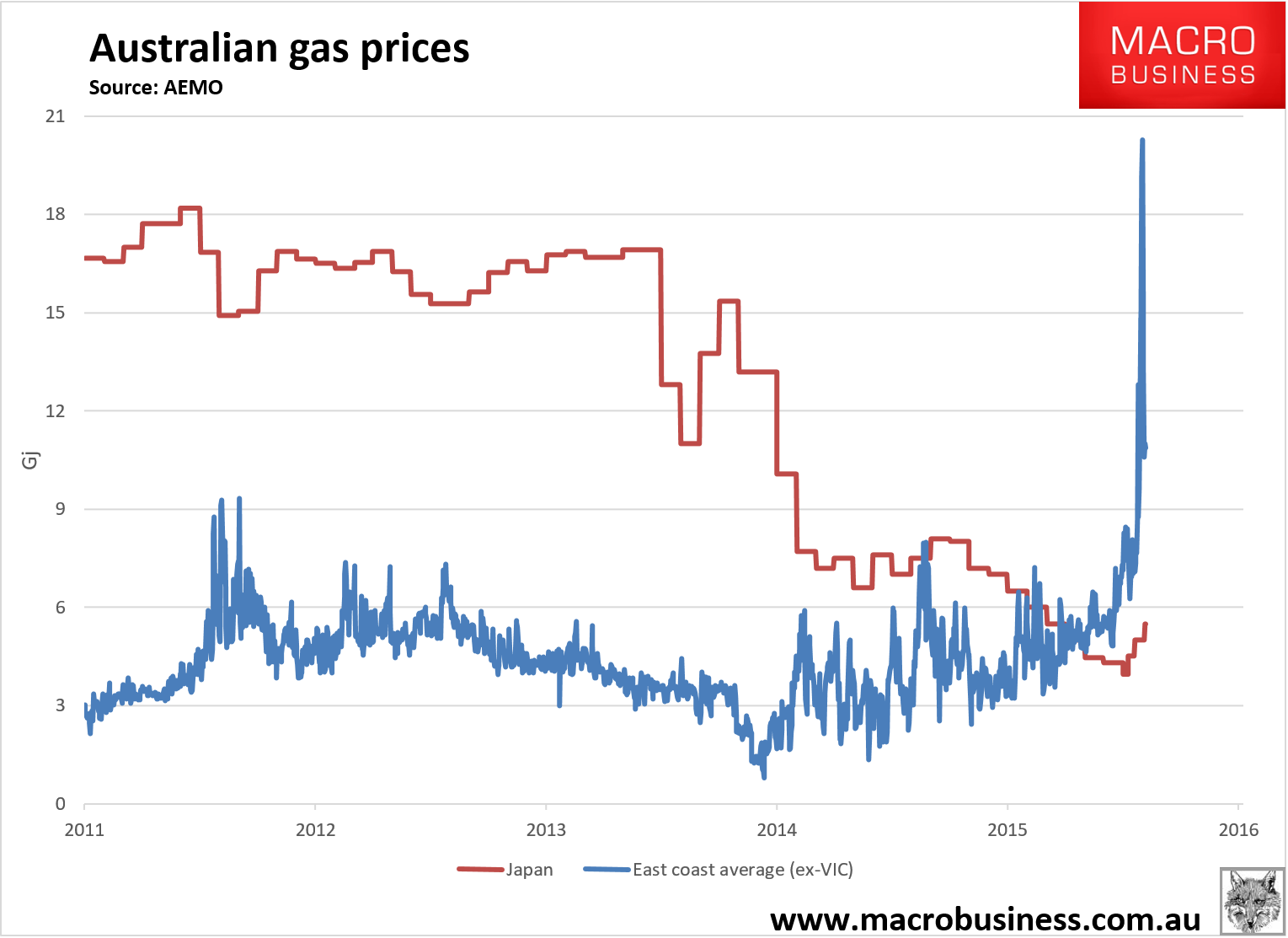

Another shocker of a week for gas users with MB’s east coast average price still at an astonishing $10.86Gj for spot markets while in Japan the same Australian gas can be purchased for $5.75Gj:

It will be very interesting to see where the price gouge settles as the east coast cold snap passes. The price trend is very clearly up in all eastern states.

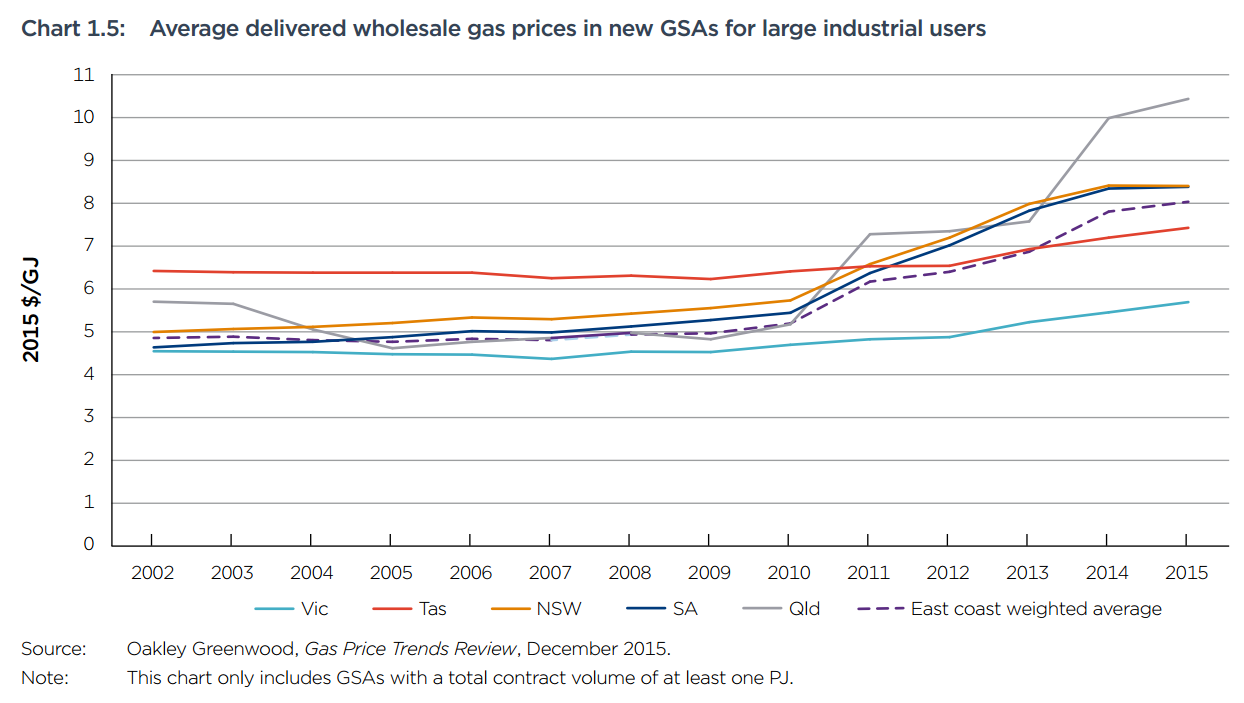

So, while Japanese consumers and industry are enjoying a golden age of cheap gas hovering above $5Gj, we at home are taking it right in the team, especially industry. The recent ACCC report into the east coast gas market showed how much:

To sum up:

- $80 billion dollars has been burned on three LNG plants in QLD that make no money;

- but, they are a part of an east coast gas cartel that can charge whatever they like at home given their exports have generated a shortage;

- that is, locals are subsidising the export losses of Banana Republican gas titans who mis-allocated this much capital piled upon pallets:

- and, to boot, we’ve given ourselves epic Dutch disease because our manufacturing is driven out of business owing to cheap gas in Japan (and everywhere else but here).

This rates as one of the most singularly stupid and rapacious examples of the “resources curse” anywhere in the Third World which, frankly, is where our policy-makers seem to have learned their craft.

So, what’s the answer:

- the ACCC and rent seekers want more gas supply but NIMBYs won’t let them, with the fair point that unconventional gas could poison the water table;

- the LNG industry has suggested eastern cities build LNG intake terminals so they can trade on the global market where gas is cheaper but that means we will be permanently embedding the price of freezing, shipping and unfreezing our own gas in the local price thus erasing any gas advantage we ever had permanently and fattening the margins of the same cartel;

- we apply domestic gas reservation to the cartel (or break it up).

At this point we can probably all see where this is going. Governments clearly do not care so we’ll see the following play out:

- industrial gas users will go out of business, leading to falling consumption that will take some pressure off prices in the medium term. In fact, this is precisely the forecast of the AEMO;

- over time, however, the gas reaming will spark a fuss over rising household electricity bills, at which point panicked governments will rush to build LNG regasification plants along the eastern seaboard;

- that will, of course, embed higher costs for Australian gas permanently given it will instituionalise the price of freezing and unfreezing the gas, but at least it will prevent the kind of monstrous gouging we are seeing now because the global price will set the local price.

It would be better policy to install a domestic gas reservation framework or to simply buy one of the gas carteliers and force them to compete with a government corporation. I have no compunction with either because what we looking at here is a total market failure.