Friday’s Statement on Monetary Policy (SoMP) by the RBA contained the below analysis of China’s housing recovery, which the RBA concludes has been driven by stimulus measures and is not sustainable due to too many unsold homes and not enough “fundamental” (owner-occupied) demand:

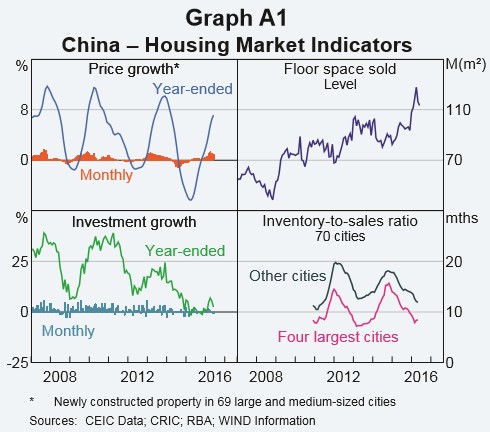

Dwelling investment has made a significant contribution to GDP growth in China over recent history. Developments in the Chinese housing market affect demand for Australia’s exports of iron ore and coking coal owing to the steel-intensive nature of residential construction. Conditions in the Chinese housing market have picked up since the start of 2016 (Graph A1). Housing price inflation has risen, sales (measured as residential floor space sold) have grown rapidly and housing investment has strengthened after a period of weakness. The ratio of unsold inventory of developers to sales has declined, although the stock of unsold property remains high.

Government policy has played an important role in Chinese housing market cycles and a range of stimulus measures implemented since 2014 has contributed to the latest strengthening of conditions.1 These policies have encouraged purchases of housing with the goal of reducing inventory levels, which have been high in many parts of the country (Graph A1). In September 2015, the minimum down payment for first-home buyers was lowered from 30 per cent to 25 per cent in most cities and a further discretionary 5 percentage point cut was authorised in February 2016. Minimum down payments on second properties were reduced from 60–70 per cent to 30 per cent over the same period. Benchmark lending rates have been cut by around 165 basis points since late 2014, and the estimated national average mortgage rate (a measure of rates actually paid) has fallen by an additional 70 basis points relative to these benchmarks. Property transaction taxes have been reduced and there have been targeted easing measures in some areas, such as subsidies for certain types of home buyers. However, local authorities in some areas have more recently introduced measures to temper strong housing price increases, as discussed in more detail below.

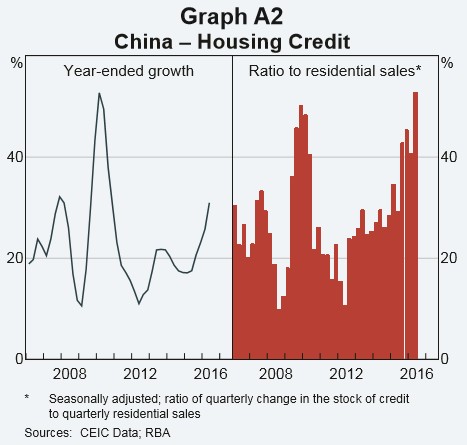

Following these earlier stimulatory measures, housing credit has grown rapidly, rising by more than 30 per cent over the year to June 2016 (Graph A2). Housing credit has also increased sharply relative to the value of property sales, suggesting that buyers are using more leverage to purchase property. Investor demand for housing appears to have contributed to the recent strength in many local housing markets. One likely reason for this is the perceived lack of alternative high-yielding investments, particularly given the unwinding of the equity market boom and declines in yields on wealth management products since mid 2015…

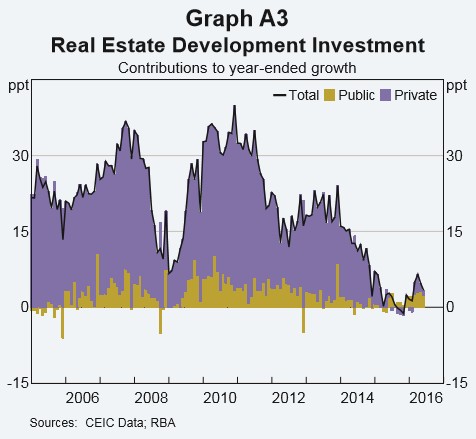

State-owned firms have contributed noticeably to the recent pick-up in real estate investment and there have been reports of some state-owned developers purchasing inventory from troubled private developers (Graph A3)…

Housing price growth has been weaker and inventory remains highest in smaller cities, reflecting more limited employment opportunities and high levels of dwelling construction relative to demand…

Given the large stock of unsold properties nationally, any slowing in demand from current levels would pose potential risks for property developers and upstream suppliers of raw materials to residential construction. The recent pick-up in sales has facilitated some reduction in developers’ inventories. Yet land prices have been rising relative to housing prices in a number of cities, potentially squeezing developer margins, and the degree of gearing has continued to rise for mainland-listed developers. Developers have diversified their funding sources in recent years, decreasing their direct reliance on bank lending. Given the dominance of banks in China’s financial system, it is likely that they are still indirectly exposed to much of this lending.3 A downturn in market conditions, brought about either by a reduction in the degree of policy stimulus or a loss of confidence among home buyers, could therefore increase credit default risks for financial institutions…

In summary, despite the pick-up in housing market conditions since the start of 2016, there remains a significant stock of unsold housing in many cities and there may not be sufficient fundamental (owner-occupier) demand to support a reduction in that unsold stock. The apparent contribution of government stimulus measures to the recent strength in the Chinese housing market raises doubts about the sustainability of the recovery, particularly for investment…

The inevitable downturn in Chinese housing construction will, therefore, likely drag down demand (prices) for Australia’s exports of iron ore and coking coal.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.