From Macquarie’s latest Chinese steel mill sentiment survey:

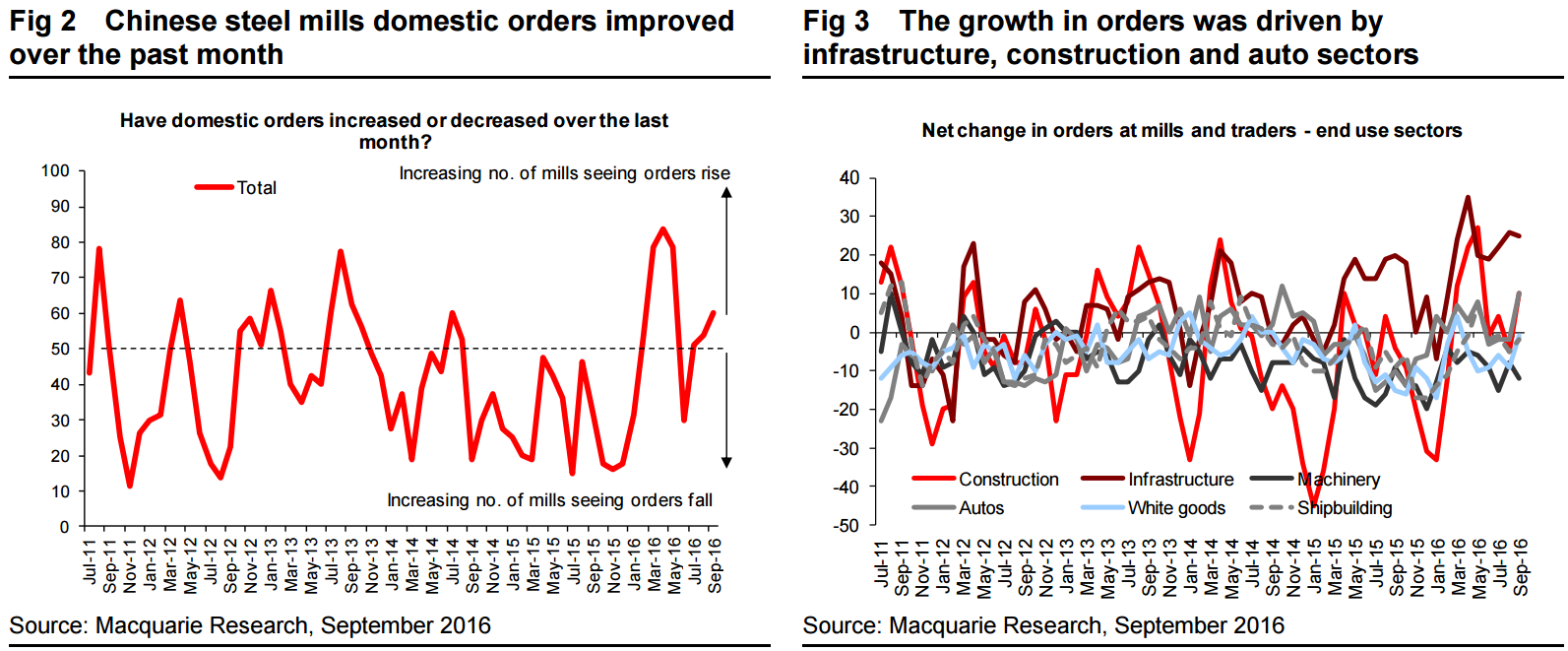

Orders and sales: Mills reported improved domestic orders over the past one month, driven by a clear pick-up in orders from infrastructure, construction and auto sectors. This is in line with the official statistics that both infrastructure and property FAI rebounded in August after a soft July (Fig 4), and auto production maintained strong growth over the same month. However, the strongerthan-expected MoM improvement in August sales means further growth in September orders may be slower given the high base.

Unlike the improvement in domestic orders, mills export orders declined for the second month through August. We understand that higher Chinese steel prices have dampened buying interest from overseas markets, and this is in line with the latest Customs data that shows that China exported 9mt of finished steel in August, down 13% MoM and 7% YoY. The decline in exports is one of the triggers for the recent steel price pullback in September. However Chinese steel mills may regain competitiveness in 4Q following the rally in the global coking coal price (note) and the recent pullback in China domestic steel prices.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.