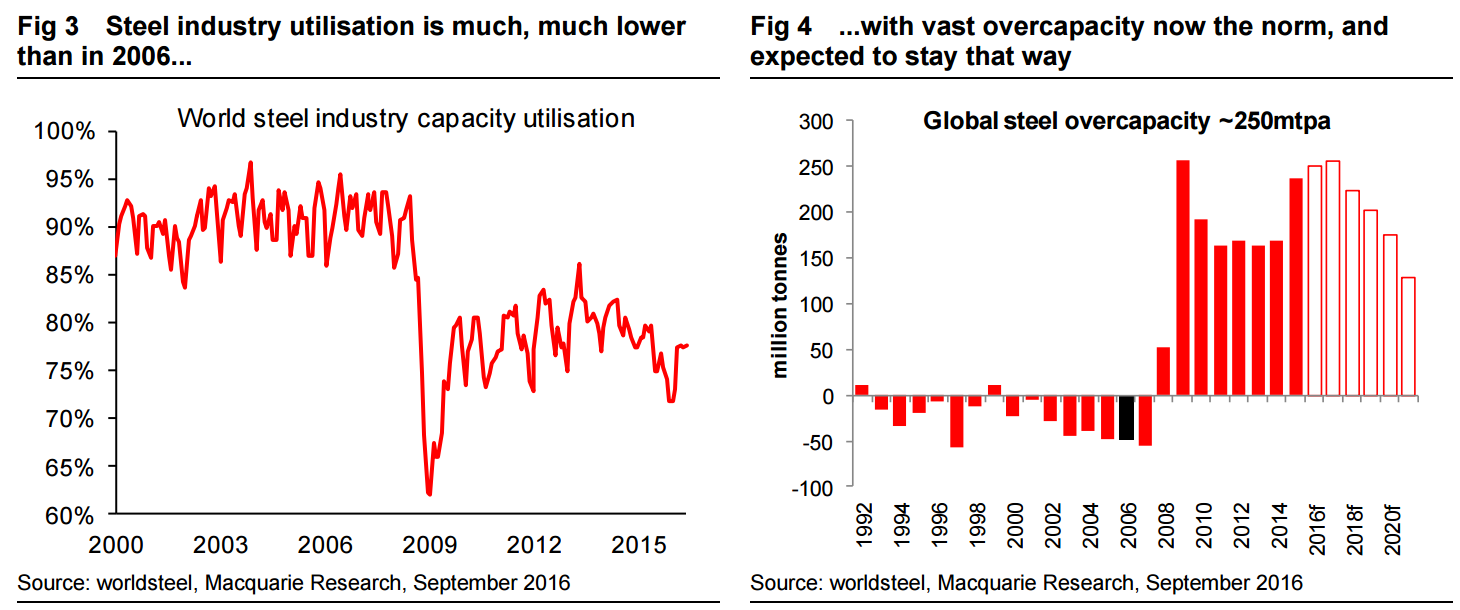

Almost exactly a decade after the merger of Arcelor and Mittal and Tata’s takeover of Corus, and steel mega-deals are back in vogue. While there are some similarities in the current deals, the market backdrop could hardly be more different. In 2006 industry capacity utilisation was touching 95% at times, and China was only a third of global output. Now, capacity utilisation is little over 75%, and China represents half of current output.

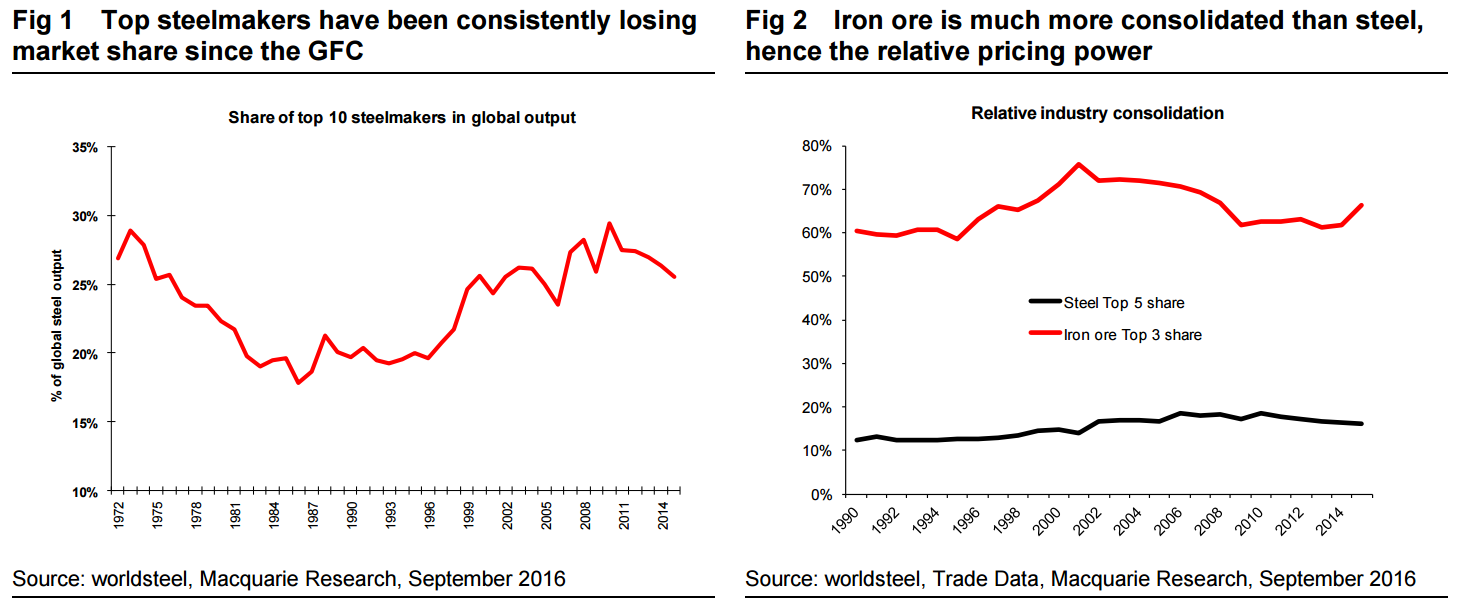

Perhaps the biggest change, however, is the focus of steelmakers in China. Back then, the industry was attracting numerous Chinese market entrants, and more fragmentation. Now, as reflected by the coming integration of Baosteel and Wuhan Iron and Steel, Chinese entities are under more pressure to start the restructuring process. This is actually the first small step towards supply-side reform, an agenda which we feel has seen limited progress to date. However, we reiterate our view that part of this aim is to make Chinese steelmakers more efficient and cost competitive on a global scale, hence our expectation for Chinese steel exports to remain above 100mtpa for the foreseeable future. Moreover, even after the coming consolidation push, steel will still look fragmented compared to major upstream and downstream industries.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.