The Brent oil price is still sick down marginally at $41.94 as I write. Henry Hub fell as well to $2.73mmBtu:

The only data was from API which showed draws in US stockpiles and was mildly bullish. Broader news flow was bearish with Nigeria returning to its bribing strategy for militants, from Reuters:

Nigeria’s government has resumed cash payments for former militants in the restive Niger Delta, an official said on Monday, in a bid to end a wave a wave of militant attacks on oil and gas facilities.

In February, Nigeria stopped the payments for former militants who agreed under a 2009 amnesty to stop blowing up crude pipelines in exchange for cash, the official said.

The government says it has been holding talks with militants they suspect of being behind a recent wave of attacks on pipelines that has reduced Nigeria’s crude output by 700,000 barrels a day.

“Payments of stipends to the ex-militants resumed this Monday. The payments are done directly from the CBN (Central Bank of Nigeria) to their bank accounts,” said the amnesty program’s media officer Piriye Kiyaramo.

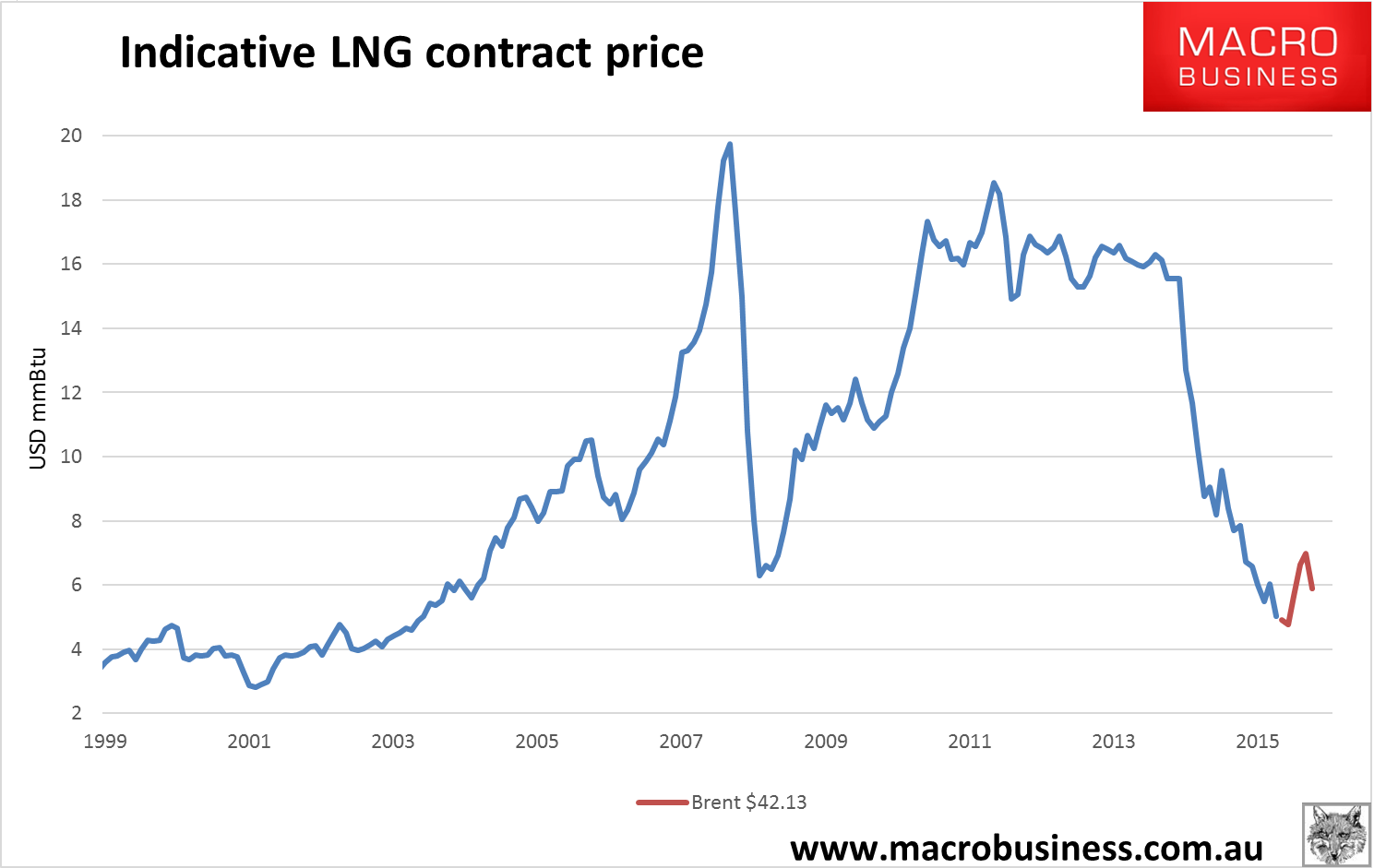

Turning to LNG, the indicative oil-linked contract price hit a new low of $5.87mmBtu:

Lots of news on producers with:

- Petronas rethinking Canada’s only big project still going ahead;

- Japan looking at more Russian production;

- India really charging producers for discounts;

- Sabine Pass firing up train 2.

Most interesting, China’s Sinopec has doubled its unconventional gas targets, from the WSJ:

Sinopec’s push now, amid a global oversupply of gas, presents an unpleasant surprise for an industry already in turmoil. If it succeeds, China’s need for imported liquefied natural gas might dwindle—potentially jeopardizing tens of billions of dollars in planned investment from Canada to Papua New Guinea.

China has huge shale reserves, but challenges from complicated geology to an inadequate pipeline network long made tapping them elusive. But with stifling pollution in many cities, natural gas offers a cleaner alternative to coal. Developing this industry will also help protect jobs at home.

Much of the planned Chinese expansion will come from the Appalachia-like region near Fuling, in central China, where tobacco plots are nestled among rolling hills, and where underground rock formations hold some of the biggest reserves of shale gas outside North America.

Sinopec’s investment is transforming a region caught between China’s past and its future. Farmers in sandals plod along winding country roads, woven baskets hitched to their backs. In Jiaoshi, Sinopec’s local base, workers in red jumpsuits clutch iPhones along the town’s main street, named after a Sinopec oil field.

Gas production will top 5 billion cubic meters this year, up from 3 billion in 2015. By 2017, Sinopec aims to raise Fuling production capacity to 7 billion.

The company’s shale push is helped along by government subsidies and political support—meaning there is less environmental debate around shale-gas production than in the U.S.

That’s only 5mt of LNG equivalent so it’s not going to kill anyone but we can see the kind of set-up here that has disrupted other markets: government subsidy, expanding into oversupply, jobs etc. It’s worth watching.