Says there is a baton passing from monetary policy to fiscal policy

Could be looking at trillions in bond issuance

2018 to 2020 … Look out, there’ll be a deficit explosion

Inflation is returning in commodities, wages

Future inflation gauge has been moving higher

two thirds of consumer price increases is from rent

And Marc Faber at CNBC:

Just because a road is lousy does not mean it will be fixed. Cripes, that’s why it is lousy.

So, I still disagree. China remains the marginal price setter in every commodity and the rally will last as long as it allows it and no longer. All major commodities remain in oversupply as well and present prices will already trigger a lot more supply, including oil. The US dollar is in a bull market too and the Fed still tightening. Goldman wrapped it all up nicely last week:

After a year in which Chinese restocking and supply-side reform have had a significant impact on bulk commodity prices, many investors are asking whether the green shoots of western world demand pick-up, coupled with the potential for fiscal stimulus (rather than monetary easing) will drive the next leg of the metal cycles. The potential for a traditional industrial cycle-led demand recovery was highlighted in a report by our Australia and New Zealand economist team ‘Morphing from a debt deflation cycle to a traditional industrial cycle’, September 1, 2016. A recovery driven by non-China industrial sectors would be likely to focus on demand for the traditionally ‘later cycle’ commodities — aluminium, copper, nickel and zinc. So, after the strong bulks rally but overall inertia in base metal prices in 2016, focus is on whether Western World fiscal stimulus will drive a rally in base metal prices.

We think a rally in base metal prices is unlikely given:

Non-China demand for base metals has fallen sharply in the past decade.

Base metals are well supplied with inventory levels high across the board.

Any slowing in Chinese demand would likely offset any Western World pick up.

Metals (and energy) have much deeper and more mature financial markets and thus are less prone to speculation led rallies, which we believe are partly responsible for the increase in the prices for bulks, along with supply-side drivers such as regulation. Therefore, we believe the recovery in economic growth in the Western World will not have enough potential to drive metal prices higher. Based on our Commodity team’s forecasts, there is less downside to base metals and gold at current levels and consequently some global base metal equities — such as S32, Aurubis and Cameco — will likely outperform their more bulk exposed peers.

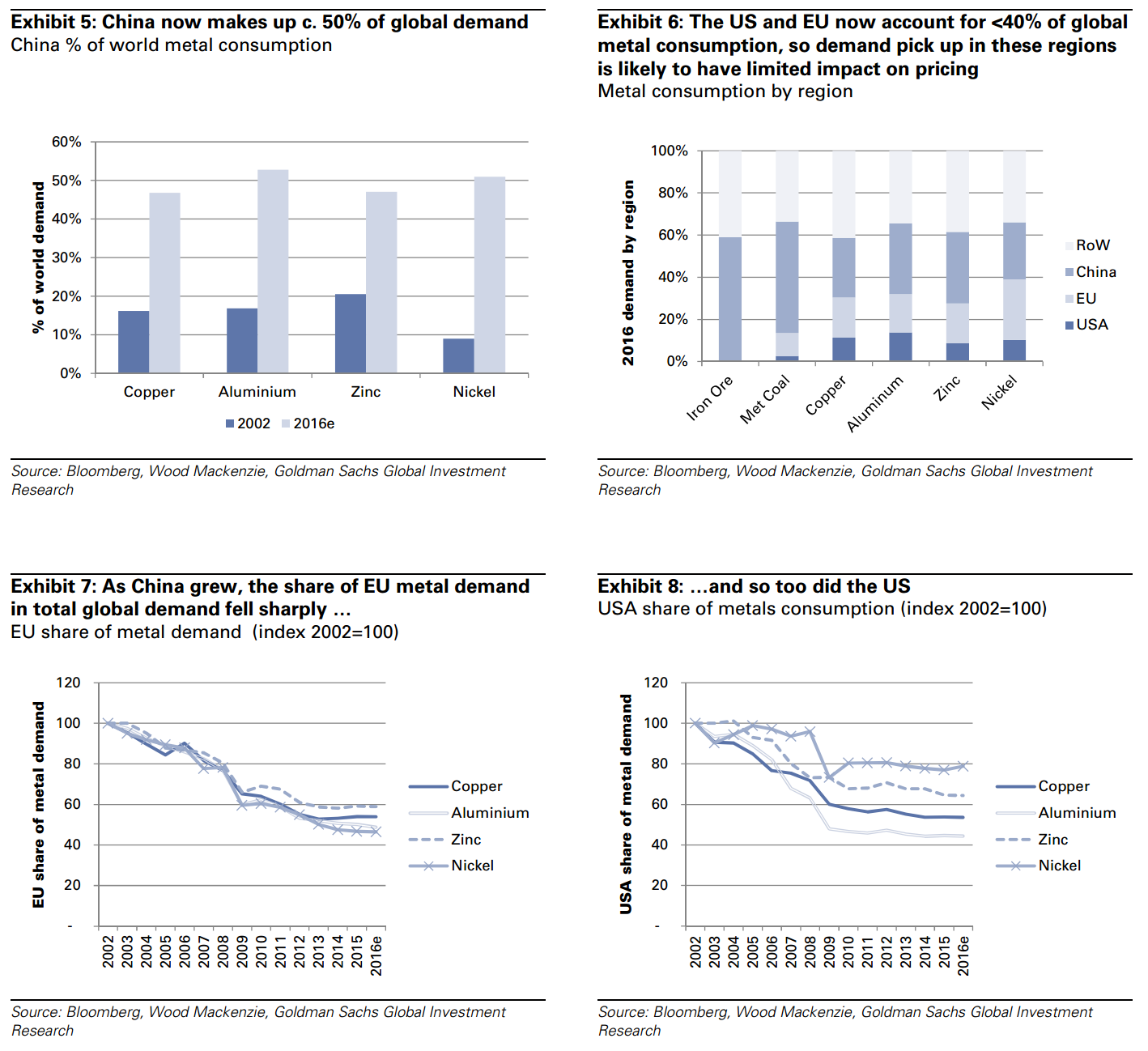

The decline in relevance for non-China metal consumption

China has accounted for over 100% of demand growth for most metals since 2002 and is now the major consumer of metals. Even when combined, the EU and US consume less metal than China. Consequently, although developed market growth is undoubtedly a positive for metals prices, its effect on physical demand is limited.

The emergence of China has significantly reduced the importance and impact of US & EU (or more broadly OECD) metal demand. Therefore, we think the impact of any demand recovery in these regions will have a more muted impact on metal prices than in previous similar cycles. Western world demand indicators Before the emergence of China as the main driver of metal demand (ie, before 2002), US housing starts, Lead Economic Indicators and M2 were the key macro indicators used to assess the directional movement in base metal prices such as copper and aluminium.

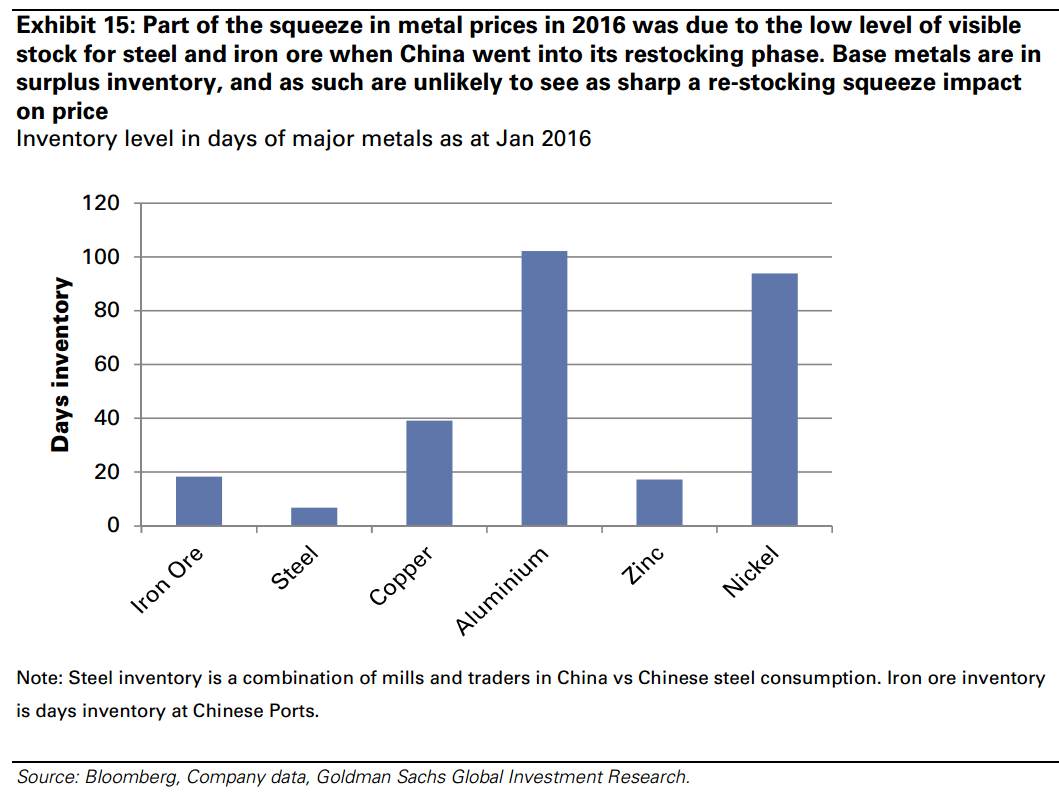

Inventory levels remain high

We believe the significant uplift in bulk metal prices in 2016 was supported by low levels of inventory, especially steel and coal, in China. Essentially, we attribute price moves to aggressive re-stocking in 2H15 and 1H16. Inventory levels of steel were at ex-GFC lows in 2H15 — and thus a rise in steel prices forced a significant re-stocking of both steel and iron ore, having an impact on price.

Whilst steel and iron ore inventory levels were low at the start of this year, the same can not be said for the base metals – with the possible exception of zinc. We would contend that the adequate level of stock (coupled with deeper futures and financial markets for the base metals) would preclude any significant upward pressure on prices stimulated by a moderate rise in Western World demand.

Could a pickup in demand shift metals from surplus to deficit?

Since 2002, non-China metals demand growth has effectively been zero. The year of maximum demand for base metals was 10% in the year coming out of the GFC (i.e. 2010). Given the 10% was off a recessionary environment we wouldn’t expect that type of growth YoY in 2017, even if fixed asset investment in both the EU and the US were ramped-up. Even a 5% elevation would represent a strong pick-up, in our view, and would be significantly above our forecasts of a c.1% uplift.

If there were a 5% uplift in US & EU, we calculate demand it would drive incremental demand as follows;

Copper – 245kt

Aluminium – 645kt

Zinc – 307kt

Nickel – 49kt

However, given current inventory levels, both copper and aluminium would remain in surplus for 2017. We already expect Zinc and nickel to be in deficit so any incremental demand would compound this.

The charts below look at what demand levels for metals would be needed to balance the markets in 2017.

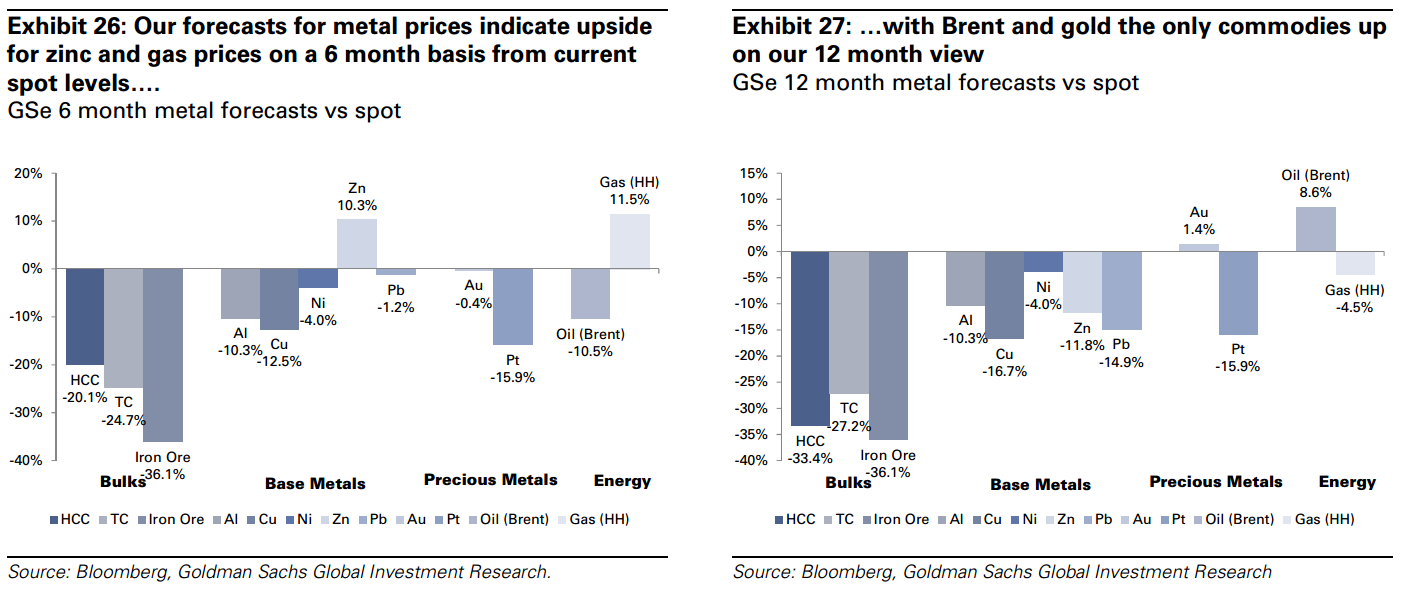

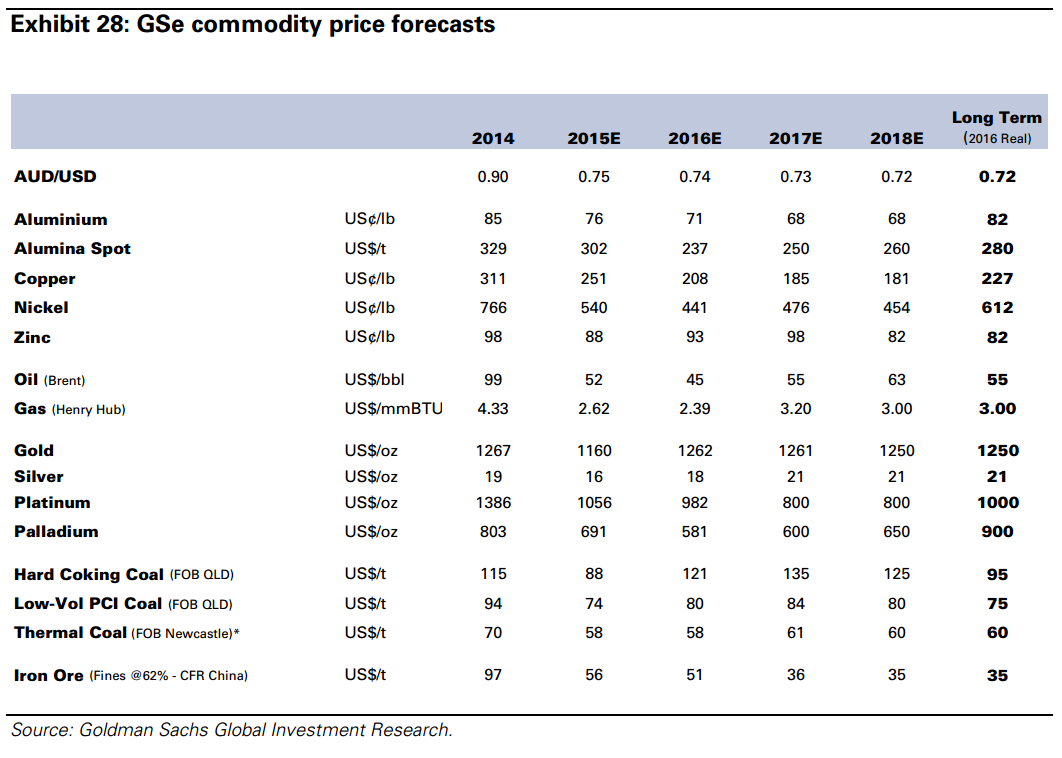

Commodity forecasts – We prefer zinc and nickel Given the deficit we expect in both nickel and zinc markets, relative to the surplus we see in aluminium and copper, we prefer the former base metals from a price perspective into 2017. The charts below look at the forecast move from spot to meet our price forecasts over 6 and 12 month timeframes.

Advertisement

For me, then, commodities are still in the process of shaking out to the lowest marginal cost of production.

I can foresee a time to buy commodities on a global infrastructure push but it is not until it is supported by monetary policy in the form of helicopter money to give it real scale. That comes after the next shock not before.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.