Let’s round up the Deutsche Bank analysis, from the AFR:

The European Central Bank’s negative interest rate policy has eroded the profitability of its retail banking operations in Germany, where margins were already thin.

But the German bank’s woes were exacerbated when the US Department of Justice made a much larger than expected $US14 billion claim to settle allegations relating to Deutsche’s involvement in the US subprime market in the lead-up to the financial crisis.

The German bank has insisted that it will not pay anywhere near that figure, which is close to its entire market capitalisation.

But the US Department of Justice demand has put Deutsche boss John Cryan in an invidious position. He is reluctant to raise extra capital at a time when Deutsche’s share price is so low.

But the claim has made investors nervous, particularly as Deutsche’s plans to sell its roughly 20 per cent stake in China’s Huaxia bank have been delayed as Chinese regulators conduct a review.

Shares in Deutsche Bank have touched their lowest level in 24 years this morning, as Germany’s largest lender slumps to the bottom of Europe’s banking index.

Deutsche shares slumped by as much as 6.5 per cent to €10.69 in early morning trading – their lowest level on data going back to 1992, according to Bloomberg.

The sell-off has spread to broader European banks this morning, with all lenders on the Euro Stoxx bank index in the red this morning. The index is down 2.3 per cent to its lowest level in five weeks.

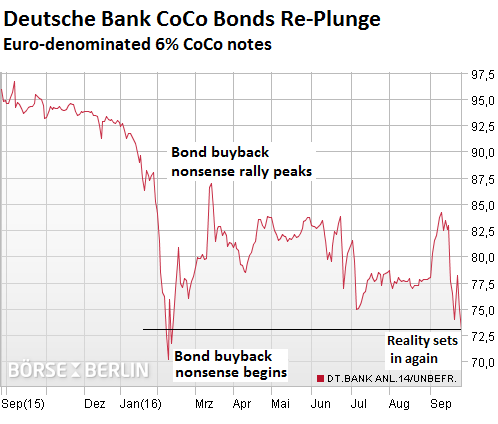

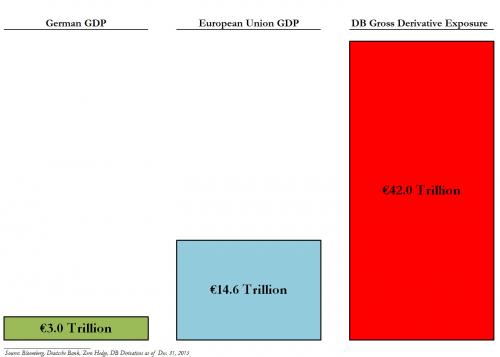

Its balance sheet, bloated with opaque risks, equals 58% of Germany’s GDP. It lost €6.8 billion last year. To hang on another day and to prop up Tier 1 capital, it has raised $20 billion in capital, in 2010 and 2014, by selling shares and diluted existing shareholders, and by issuing contingent convertible bonds.

These infamous “CoCos” are designed to be “bailed in” before taxpayers get to foot the bill. Thus, they’re a measure of investor fears about getting bailed in.

So when heck and high water came earlier this year, the bank responded by announcing on February 12 that it would buy back $5.4 billion of its ownbonds! Everything soared! Even CoCos, though not included in the buyback, rose 24% over a few weeks. We have long ridiculed this manipulative move [here’s detailed explanation… Deutsche Bank’s CoCo Bonds Speak of Fear of the Worst].

Now shares hit new lows, and the miserable CoCos are getting clobbered, dropping 2.7% today to 73 cents on the euro, down 28% from April 2015 when they still traded at 102 cents on the euro. They’re now just a smidgen from also setting new lows.

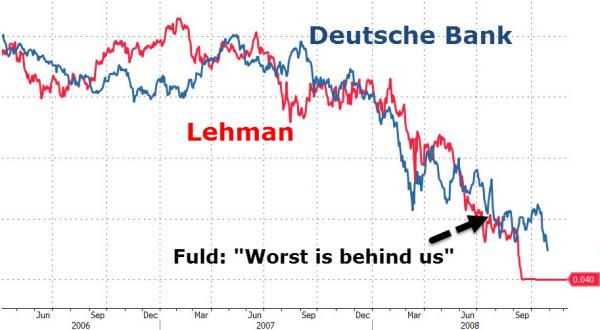

…it has become increasingly hard to ignore the slow-motion car crash that is Deutsche Bank, or to avoid the conclusion that something very nasty is developing at what was once seen as Europe’s strongest financial institution. Its shares have been in free-fall for a year, touching a new low of 10.7 euros on Monday, down from 27 euros a year ago. Over the weekend, the German Chancellor Angela Merkel waded into the mess, briefing that there could be no government bail-out of the bank.

But hold on. Surely that is an extra-ordinary decision? If the German government does not stand behind the bank, then inevitably all its counter-parties – the other banks and institutions it deals with – are going to start feeling very nervous about trading with it. As we know from 2008, once confidence starts to evaporate, a bank is in big, big trouble. In fact, if Deutsche does go down, it is looking increasingly likely that it will take Merkel with it – and quite possibly the euro as well.

…the German government looks to have abandoned it to its grisly fate. An article in Focus magazine quoted senior officials as saying the German Chancellor Angela Merkel was adamant that bank would not be rescued. There could be no state assistance if the bank was unable to raise the capital it needs to stay afloat, and she was not planning to intervene to get the American fine reduced. If it was in trouble, it was on its own.

…True, Merkel’s position is understandable. The politics of a Deutsche rescue are terrible. Germany, with is Chancellor taking the lead, has set itself up as the guardian of financial responsibility within the euro-zone. Two years ago, it casually let the Greek bank system go to the wall, allowing the cash machines to be closed down as a way of whipping the rebellious Syriza government back into line. This year,there has been an unfolding Italian crisis, as bad debts mount, and yet Germany has insisted on enforcing euro-zone rules that say depositors – that is, ordinary people – have to shoulder some of the losses when a bank is in trouble.

For Germany to then turn around and say, actually we are bailing out our own bank, while letting everyone else’s fail, looks, to put it mildly, just a little inconsistent. Heck, a few people might even start to wonder if there was one rule for Germany, and another one for the rest. In truth, it would become impossible to maintain a hard-line in Italy, and probably in Greece as well.

And yet, if Deutsche Bank went down, and the German Government didn’t step in with a rescue, that would be a huge blow to Europe’s largest economy – and the global financial system. No one really knows where the losses would end up, or what the knock-on impact would be. It would almost certainly land a fatal blow to the Italian banking system, and the French and Spanish banks would be next. Even worse, the euro-zone economy, with France and Italy already back at zero growth, and still struggling with the impact of Brexit, is hardly in any shape to withstand a shock of that magnitude.

It short, it cannot be let go though we’ll probably have to sail to the edge of the abyss first.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.