Late last year, Bob Birrell and David McCloskey from the Australian Population Research Institute released an explosive report examining new household and dwelling projections for Sydney and Melbourne for the period 2012 to 2022.

The report found that there would be a continuing scarcity of family-friendly housing in both cities, especially of detached housing, but an epic oversupply of shoe box apartments, particularly in Melbourne, if current construction trends persist.

The report estimated that if net overseas migration continued at 240,000 a year, and Sydney and Melbourne continued to receive almost half of these migrants, then Sydney would have to add a total of some 308,000 dwellings and Melbourne some 355,000 over the decade 2012 to 2022, with around half of this increase in demand coming from net migration (i.e. 199,000 dwellings in Sydney and 193,000 dwellings in Melbourne).

At the same time, there would be huge growth in the number of older households living in both cities. In the inner and middle suburbs of Sydney and Melbourne, 50% to 60% of the detached housing stock was occupied by older households in 2011, and the report projects that their numbers will rise rapidly. Moreover, as of 2011, the share of older households living in detached dwellings does not start to decline significantly until people reach 75 years of age.

Advertisement

The net result is that younger households wishing to start a family will find it increasingly difficult to secure a detached home with a backyard, since the stock that is available will be taken-up mostly by older empty-nesters at the same time as the number of younger households is increasing via rapid immigration.

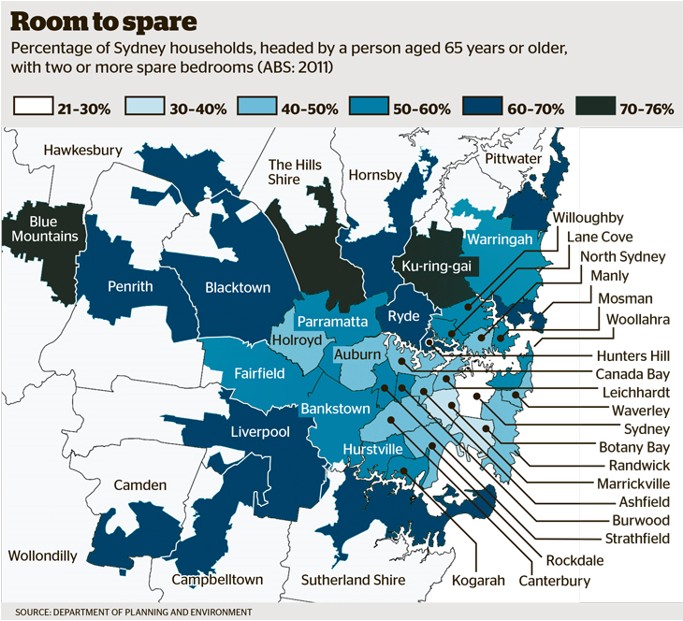

Over the weekend, the NSW Department of Planning and Environment released research showing that the equivalent of 20 years of housing supply is tied up in empty bedrooms, mostly pertaining to older empty nesters, and that this is making it increasingly difficult for young households to find “family-friendly” accommodation. From The SMH:

According to 2011 census figures, about 1.8 million bedrooms were unused across Sydney every day. This equated to 20 years’ worth of housing supply based on 30,000 new housing completions each year…

The research highlighted the potential benefit to the city’s housing supply if some homeowners chose to live in smaller dwellings, allowing young families to fill the larger houses. But efforts to encourage this shift were thwarted by a lack of alternative options, Planning Minister Rob Stokes said…

Couples who remained in larger homes involuntarily effectively prevented the “freeing up of larger homes for the next generation of families”, the study concluded…

Advertisement

For mine, these reports highlight four important issues.

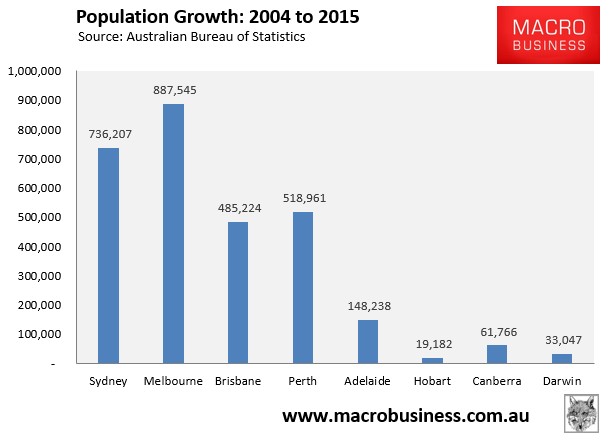

First, the immigration intake needs to be tightened significantly. Much of the added demand for housing is coming from new migrants (see next chart), which are causing severe housing indigestion and congestion, particularly in Melbourne and Sydney, thereby lowering the living standards of pre-existing residents (especially younger generations).

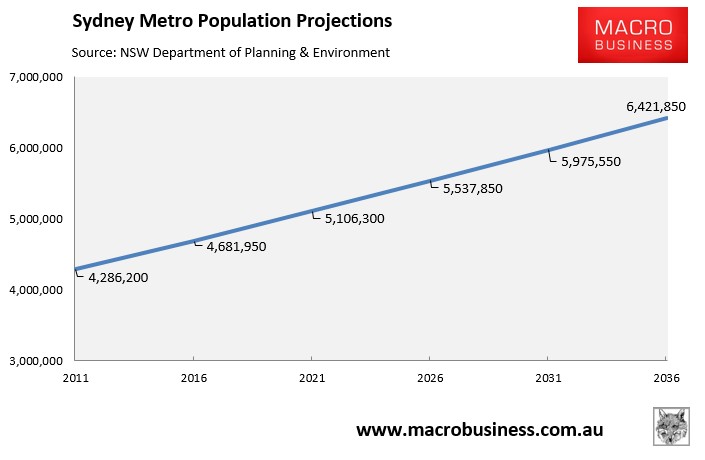

Sydney’s population is projected to rise by 85,000 people per year to 6.4 million over the next 20-years – effectively adding another Perth to the city’s population:

Advertisement

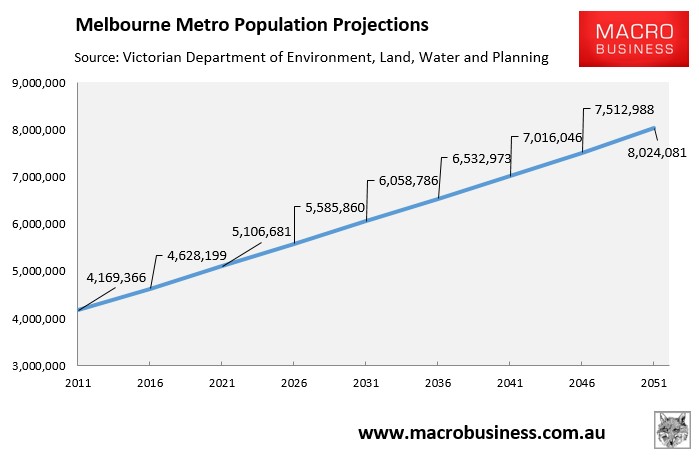

For its part, Melbourne’s population is projected to balloon by nearly 75% over the next 35 years to more than 8 million people:

Advertisement

With the flood of new migrants projected to inundate Sydney and Melbourne, finding a family-friendly home will become ever more difficult.

Second, one’s owner-occupied residence needs to be brought fully into the assets test for the Aged Pension.

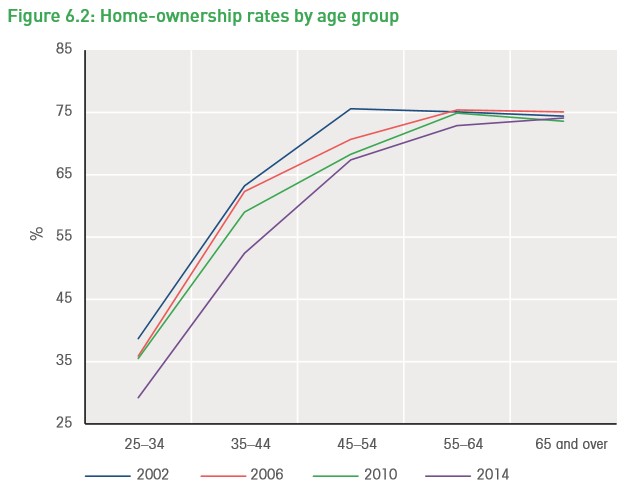

It is the height of unfairness that the biggest asset most households retiree with is largely excluded from their capacity to fund their own retirement. And it is especially unfair to expect younger generations – who are either struggling under the weight of the high mortgage debt legacy they inherited or unable to afford a home altogether (see below chart) – to bare the full cost of their parents’ and grandparents’ retirement while they live in homes they themselves cannot afford.

Advertisement

The Aged Pension should, therefore, be modified to provide less taxpayer assistance to wealthy home owners and more assistance to renters, via:

Including one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

Once implemented, raising the overall assets test for the Aged Pension, and the base rate as well.

Extending the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HELP-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Advertisement

Including the family home in the pension assets test – along the lines explained above – would also encourage empty nesters to downsize to smaller accommodation, thus freeing-up larger family-friendly homes for young families.

Third, stamp duties should be replaced by a broad-based land tax. In addition to vastly improving tax efficiency, such a tax shift would encourage households to move to homes that best suit their needs by removing the punitive tax on moving (stamp duty), encouraging the highest value use of land, and penalising land banking and vagrancy.

Finally, artificial constraints on fringe land supply should be abolished, along with better provision and funding of housing-related infrastructure, and replacing the “first-user-pays-all” tax on new housing with long-term bond financing recovered through rate payers over time.

Advertisement

If the Government is going to persist with a high immigration intake, the least it can do is facilitate this growth via an adequate release of new land and the provision of housing-related infrastructure.

Without policy change, Australia’s young families are facing lower living standards than their forbears, and the unenviable reality of raising their kids in dog box apartments and townhouses while they support their parents as they live in homes that they will never afford.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.