by Chris Becker

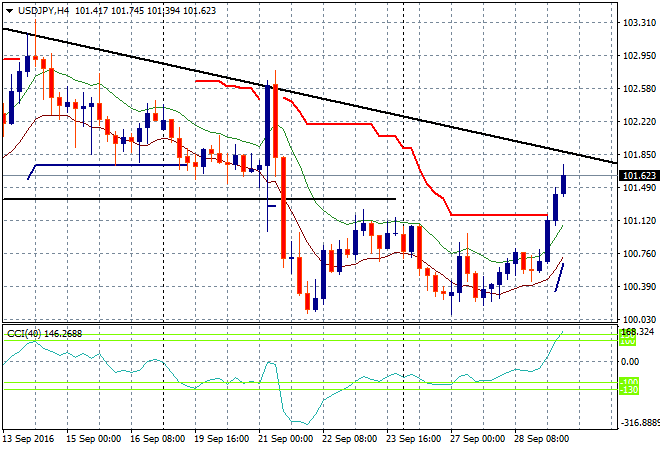

Oil is oils….the OPEC non-deal is pushing risk up to new heights of silliness with stocks across Asia boosted by the rise in oil prices as the USD firmed especially against Yen. The USDJPY pair has rocketed through the 101 handle and is about to breach its long held downtrend from its start of year decline:

As a result of Yen weakness, the Japanese Nikkei took lifted 1.4% to 16700 points to its highest mark for the week. Chinese stocks reversed their previous losses with the Shanghai Composite rallying above terminal support at 3000 points, now up 0.5% to 3002 going into the close. Can it hold here as the risk train gathers momentum?

As for the ASX200, even as the fallout from the SA blackout, well falls out (including the nonsense about renewables from the experts like Alan Jones), energy stocks are soaring with Santos, Origin and Woodside all up around 7% or more. Coupled with a return to favour in bank stocks, the local bourse closed up 1% to 5471 points, almost at my target of 5500 points.

Eurostoxx and S&P500 futures are up over 1% going into the London session with the OPEC deal ringing the bell for risk traders on both sides of the Atlantic.

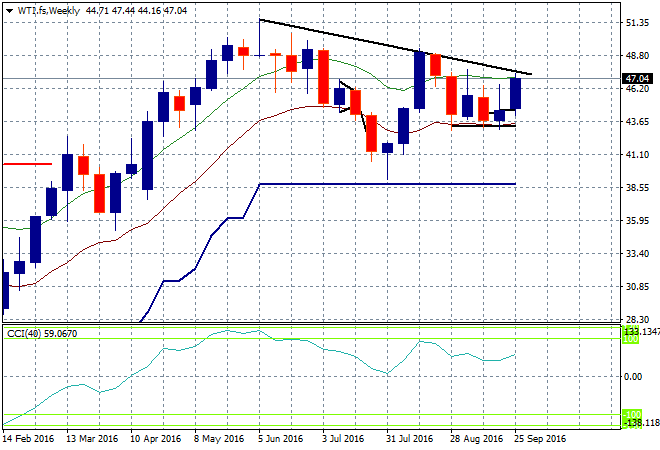

The longer term chart of WTI bears (sic) looking at however:

The weekly chart shows that while momentum is behind it, WTI faces resistance very close overhead at the $50USD per barrel level. But as you all know, oil can go up 50% for no reason at all, and the first oil production cut in 8 years may be catalyst enough to send the bulls racing.

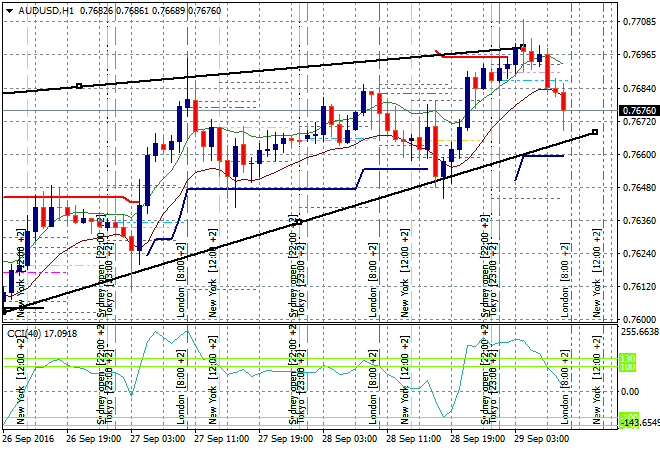

In currencies, the Aussie dollar is losing its to shine, after getting up to 77 cents against the USD it has slowly melted in the Asian session as a potential bearish rising wedge pattern is building on the hourly chart. I’m watching the bottom trendline here for a break tonight:

The data calendar tonight focuses on the only unemployment print the ECB cares about – Germany (because who gives a damn if half of Southern European young people can’t find a job!) and the September preliminary CPI print, which again the ECB only cares about, as it clings to a Weimar view of economics! In the ‘States theres a few 2Q GDP internals being released and a few speeches from Fed members to watch out for.