LF Economics lodged a submission to the House of Representatives Budget Savings (Omnibus) Bill 2016, entitled Australia’s Low Public Debt… With Poor Infrastructure to Prove it, which examines the state of government finances in Australia and calls for significant public investment in economic and social infrastructure.

The report notes that Australian public debt is low by historical standards, therefore, the real focus of policy makers should be on Australia’s world record private debt:

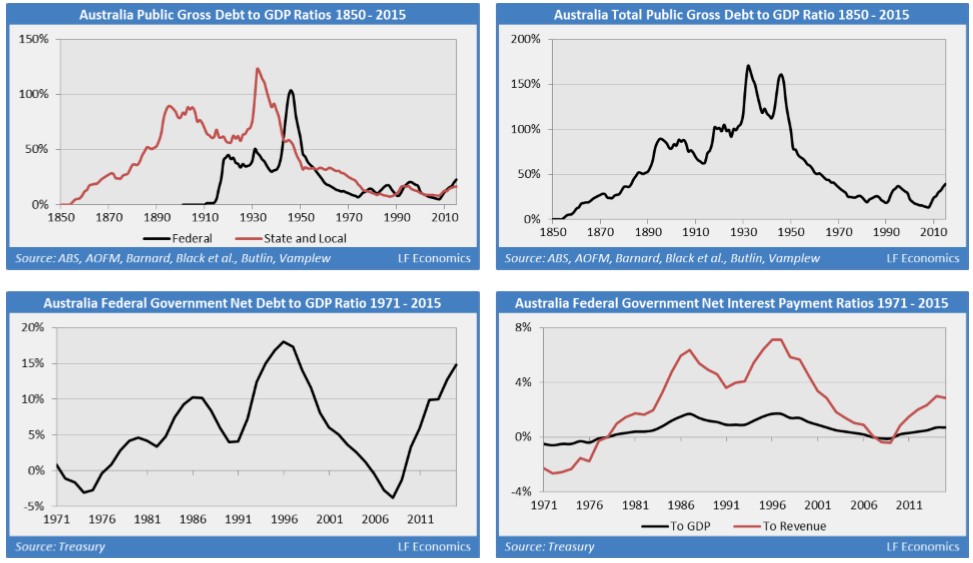

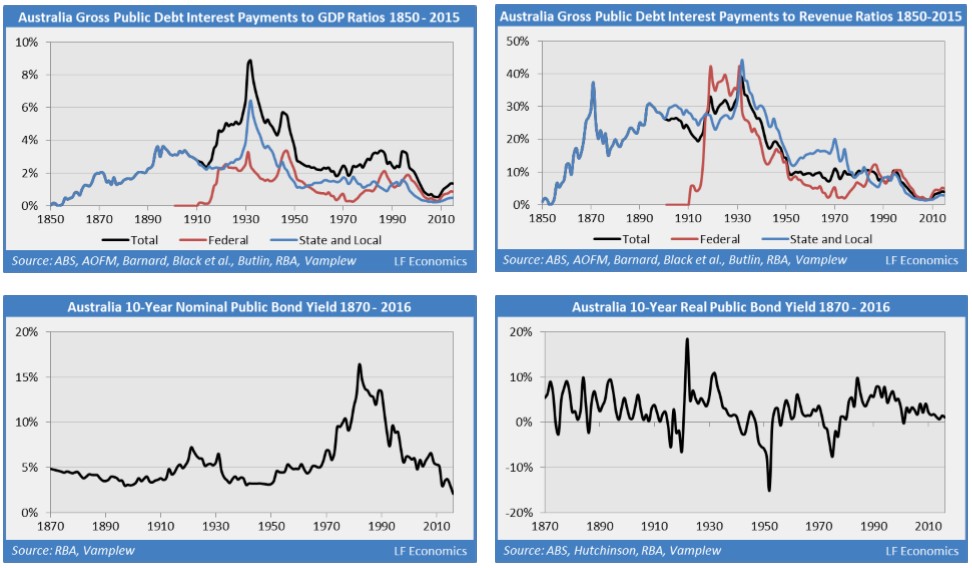

Despite the concerns (primarily from the LNP) about the rising stock of public debt, viewed over the long-term, it is low relative to GDP. The decline in interest rates has also resulted in low debt interest expenses to both GDP and revenue. This long-term data is rarely shown or referenced as it demonstrates the often hysterical commentary about the ‘budget emergency’, ‘peak debt’, ‘bankruptcy’, ‘running out of money’, ‘record deficit’ and so on is blatantly false.

With an estimated deficit of 2.3% and 2.0% for 2015-16 and 2016-17 respectively and a historically low 10-year government bond yield, the deficit could be slightly increased to 3%, targeted to nominal GDP. This counters the slowing of the economy, demonstrated by rising underemployment and weak youth unemployment, falling capital expenditure, record low wage growth, compounded by the closure of the auto industry, a lacklustre innovation system starved of private capital, paltry R&D investment and pitiful transportation infrastructure.

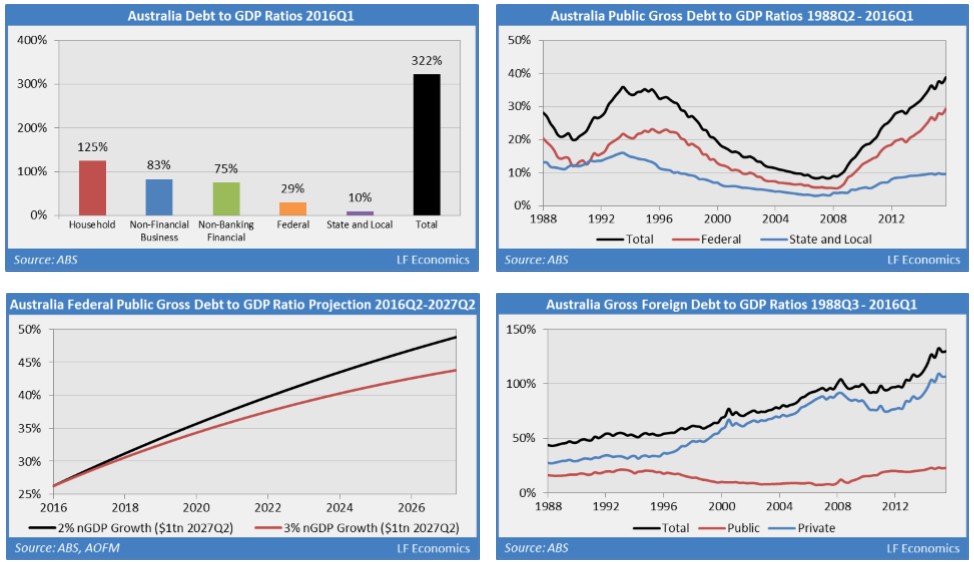

The real budget emergency lies in the household sector, with debts of 125% of GDP and rising. Government refuses to deal with this as the FIRE (finance, insurance and real estate) sector is generating immense profits and provides campaign contributions (bribes) to the government…

As long-term data shows both the stock of public debt and net interest payments to be at historical lows, concern appears to be largely fabricated. It may be the government and FIRE sector has done this to:

- Distract from the threat of the massive private sector debt boom, financialisation and the housing bubble. The diversion is understandable, for the FIRE sector has fuelled an immensely profitable land market bubble enriching its participants;

- Create a non-existent ‘economic Armageddon’ scenario facing the economy, thereby preparing a case for further privatisation of essential public assets and services as a ‘solution’ to reduce public debt. The end result is typically economic inefficiency: private monopolies, duopolies and oligopolies;

- Prevent government from funding infrastructure efficiently, given public borrowing costs and fees are significantly lower than that of the private sector;

- Provide a pretext for austerity which disproportionately disadvantages low and moderate income earners; and

- Ensure government has room to ramp up public debt to fund a future bailout of Australia’s highly leveraged banking system once the housing bubble bursts and lenders become insolvent. Australia’s low public debt is similar to Ireland’s prior to the GFC.

It is critical policymakers reign in exponentially-growing private sector debts as this consists of a major source of future financial instability. Australia’s household debt to GDP ratio is the highest in the world, at 125% and rising. Ironically, by ignoring private debt expansion which has generated a housing bubble, public debt will inevitably rise to stimulate the economy to counteract the economic downturn when it bursts. This is what we should be paying attention to…

LF Economics also calls for the abandonment of the Omnibus savings bill in favour of expanded spending on infrastructure and innovation:

The government relies upon unachievable expectations of the private sector by assuming the Australian economy will continue to grow while government seeks to reduce its expenditures. Put simply, the government is not interested in investing for the future and expects the private sector to do the heavy lifting even as capital expenditure plummets and wage growth falls to record lows. Federal public debt, including that at the state and local levels, are low by global standards and Australia has some of the poorest infrastructure in the OECD to prove it.

Congested roads, slow rail transportation systems, monopolistic airport networks and Internet services are a national disgrace. Poor transportation infrastructure is generally more taxing to society and government revenue than the cost of investing and renewing such infrastructure. Reducing travel times by road and rail in our cities by half should take priority over balancing the budget. Opening new transport and communication corridors to rural and remote regions will assist in the revival of some of Australia’s once popular towns now combating challenging economic conditions. The private sector has neither the capacity nor credit rating to rejuvenate Australia’s ailing and second-class infrastructure.

Government cannot expect the so-called ‘Ideas Boom’ to successfully develop without significant upfront public investment over the next decade, building the nation’s pipeline of R&D projects and innovations. Contrary to popular belief, most of the high-calibre technological innovations in the U.S. were initially developed within the public sector i.e. government laboratories and the university sector. U.S. government agencies such as DARPA, NASA, alongside the EPA, have been at the forefront of their innovation system whereby the public sector creates the technology then passes it onto the private sector to commercialise and mass-market the products and services.

The benefits of the government setting up and funding a similar group of public institutions – like the CSIRO – would significantly supersede any possible detriment arising from a constant but small public deficit. This would also assist in the recovery of Australia’s dying manufacturing sector, renewables industry and export-exposed sector, harmed by the persistently high real effective exchange rate. If the government is serious about investing in Australia’s future, it needs to abandon its aversion to historically and internationally small public debt and deficits.

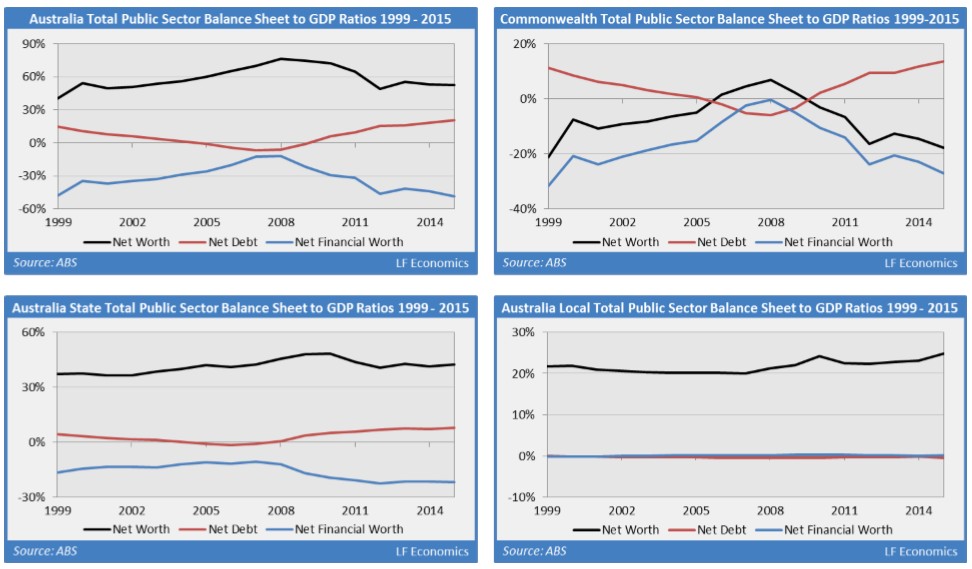

To support its arguments, LF Economics has included a comprehensive chart pack illustrating Australia’s low public debt:

Great report. You can view the whole thing here (Submission #145).