Rising inequality has gone hand-in-hand with trends that have been helpful for investors – notably the fall in corporate labour costs and the rise of excess saving, which in turn has led to rates trending down. Rising inequality is also one factor behind rising political risk. Political risk is one factor behind my view that the medium-term risk-reward trade-off for equities is not very attractive.

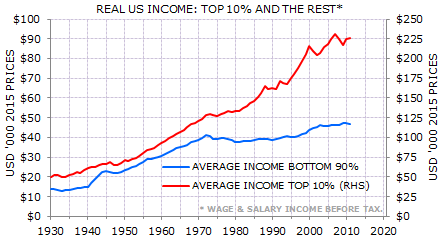

It’s increasingly well-known that income gains in developed economies over the past 35 or so years have been unequally distributed. Labour income has fallen as a share of GDP in most economies. The distribution of labour income has itself become more skewed, with significantly weaker growth in the bottom 90% of income earners (Exhibit 1).

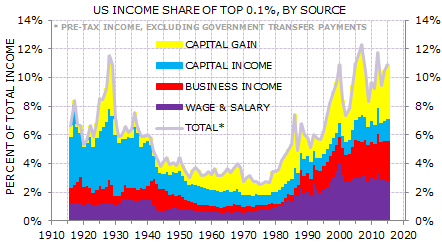

Inequality is greater when account is taken of capital income. Broadly speaking, the higher the income the larger the gain. Exhibit 2 shows the share of income going to the top 0.1% in the US.

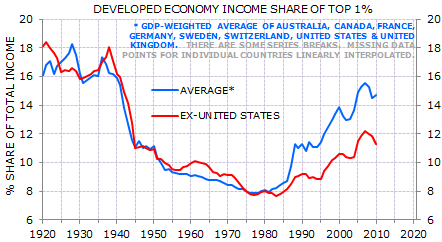

Inequality has increased throughout developed economies over the past 35 years, although not to the same extent as in the US. The share of total income going to the top 1% of income earners is now at a post-1945 high (Exhibit 3).

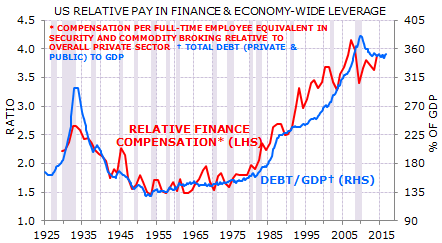

Several factors are behind the rise in inequality. The rise of finance is one (Exhibit 4).

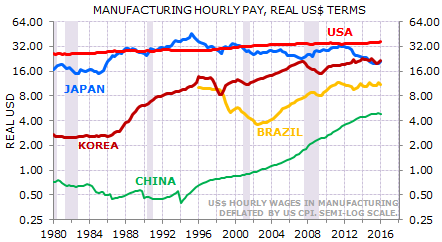

A second is globalisation. This worked as theory suggested it would work: increased trade led to the returns to the factors of production converging. Labour is one factor of production. Exhibit 5 shows average pay in manufacturing in a selection of economies. Note that this is a log scale, so real hourly pay in Chinese manufacturing has increased tenfold over the past 25 years. (Also note that currency movements explain some of the relative changes, notably the cycle in Japanese manufacturing pay is largely due to the dollar-yen exchange rate moving.)

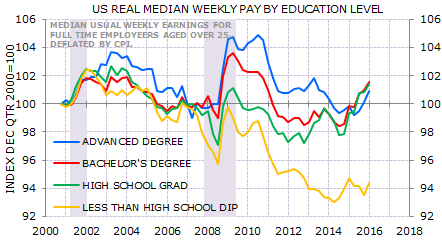

Immigration is a third factor. Immigration and trade squeezed unskilled workers’ pay. Their pay has fallen in real terms in the US (Exhibit 6).

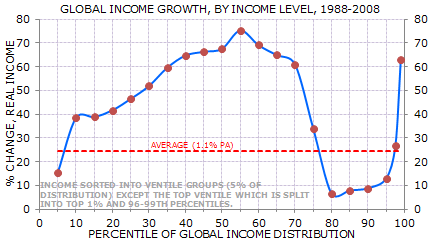

Exhibit 7 shows global income growth by income level. The slowest growth has been around 80-90 percentile of incomes – broadly speaking, the lower income earners in the developed economies.

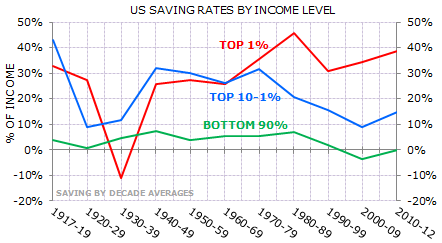

These trends have helped investors. Falling labour share boosted listed-sector profits. (Better still, this did not apply to finance. That, ahem, may be changing.) Increasing inequality tended to increase saving, as higher income earners have higher-than-average saving rates (Exhibit 8). The key to secular stagnation is the imbalance between planned saving and planned investment – so rising inequality is one factor behind the developed world’s current funk.

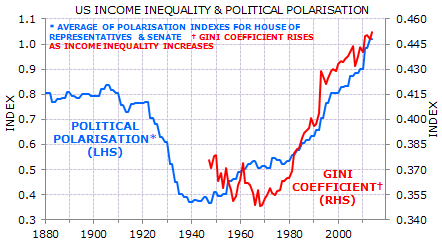

Rising inequality has also gone hand-in-hand with rising political polarisation. Exhibit 9 shows an index of political polarisation in the US (based on Congressional voting records). Polarisation and political pushback against the trends of the past 35 years are becoming more widespread.

Financial markets are poor at calibrating political risk. The S&P500 at an all-time high on the same day Donald Trump became the Republican’s presidential nominee suggests that markets are not, for now, discounting much for political risk.