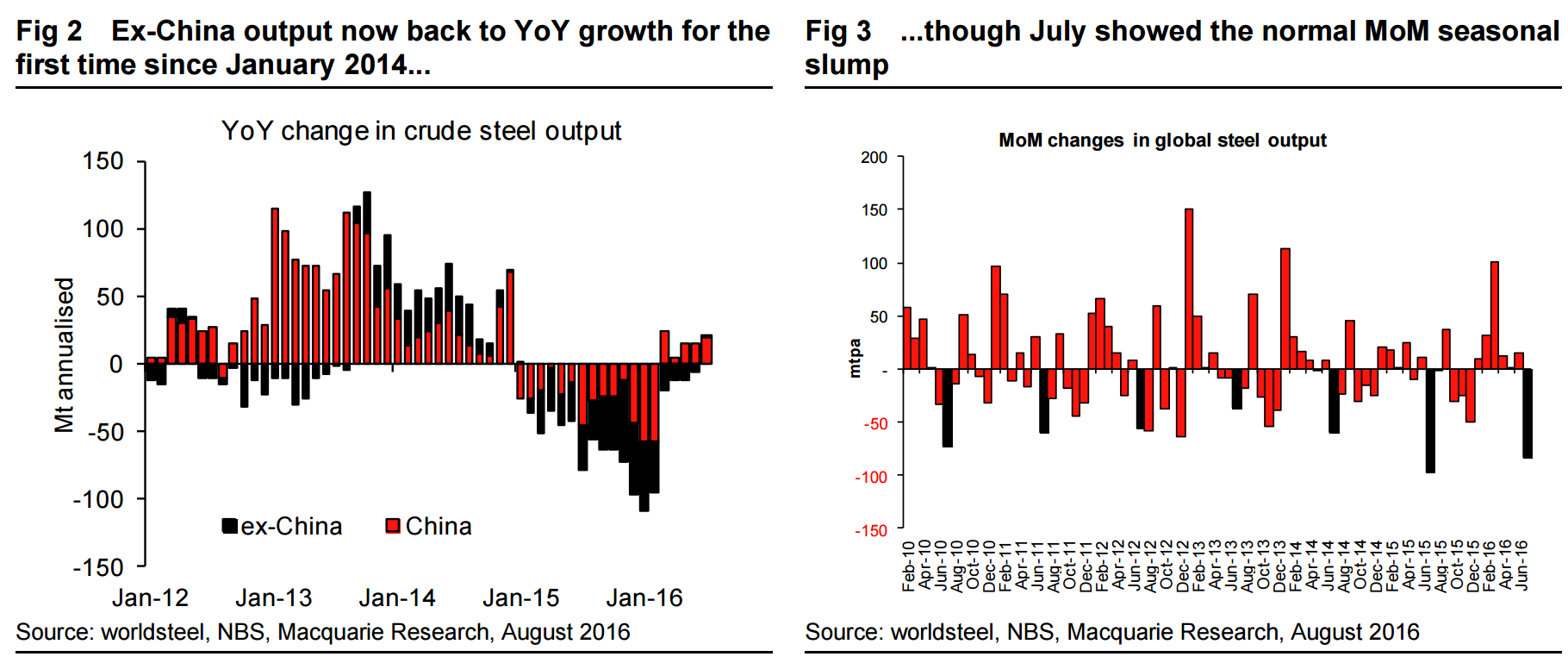

July’s global steel crude output data, as released by worldsteel yesterday, shows world ex-China output to have recovered to positive YoY territory for the first time in over 18 months. This, coupled with China’s relative resilience reinforces the view that the global industrial recovery is gathering some momentum – something we covered in more detail in a recent Commodities Comment and our Global Macro Outlook.

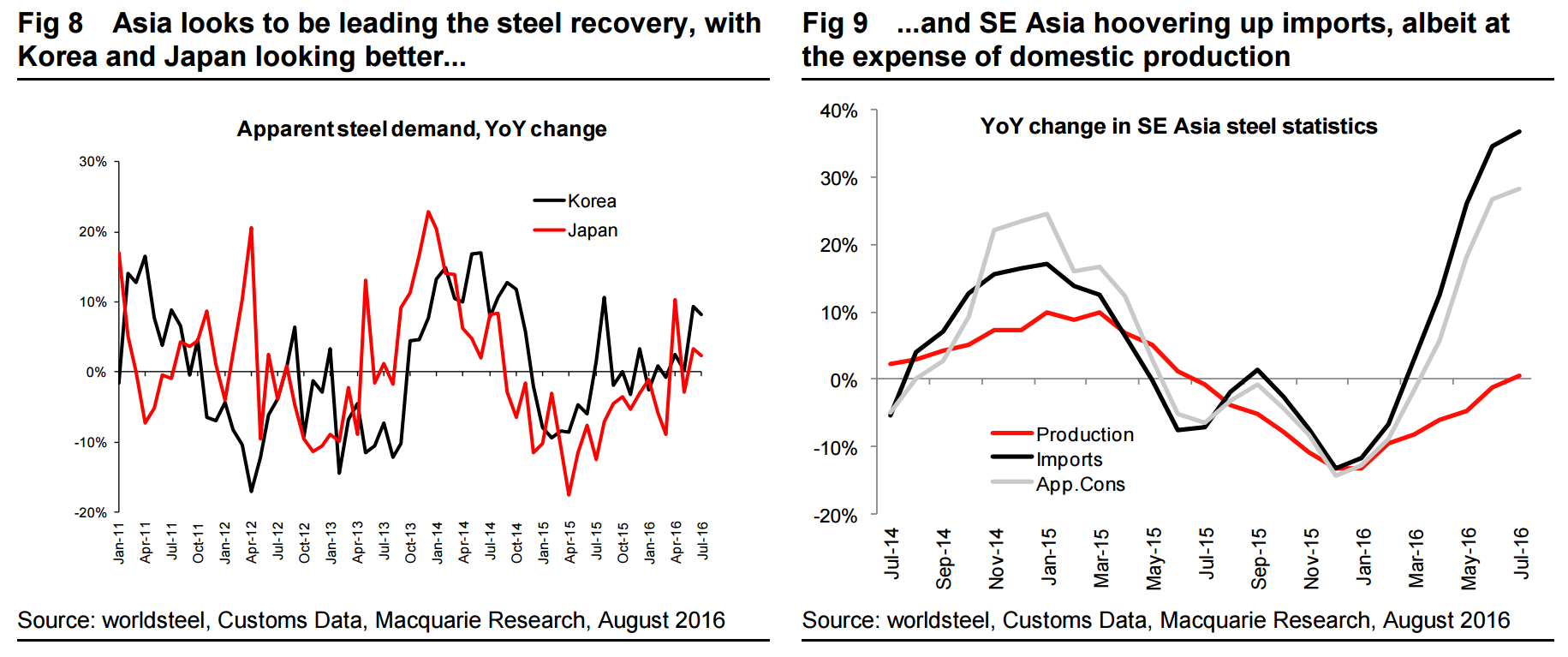

However, looking behind the headlines does suggest some winners and losers. Asia is clearly leading the recovery, with Korean and Japanese consumption trending back into positive territory. Also, demand from smaller countries looks to be very strong, though whether this has been encouraged by lower prices or forced through Chinese exports is still in question. We reiterate our view that import regions will struggle to swallow any more steel.

In contrast, the areas which look to be struggling for demand over the past couple of months are Germany and the US. For the former, the usual summer slump makes comparisons difficult, but even so YTD consumption is running down 5%. For the latter, the tariff-induced higher prices are certainly keeping steel demand in check even with an improving domestic economy.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.