As reported over the weekend, almost 70% of Aussies with private health insurance have considered dumping or downgrading their cover over the past year due to escalating premiums and the perception that they are being ripped-off:

Close to 80 per cent of people believe health insurance companies put profits before patients and more than 90 per cent are concerned they’re trying to “Americanise” the health system to boost their bottom line.

The new ReachTEL polling shows just how displeased and distrustful Australians have become of their health insurance providers.

The average cost of premiums has gone up by about 35 per cent since 2010, well outpacing inflation. This is believed to be a key reason why people are starting to abandon private cover…

Commissioned by the Medical Technology Association of Australia, the polling of more than 1100 people found 69.2 per cent have considered dropping or reducing their coverage. The numbers are largely in line with a recent government survey of 40,000 people.

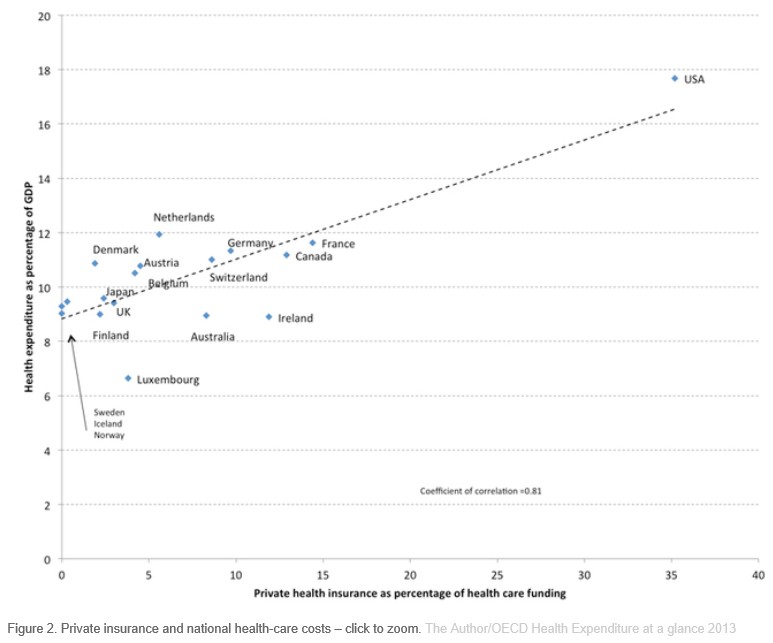

Perhaps it is time for Australia to rethink the role of private health insurance and private health care?

Every year, the Australian Competition and Consumer Commission (ACCC) releases its report to the Australian Senate on competition and consumer issues in the private health insurance industry. And every year, the ACCC finds that Australia’s private health insurance industry is characterised by market failures due to asymmetric and imperfect information, as well as significant complexity.

Since 1999 a raft of government initiatives – essentially financial carrots and sticks – have forced Australians into purchasing private health insurance.

And yet successive governments – both Coalition and Labor – have failed to articulate why Australians need a duplicate health care system, or why the federal Government subsidies to private health insurance should be so substantial.

It’s not as if private health insurance buys patients extra quality and safety. The Productivity Commission (PC) found that the larger, most comparable public and private hospitals had similar adjusted premature death ratios. Further, the PC found that the team-based care in large public hospitals also leads itself to better coordination of care.

In fact, in Australia’s case, private health insurance is likely raising overall health costs. This is because the high financial overhead of private insurance means that only 84 cents in every dollar collected by private insurers is returned as benefits, with the rest going to administrative costs and corporate profits. By contrast Medicare returns 94 cents in the dollar, even after the cost of tax collection is taken into account.

A single national insurer, like Medicare, also has the monopsony buying power to control prices demanded by powerful service providers.

The 2015-16 Budget Papers showed that the cost of the private health insurance rebate will rise from $6,228 billion in 2013-14 to $7,061 billion by 2019-20 – an increase of 13%.

Where is the evidence to show that spending taxpayer money in this way is superior to expanding funding to the public system?