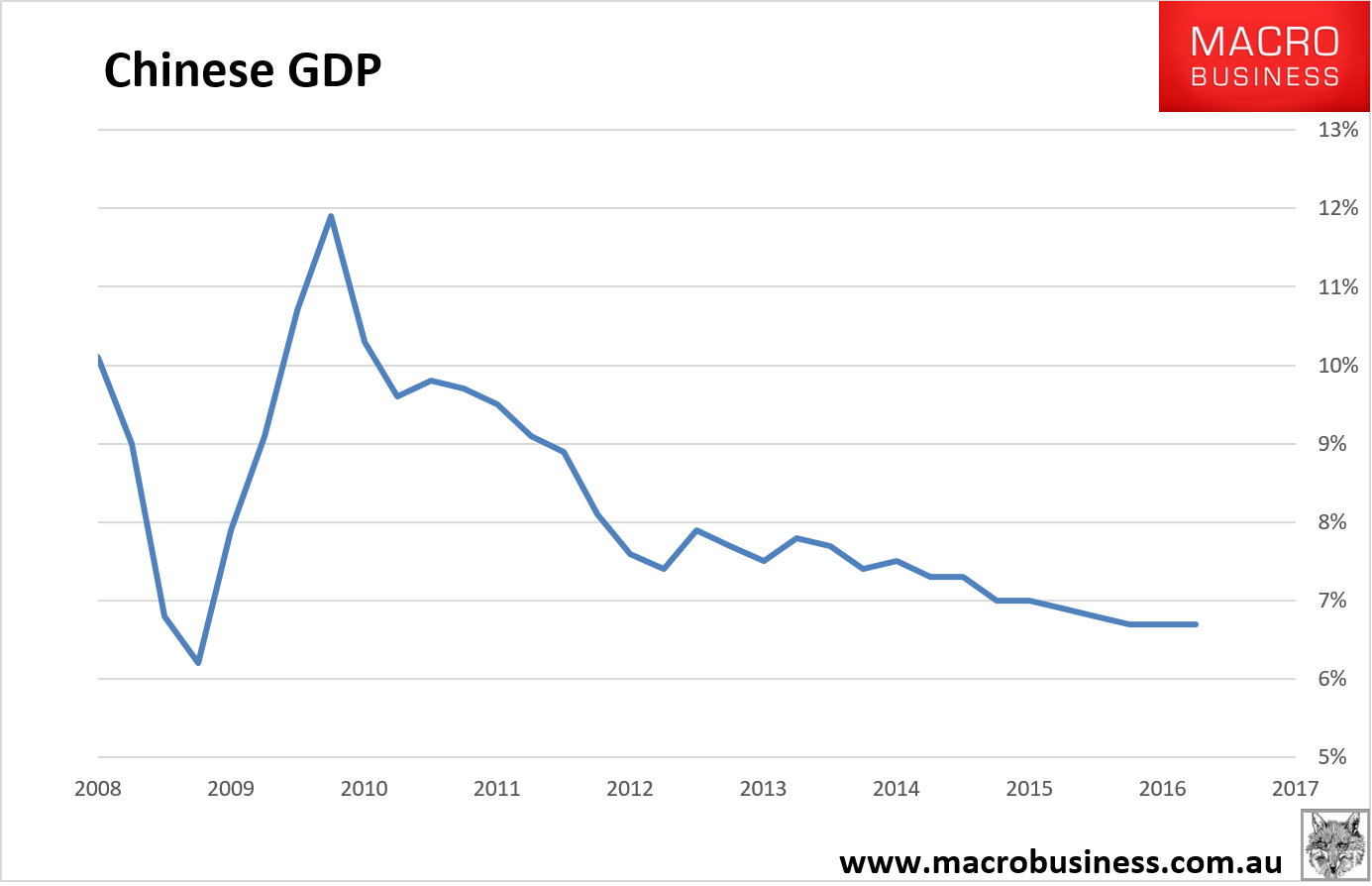

China’s September data dump is upon us. GDP hit 6.7% as expected (shock!) and quarterly growth came in at a pretty warn 1.8% or 7.2% annualised:

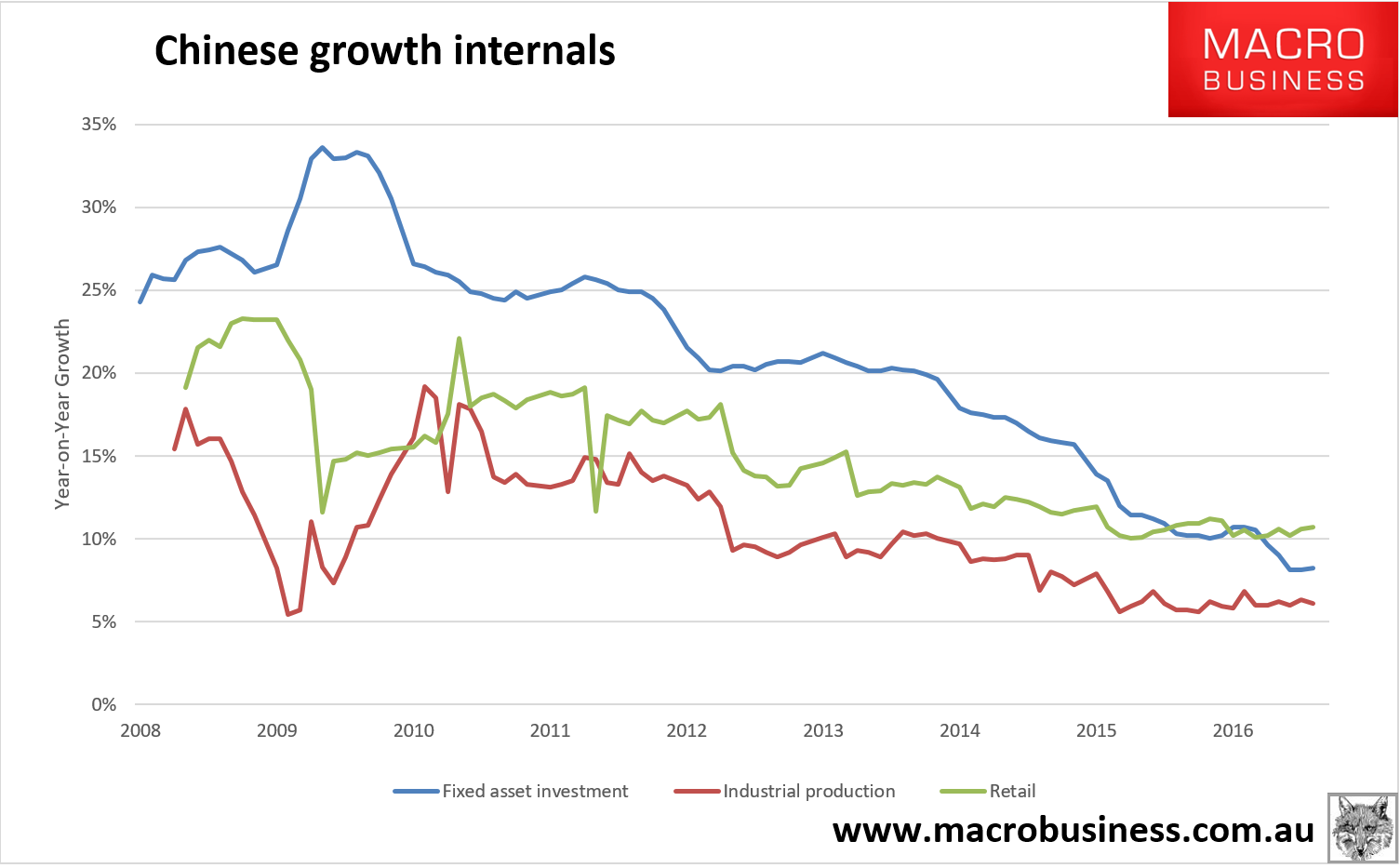

Digging into the monthly data we find everything around consensus with industrial production at 6.1%, fixed asset investment 8.2% and retail sales 10.7%:

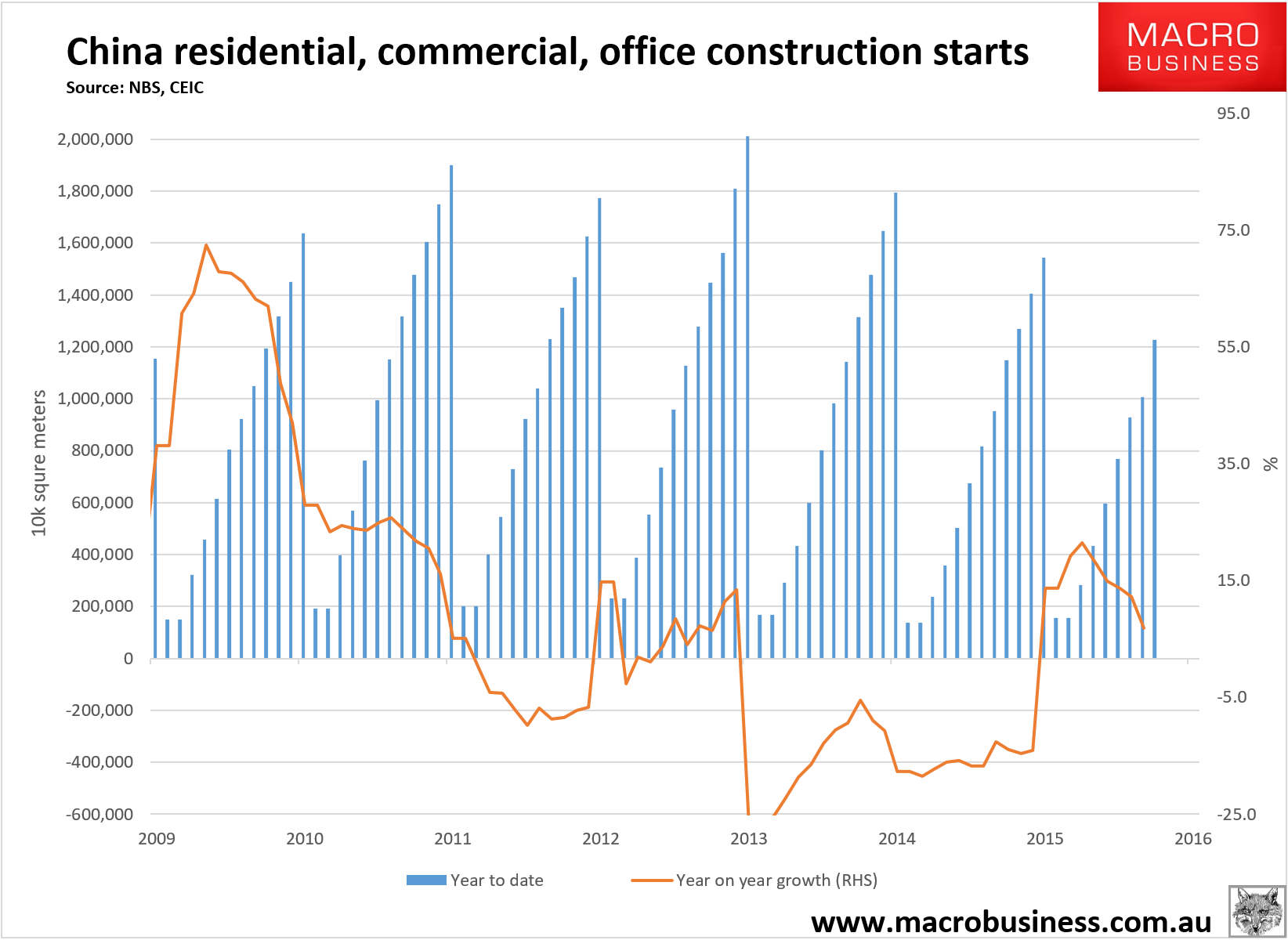

Turning to more commodity-centric data, the property market continues to decelerate very much as expected. Starts are now up 6.2% versus 12% last month:

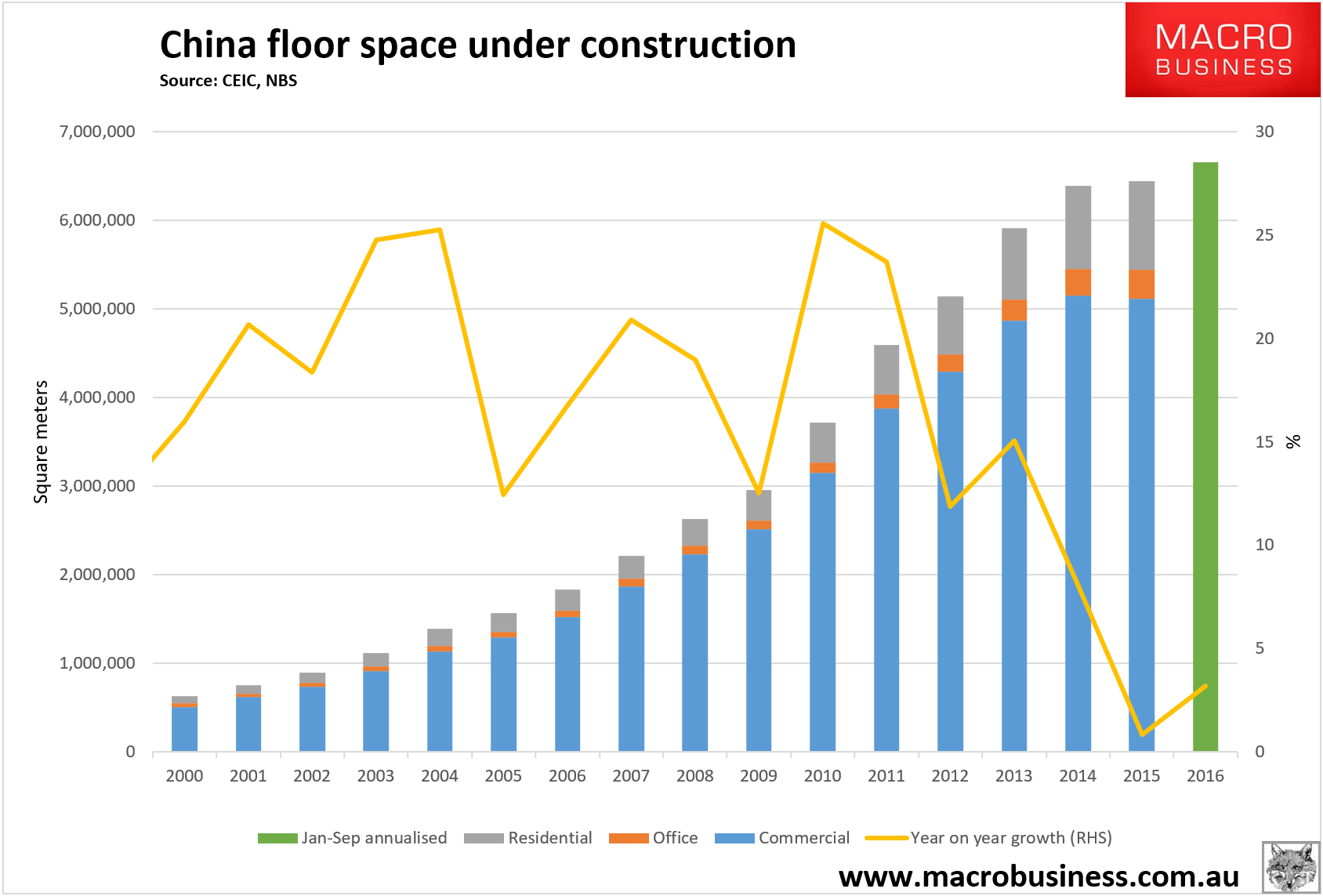

And year to date total floor area under construction receded to 3.2% from 4.6% growth annualised. I still expect it to end the year flat:

Sales of realty floor space were pretty barmy at 43% growth year to date but some of that is the base effect from a weak 2015 and a lot of it was the pre-tightening charge that hit the market when it sniffed the prudential handbrake was being pulled. I am skeptical that it will lead a surge in new construction.

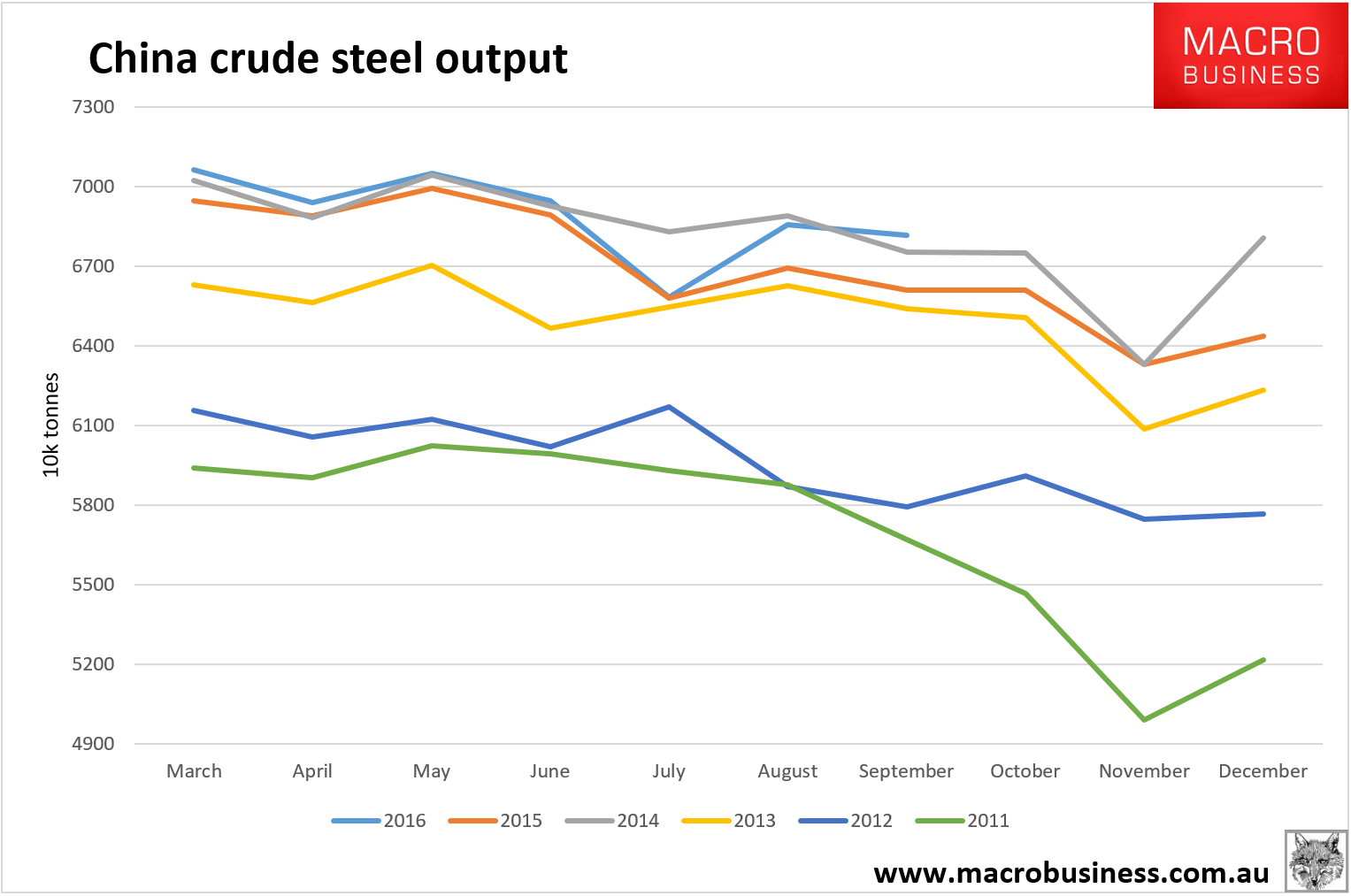

In terms of actual output, steel production hit another record at 68.17mt, now up year to date by 0.4% and quite likely to end the year with growth:

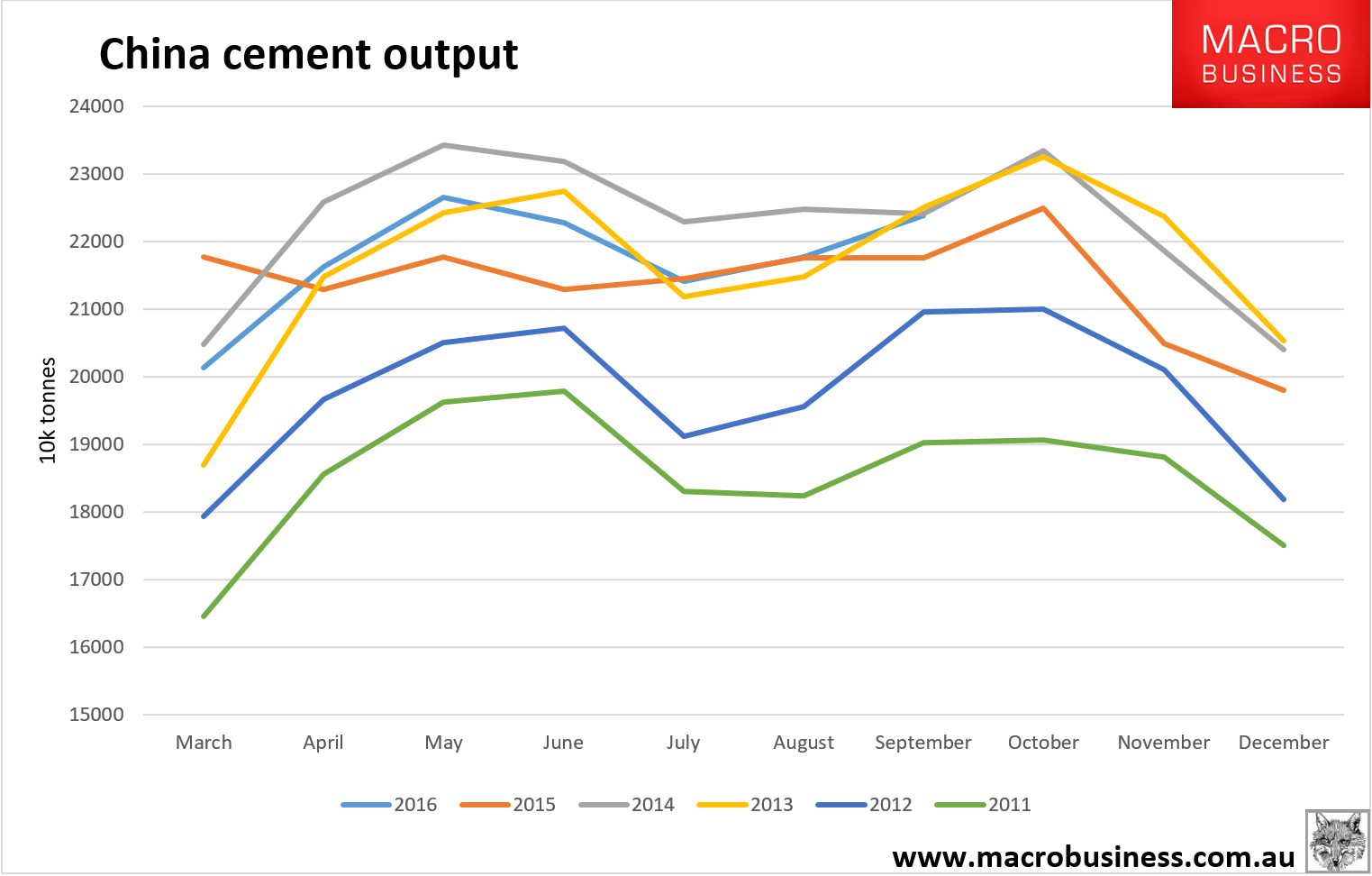

And cement production climbed into the construction season at 22.4mt, up 2.6% year to date:

In short, China is chugging along perfectly happily right now on its real estate boomlet but the signs are still there in the second derivative of growth that construction will be a problem for commodities by year end.