This will be no surprise to MB readers, from Morgan Stanley:

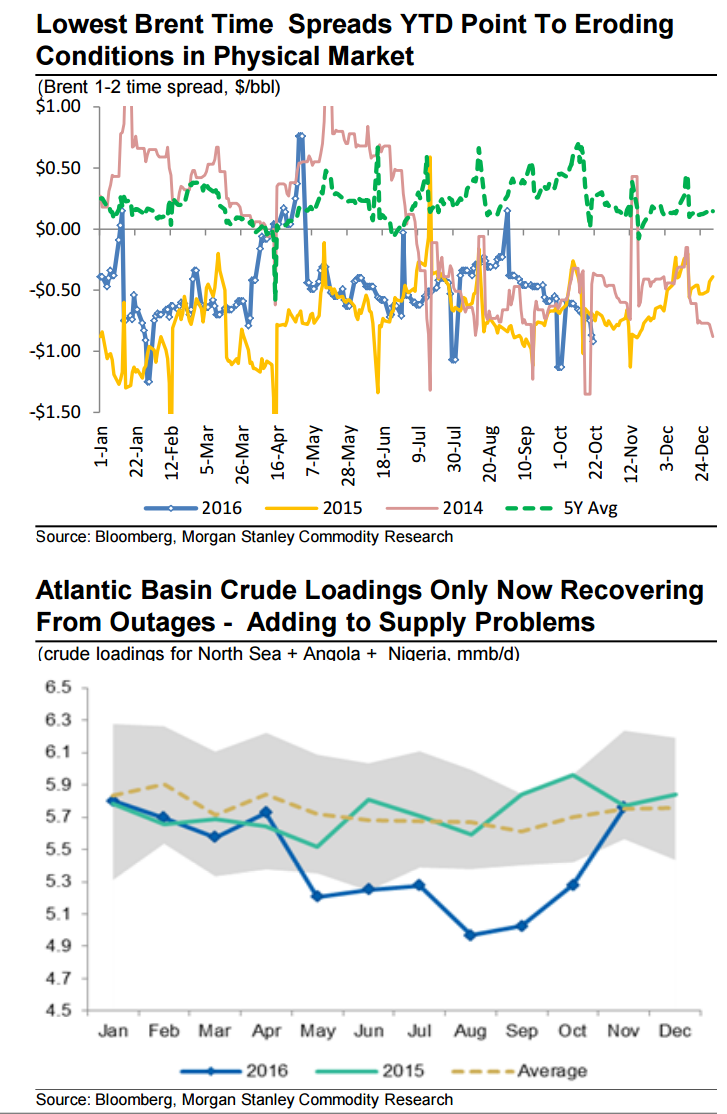

Physical Markets Showing Stress As Crude Loadings Recover. While the market has focused on better US inventory trends of late, the global market is quietly showing some signs of physical market stress. The Brent prompt time spread is now at its lowest level YTD (other than expiry days), and North Sea and WAF crude diffs are weakening. The primary challenge is not refinery maintenance. Atlantic Basin loadings, which have been quite low since May on supply disruptions and maintenance, are finally recovering. This is why many recent inventory data points citing bullish inventory draws are backward looking. However, the schedule shows a sharp increase into Nov, back to early 2016 levels. These exports are more important than production for inventories and physical markets. The return of Libya and rising freight rates likely compound the problem. Dubai time spreads offer a mixed picture.

Headline Rig Count May Understate Upcoming US Supply. Total rig count and time lags continue to distort the magnitude of the coming US response. The growth rate of more productive horizontal oil rigs has continued unabated, with volatility coming in vertical and directional rigs. We should see rig counts continue to increase in the wake of the recent price rally and hedging, but with a lag, based on recent trends in producer hedging, prices and the 12-24 time spread – all of which point to more US production in 9-12 months. Moreover, the recent rise in horizontal rigs and hedging at increasingly lower thresholds is indicative of lower breakevens and the US potential. And yet, well productivity has the potential to rise substantially from here. Thus, we are increasingly in the Exxon camp (see comments inside), as shale’s disruptive nature and potential remains underappreciated, in our view.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.