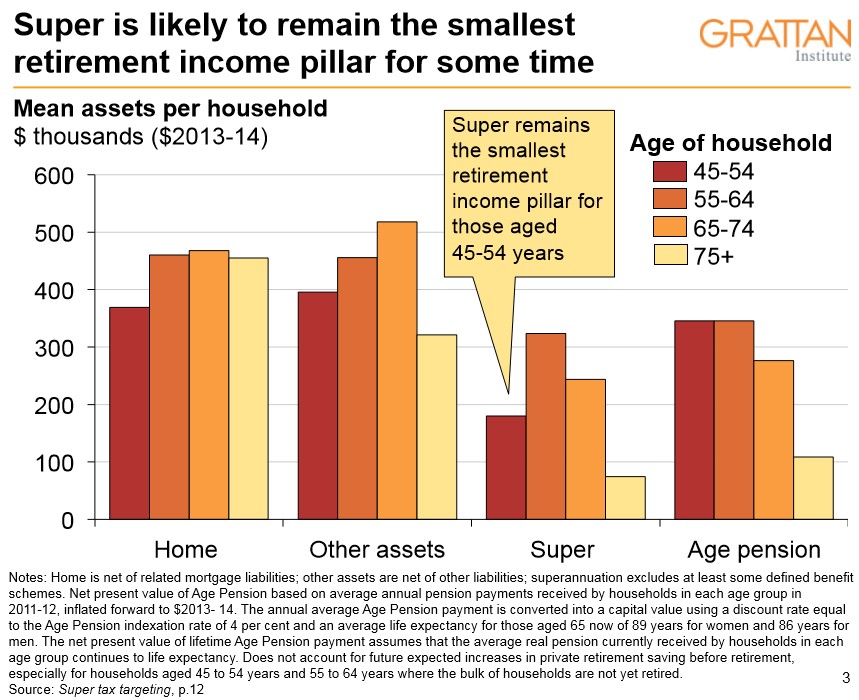

The Grattan Institute has released an interesting background paper showing that the importance attached to superannuation as a way of funding retirement is way overblown, with super likely to remain the smallest pillar of retirement income for the foreseeable future:

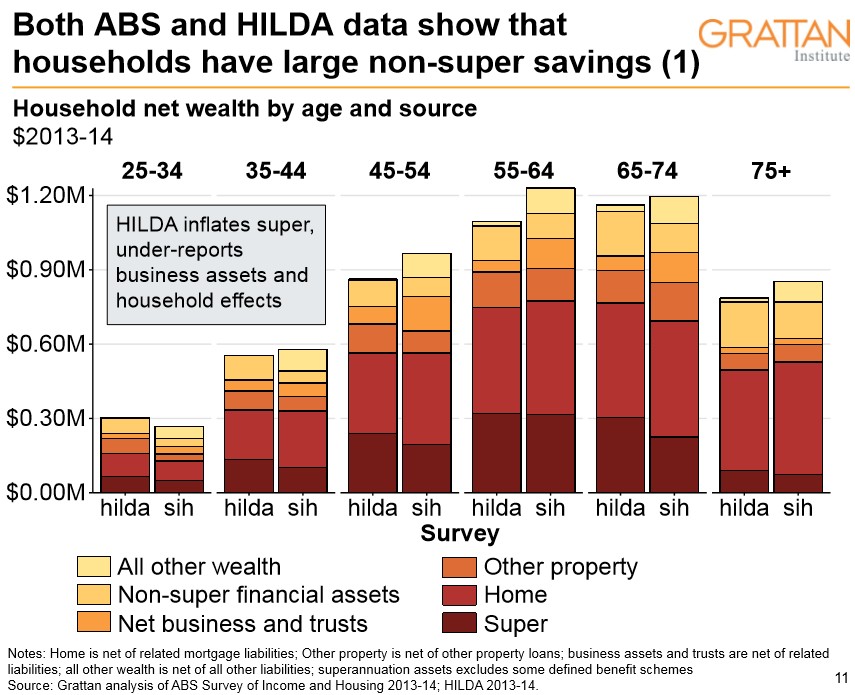

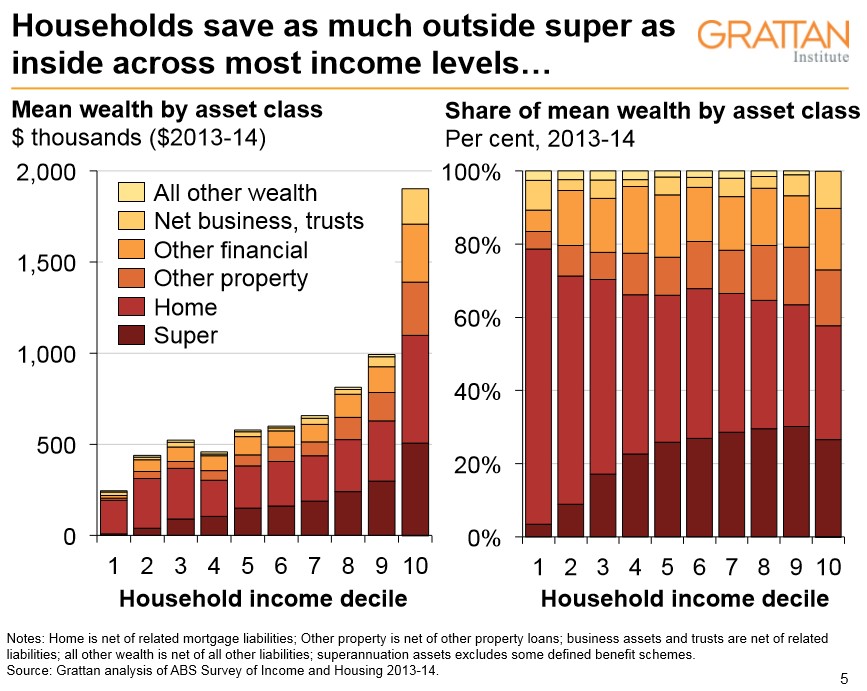

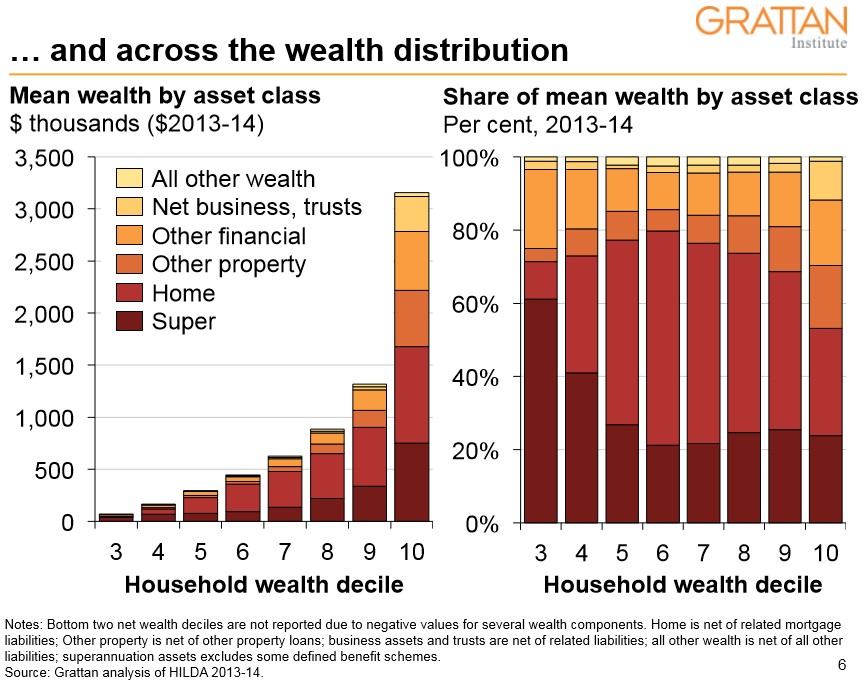

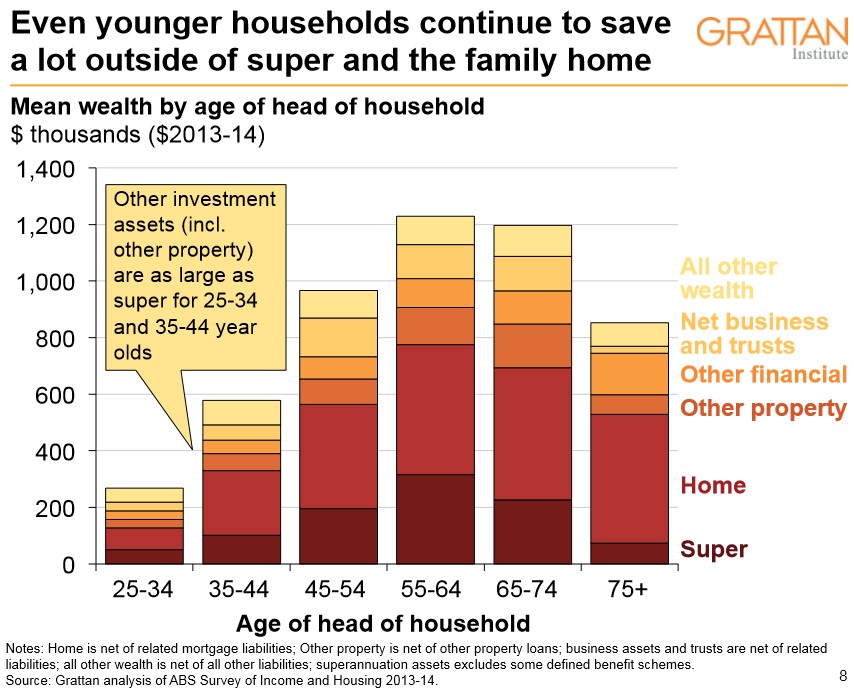

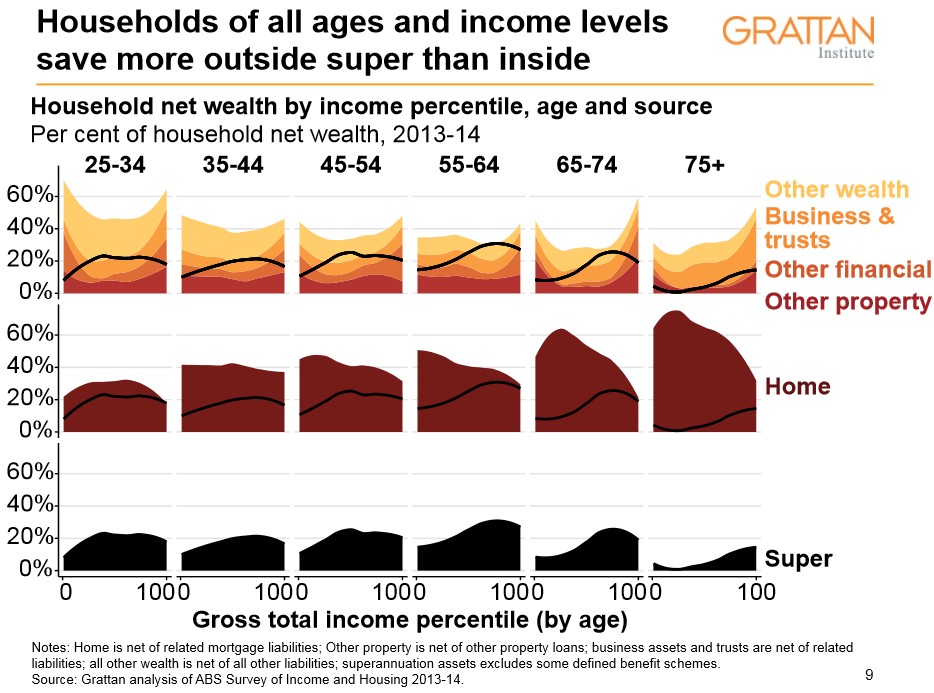

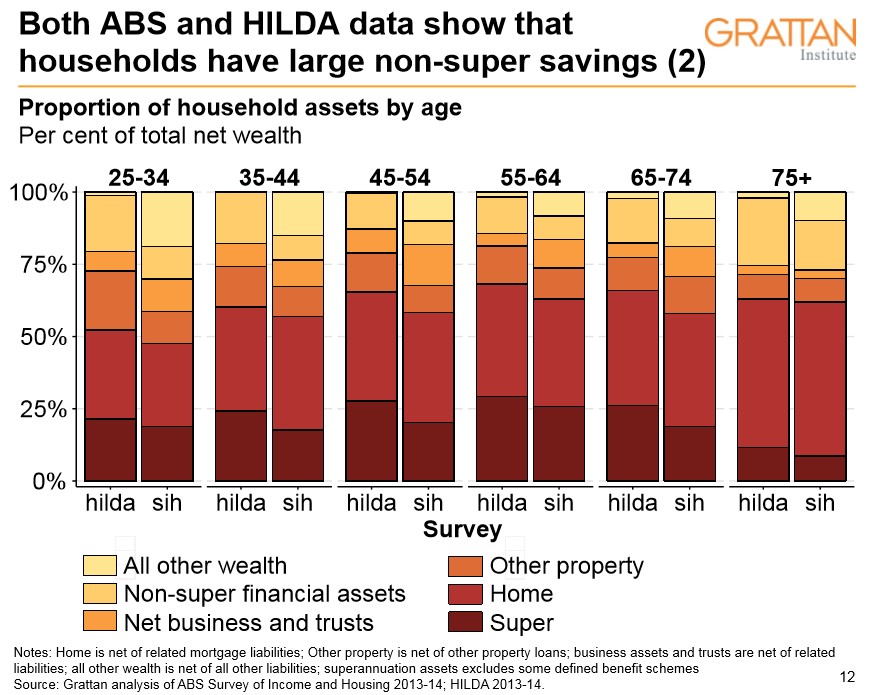

The reality is that superannuation savings account for only a small portion — about 15 per cent — of the wealth of most households, as confirmed by new analysis for Grattan Institute of both ABS data and the Melbourne Institute’s HILDA survey. Even without counting the family home, the average Australian saves as much outside as inside the super system. For older households close to retirement, assets other than super are often even larger than the value of their homes. Super’s modest contribution to retirement savings is true for households of most levels of wealth and income.

When confronted with facts about the modest contribution of super to retirement savings, many commentators point out that the system is immature. It will be another two decades before typical retirees will have contributed at least 9 per cent of their wages to super for their entire working lives. But while we might expect younger households to save more in super, and less outside, that’s simply not true. Their assets outside are typically as large as their assets inside superannuation, even without counting home ownership. This is so even for households in the 25-to-34 and 35-to-44 age groups who have had high levels of compulsory super for most of their working lives.

The enduring importance of non-super savings should come as no surprise. While compulsory superannuation forces people to save more via superannuation, there’s little evidence that non-super savings have fallen very much in response.

There is little reason to expect this pattern of non-super saving to change radically. Households hold a material portion of their wealth outside of super so that they have an option to use it before turning 60, and because they are nervous that government may change the superannuation rules before they retire. Other asset classes, such as negatively geared property, are taxed lightly, and so will likely remain an attractive vehicle for accumulating wealth. Whatever the motivation, most households heading towards retirement have substantial non-super non-home assets to draw on.

Grattan believes that super’s more modest contribution to retirement savings also has big implications for retirement incomes policy:

Advertisement

First, since most Australians will rely upon a range of assets and income sources to support their retirement, we shouldn’t expect superannuation alone to provide an ‘adequate’ or even a ‘comfortable’ retirement, as the super industry demands.

Second, ignoring non-super savings may lead policymakers to force people to save too much through superannuation, if the compulsory Superannuation Guarantee is lifted from 9.5 per cent to 12 per cent of wages, as currently legislated.

There are powerful vested interests pushing the idea that super equals retirement savings. Yet such a view is inconsistent with the facts. Super’s importance to retirement savings has been overblown for far too long. As the debate heats up over policy for Australia’s $2 trillion super sector, recognising what households actually save, and why, would be a big step in the right direction.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.