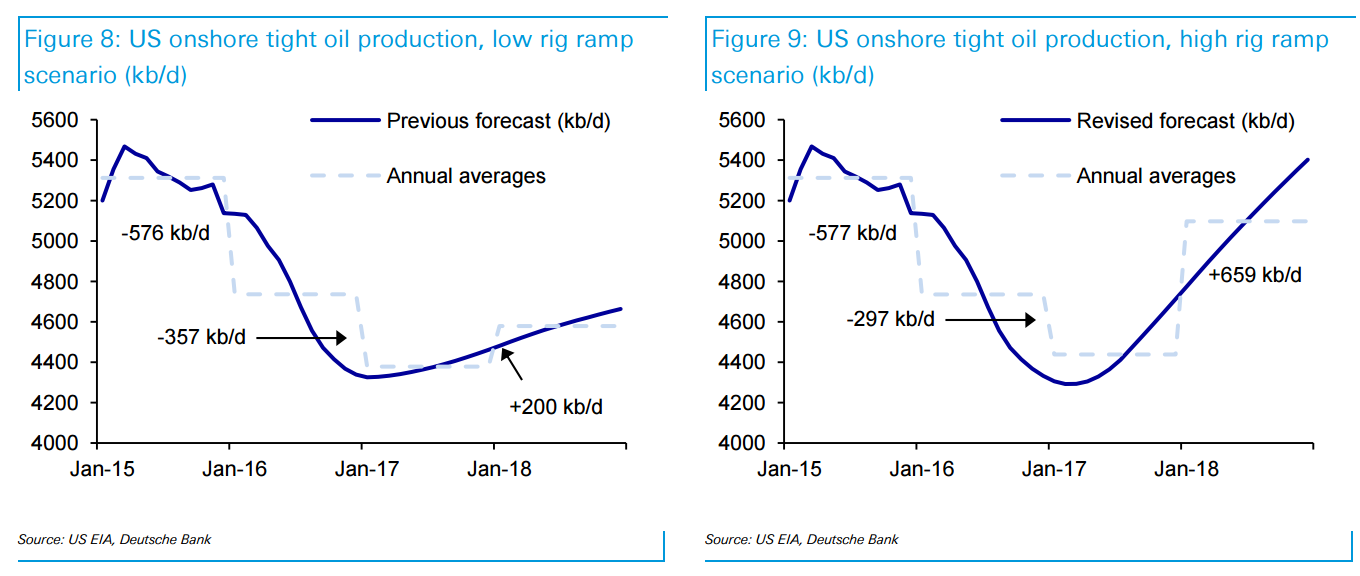

The cumulative contribution of maintaining a larger number of active rigs over a longer period of time turns into a much larger effect in 2018 than 2017. The result is that while we would see only a 60 kb/d increase in 2017 average production (from US tight oil decline of -357 kb/d to -297 kb/d) we would expect a much more significant 459 kb/d increase in 2018 average production (from US tight oil growth of +200 kb/d to +659 kb/d).

After including our assumptions for other US production After adding growth in NGLs (+240 kb/d) and the Gulf of Mexico (+90 kb/d) this still leaves headline US liquids production roughly flat in 2017 (-30 kb/d), and up +750 kb/d in 2018. The summarized inputs and resulting production forecasts are seen in Figure 6 to Figure 9.

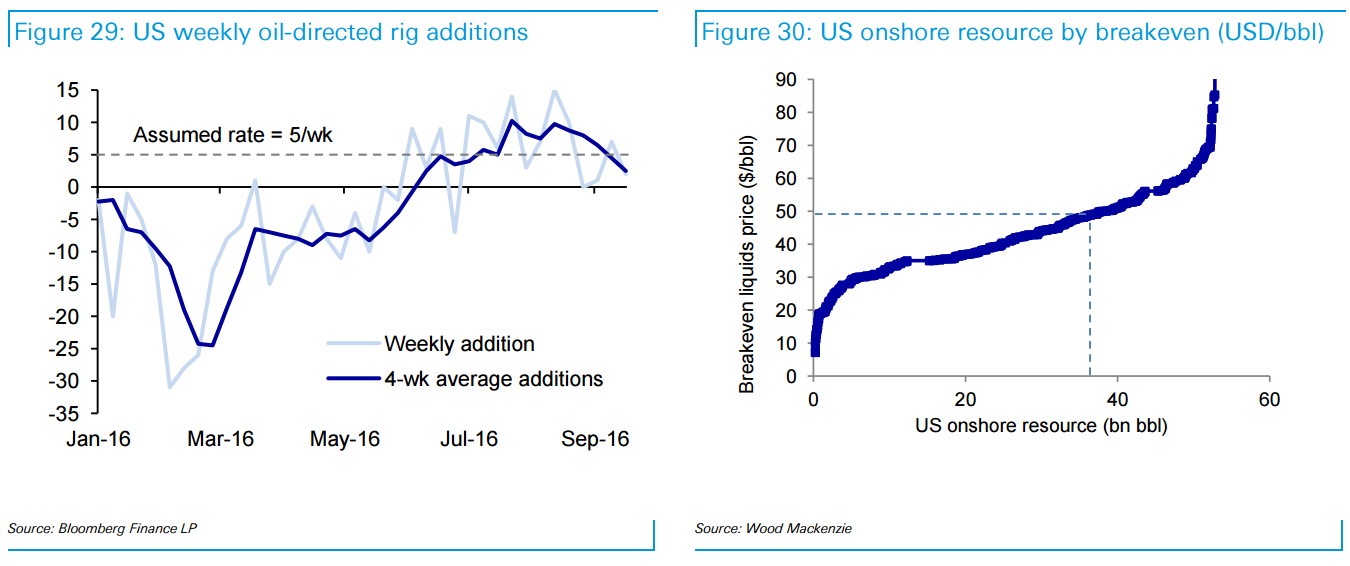

…Notwithstanding large swings in the inventory error term, the broad decline in US onshore tight oil production has largely progressed according to expectations, and could rise substantially under the high rig ramp scenario which we assume as a consequence of tighter fundamentals post-OPEC, Figure 28. Given that rigs were added at a faster-than-expected rate for most of July and August, Figure 29, and considering that we expect US Gulf of Mexico offshore production to grow by 90 kb/d in 2017, we now believe that US overall crude production may be bottoming over the course of the fourth quarter and that it will begin to show consistent growth in Q1. Given the progression of oil prices, we believe rig counts may now stabilize and show some bias towards small declines over the balance of the year, in response to the previously established 2-3 month lag to the oil price. In the US onshore tight oil sector, the overwhelming dominance of the Permian Region in terms of rig additions (accounting for 68% of additions since June) means that we expect Permian Basin production to exceed combined tight oil production from all other regions by April 2017.

Last year’s prospects for US onshore cost deflation have largely been realized. In September 2015, we stated that 32% of 2016 US tight oil assets by volume would breakeven (yielding 10% IRR) based on a -15% deflation assumption and the Cal-16 strip at USD49/bbl, while 83% of 2016 volume would breakeven at the same level on a -30% deflation assumption. Today, we revisit these metrics and see that 69% of US onshore oil-only assets totaling 36.6 bn bbl in remaining liquids reserves would be economic at or below WTI USD 49/bbl, Figure 30, suggesting that more than 15% and closer to 30% cost deflation has been achieved relative to the 2014 benchmark.

This is highly amusing stuff. If you combine the Deutsche forecast US turnaround with a rebounding Libya and Nigeria you get nearly 2mmb/d more oil versus a 0.2-0.7mmbb/d OPEC cut for 2017.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.