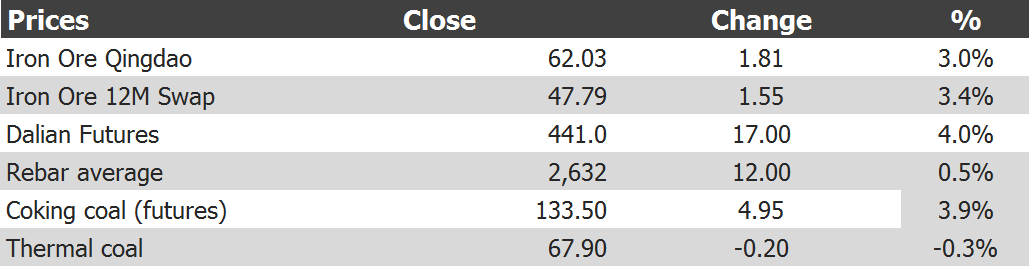

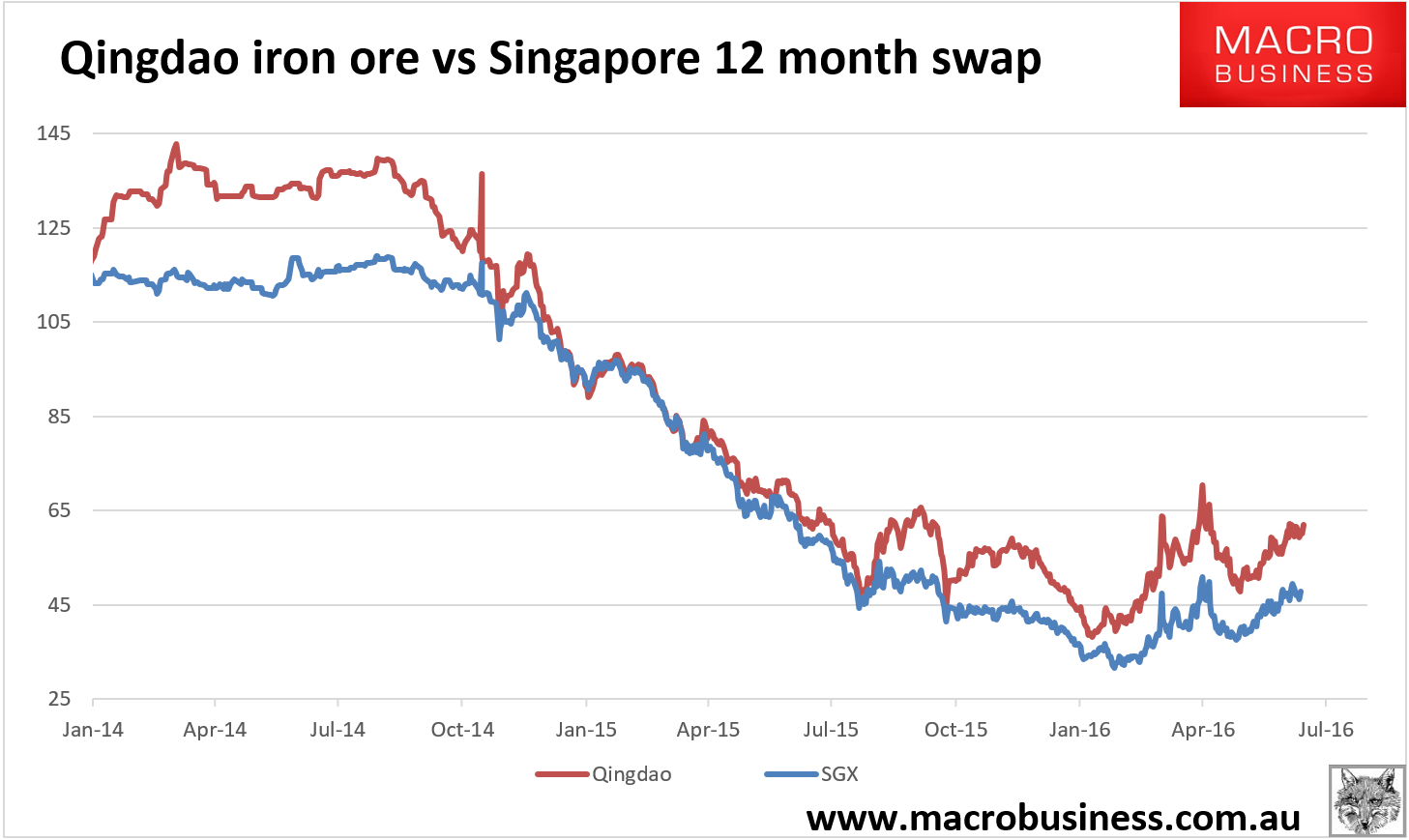

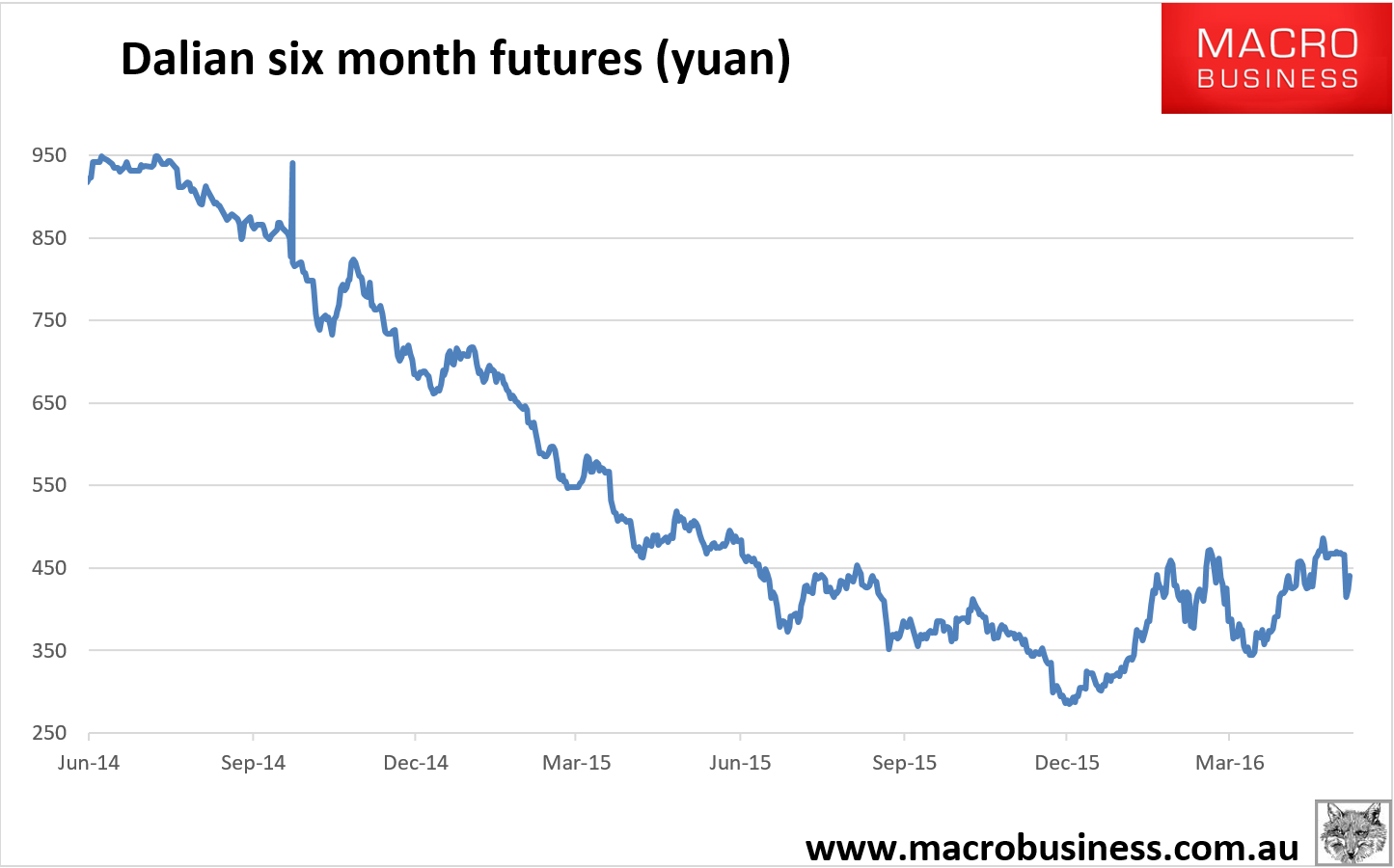

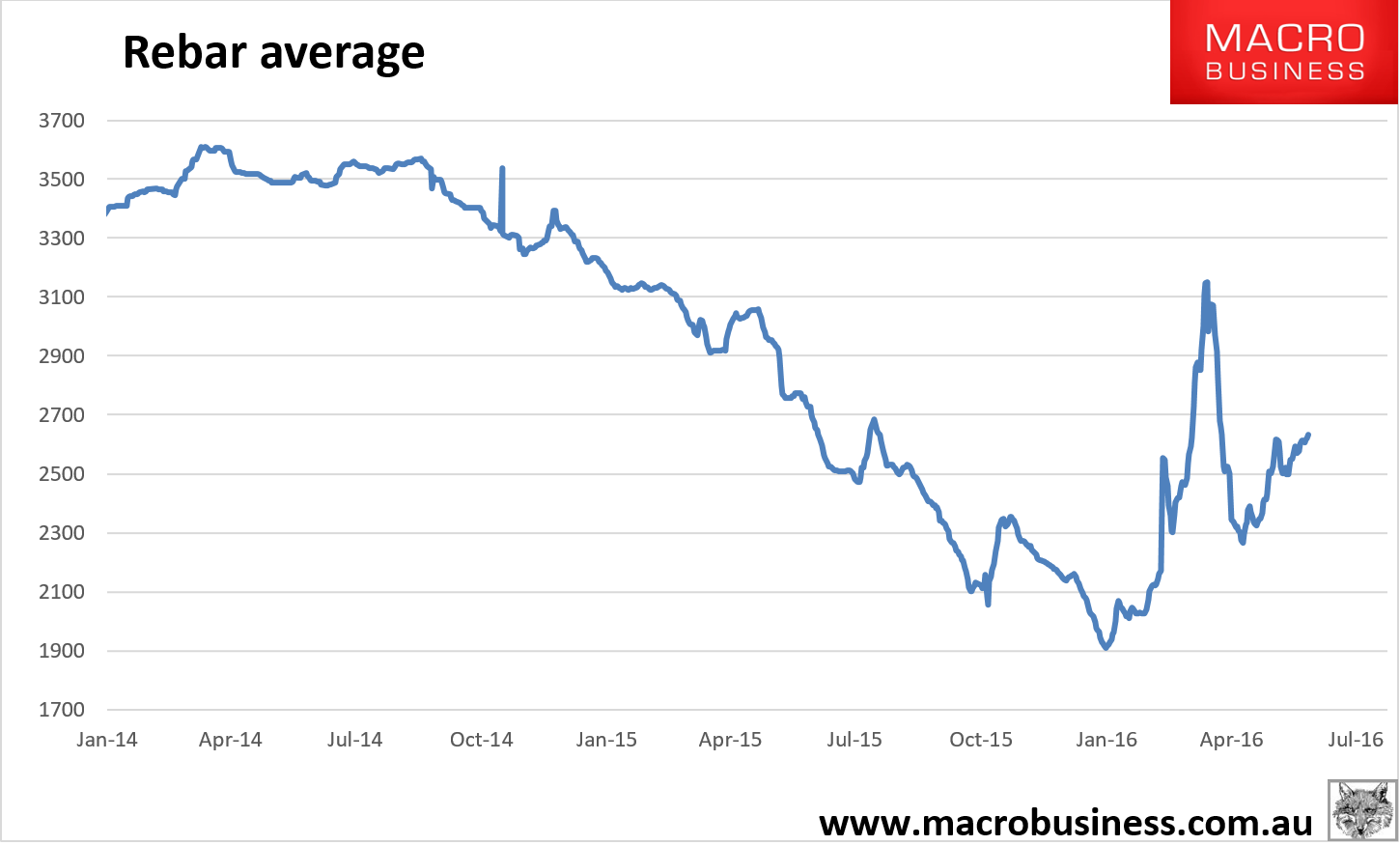

Sorry this is late. Forgot to hit “post”. Iron ore charts for August 16, 2016:

Tianjin benchmark up 3% to $61.80. Spot isn’t falling when Dalian does but it is rising when it rises. Rebar is soldiering on. The ease with which the market has shrugged off last week’s lousy Chinese data shows bulls in control. I don’t know how far they’ll get before reality bites. This gent thinks it’ll run all next year:

Manufacturing makes up roughly one third of Chinese steel consumption so it would help to see it grow but it is clearly secondary to what happens to the other two-thirds used in construction. My outlook on that front remains slowing henceforth until another possible can-kick early next year but that will coincide with the arrival of roughly 60mt of new seaborne iron ore supply (ex-Samarco) so I can’t see $70 even if we get more stimulus. More like $50 in H1 falling to $40 in H2.

Axiom Capital’s Gordon Johnson, a noted bear on iron ore and steel–and the stocks of companies like U.S. Steel (X) and Cliffs Natural Resources (CLF) that produce them–sees a crash in iron-ore prices coming as soon as the next four to eight weeks. He explains why:

With: (a) more iron ore supply coming in 2H16 and 2017, (b) speculation in China’s iron ore futures trading market (via the Dalian stock exchange) at a record high (and likely to end soon), (c) what appears to be a peak in China’s port stocks (which has been a crucial harbinger of price pressure over the past several years), and (d) demand for iron ore on the decline (measured by China crude steel output), we see the next crash in iron ore prices as 4-to-8 weeks out. As investors refocus on the factors that drive fundamentals in the iron ore market (and away from perpetual stimulus expectations – stimulus has failed to drive economic growth over the past 19+ months measured by GDP in many of the world’s most aggressively stimulated economies below 2% at present), and speculation in China’s iron ore futures market fades, we expect iron ore prices to eclipse the lows set earlier this year (i.e., sub-$40/mt) before “Santa Claus come barreling down the chimney” (i.e., December 25th, 2016).

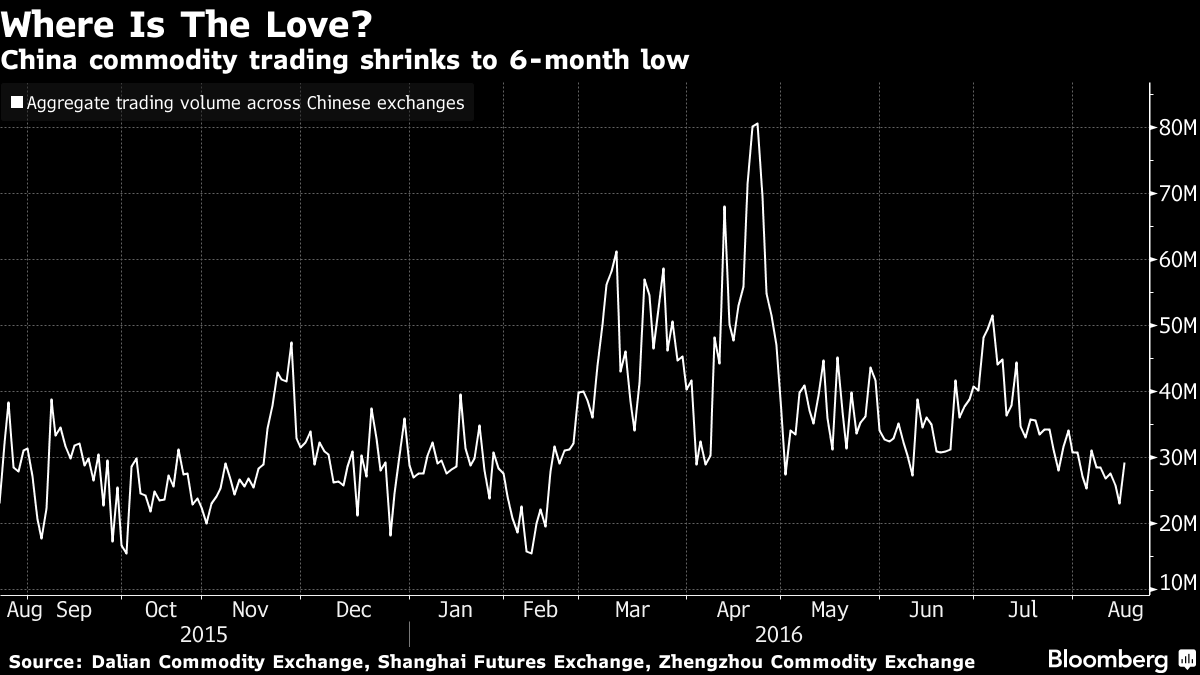

Interestingly, if Banana Man is still loose in the Dalian exchange, it’s not showing up in volumes, from Bloomie:

Chinese traders are falling out of love with commodities.

Aggregate volumes across the nation’s three biggest exchanges have shrunk to the lowest level in six months, a shadow of the fevered trading in March and April when retail investors charged into markets for everything from iron ore to cotton, driving up prices and stoking fears of a bubble. Chinese authorities brought an end to the frenzy by introducing curbs on excessive speculation and trading has failed to recover since.

Does that presage price falls or rising real demand in today’s strong price action? We’ll know soon enough.