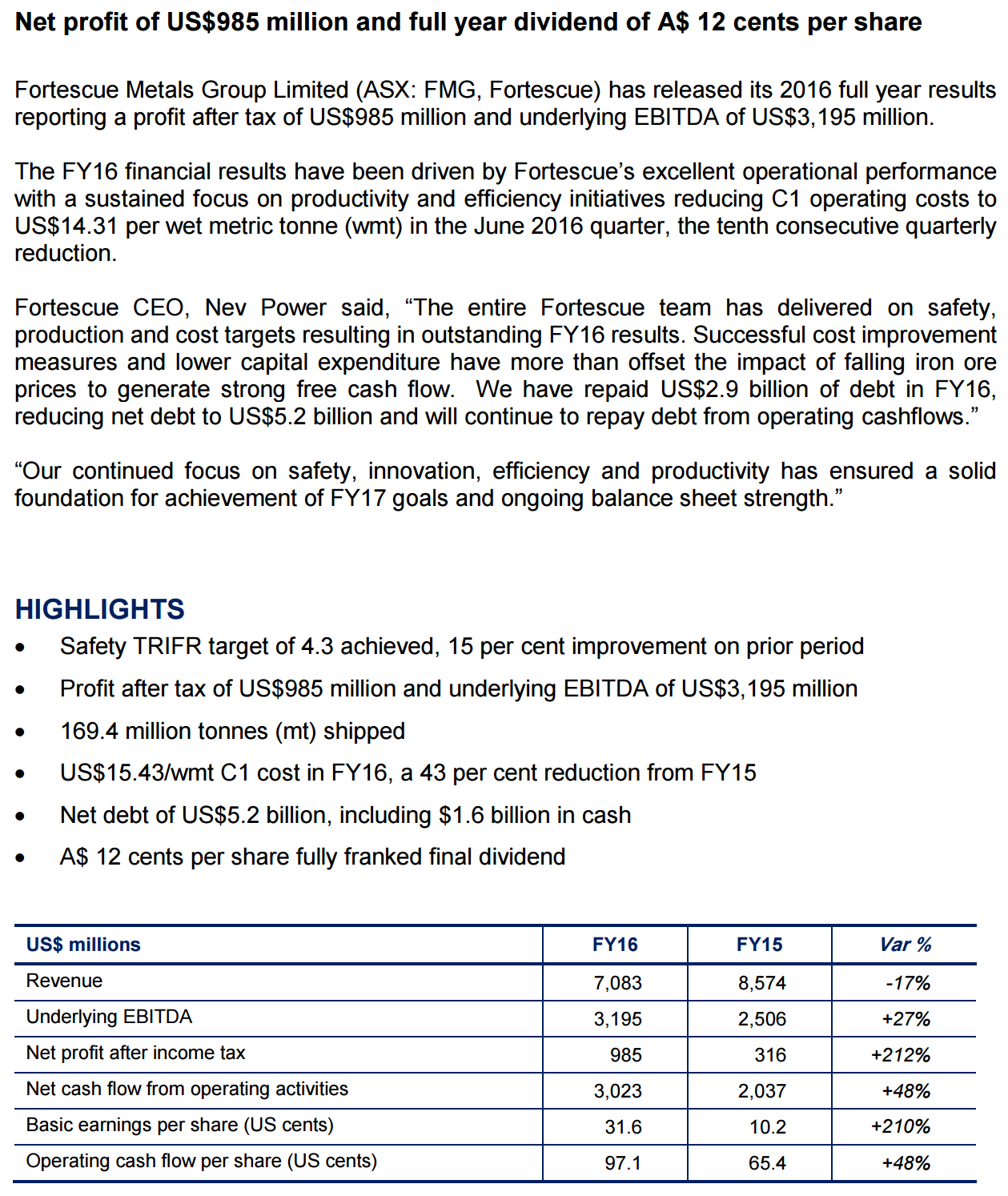

Fortescue’s full year is out:

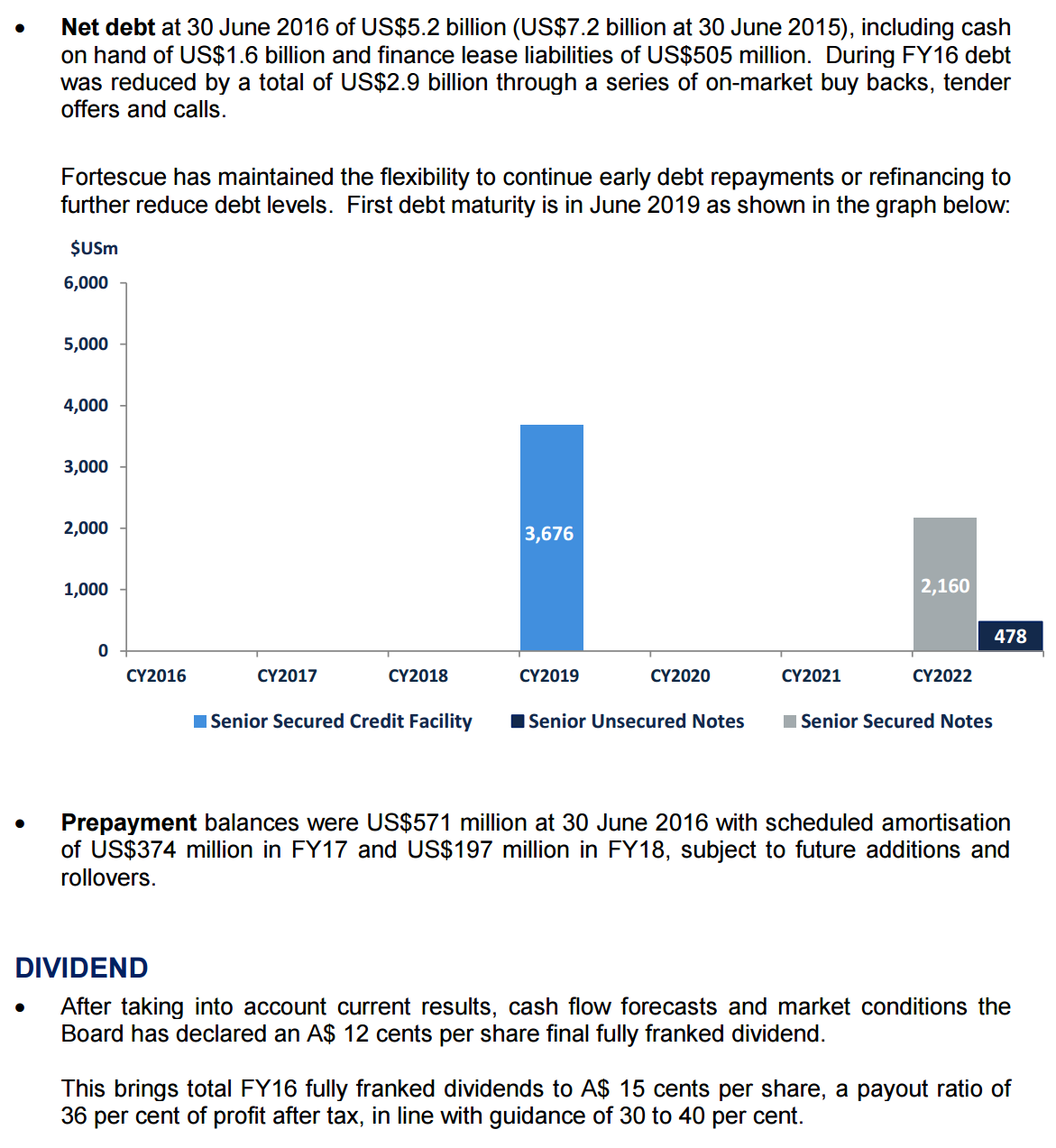

So ends one the most extraordinary corporate transformations in modern Australian history. From a $90 all-in breakeven fours years ago, FMG is now in the low $30s. In 2012 the firm was negotiating with banks to waive debt covenants and cancelling expansion plans, today it has nearly halved its total debt from $13bn despite the iron ore price falling 50% over the same period. Hard work, innovation and good luck saved it.

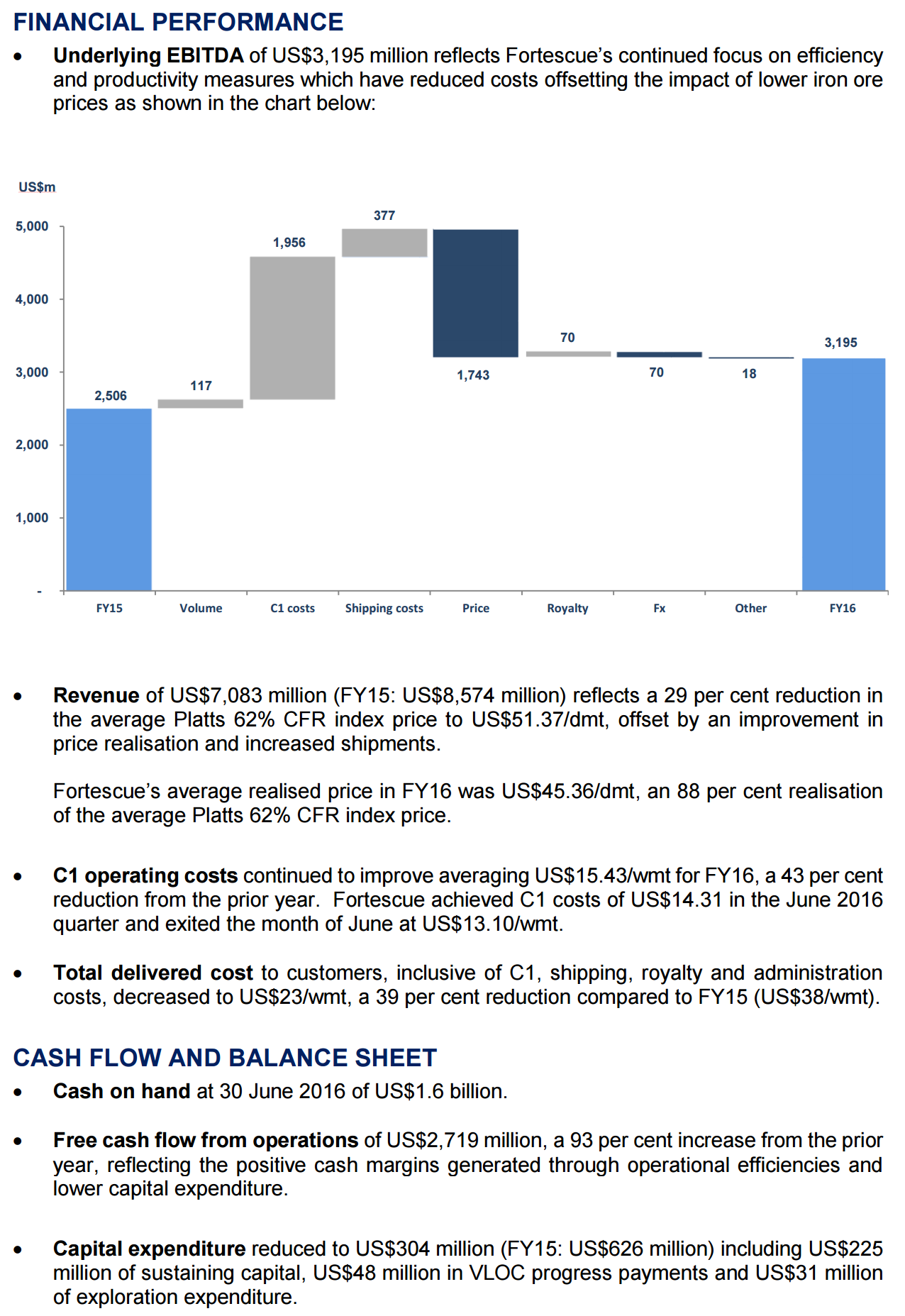

Yet this result will likely disappoint markets. The dividend is only 3% versus the sell side looking for as high as 6%. The cost reductions are now all but over and the future of the iron ore price remains as troubled as ever. So much so that the dividend is very unlikely to persist for long.

In the long run, the miner will struggle to hold costs so low, and it will still very likely end up as the marginal cost producer as Chinese steel output marches lower towards 600mt over the next decade.

It’s a brilliant miner, great innovator, and very determined firm. But is still uninvestable over any time frame beyond your nose.