At the conclusion of the Algeria meeting, Reuters is reporting OPEC has agreed to limit production

The agreement would be finalized at the next OPEC meeting on November 30, 2016

OPEC is supposedly limiting its output to 32.5 mmbpd, which is effectively where OPEC was in January 2016.

But in August, output reached 33.47 mmbpd, which implies a 1 mmbpd cut.

The delta from August output levels is contributing to the market jolt

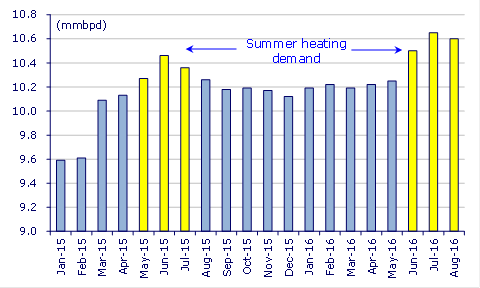

But remember, Saudi Arabia oil output spikes in the summer due to cooling demand

What is unclear is Iran and Libya

Iran is at 3.6 mmbpd with a target of 4.2 mmbpd…and a staunch resistance to freezing until reaching 4.2 mmbpd

Libya is at 0.3 mmbpd with a target to recover to 1.0 mmbpd by year-end (aggressive)

Saudi Arabia oil output

All-in, if the 32.5 mmbpd number is accurate, then OPEC is rolling back to January levels, which is effectively what it had previously suggested it might due. The market response is not surprising, but probably not sustainable either. The devil is in the details and we still do not know how Iran and Libya fit into the equation, or if this is just another proposal that will be dismissed by Iran.

Shale oil economics are an increasingly convincing and credible source of supply growth. Initial production rates have jumped 50 – 100% just in the span of a few years. Spud-to-pipe times have also dropped to 135 days for a pad of three wells, down 13% from 2015. Oil prices sustained in the low $50s is the level that seduces more capital in shale…thus Saudi better be careful what it wishes for. We already expect supplies to flatten out in the US in early 2017 with limited increases in rig activity. A rebirth of activity could prompt a rapid rise in US oil output within 6-months, offsetting OPEC’s efforts once again.

Note – possibly negating the some of the potential impact of this news. Russia, the world’s largest energy exporter, is reportedly on course to pump a post-Soviet record amount of oil in September, adding as much as 400,000 barrels a day to the country’s production.

Who is going to cut? Iran? No. Iraq? No. Libya? No. Nigeria? No. The tiddlers? No. Maybe Kuwait but without the others?

Saudi is nodding at itself in the mirror. It cuts unilaterally or there is no cut.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.