From Westpac:

The Deloitte Access Economics “Investment Monitor” provides a detailed snapshot of Australia’s investment project pipeline. The database contains details on 1,073 projects valued at $20mn or more, as at June 2016. Here we provide an update of the key results.

Note, the full value of a project is included in the investment pipeline until the project is either completed or deleted. This differs from official estimates of the existing “work pipeline”, which is the value of work yet to be done on a project currently under construction.

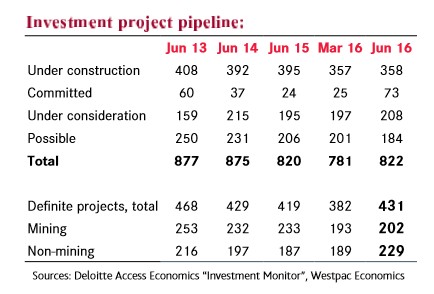

The Investment Monitor estimates the total project pipeline to be $822bn at present. That is a $42bn increase on March, reversing declines over the second half of 2015, to be $2bn higher than a year ago.

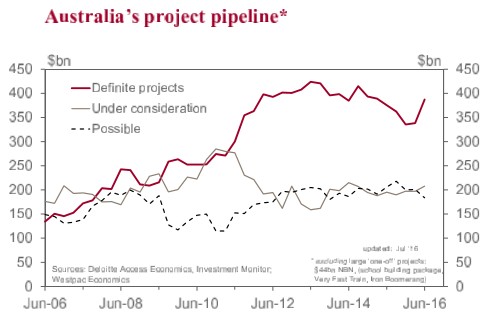

Significantly, the value of definite projects (those either under construction or committed) rose by $49bn to $431bn, to be $11bn above a year ago but $37bn below the peak of three years earlier.

Potential projects (either under consideration or possible) are valued at $391bn, some $10bn lower than a year ago.

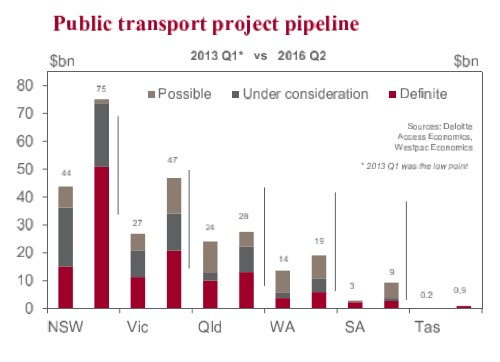

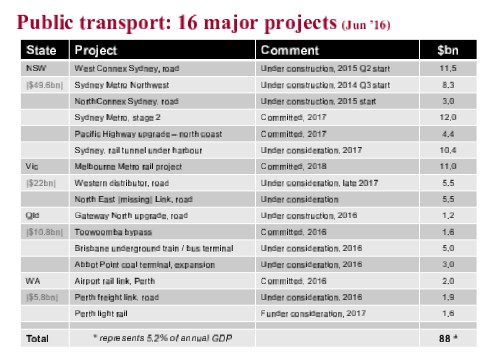

As we have highlighted previously, the project flow is changing course on a stream of new public transport initiatives. That was the clear theme in the latest update.

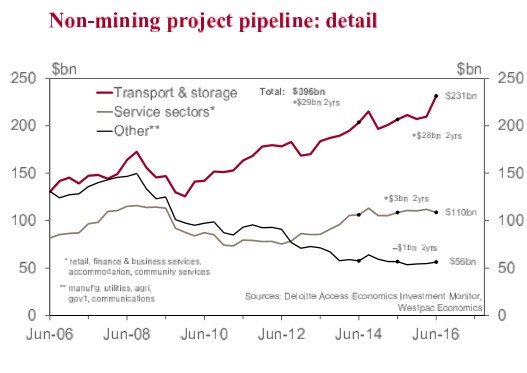

In June, $39bn of the $49bn increase in total definite projects was explained by public transport initiatives. Following the round of annual state budgets, there are now 29 public transport projects at the committed stage, with a combined value of $44bn, up from 19 with a value of $5bn in March. The transport & storage investment pipeline in total is $231bn, dominated by the public sector, $190bn.

The oil and gas sector accounted for the remaining $10bn increase in definite projects in June, most of which was a $7.6bn cost blow-out on the Inpex Ichthys gas field project to $45bn. Phase 2 of the Greater Western Flank project in the Pilbra WA, valued at $2bn, entered the database in June, at the committed stage, with a 2016 H2 start date.

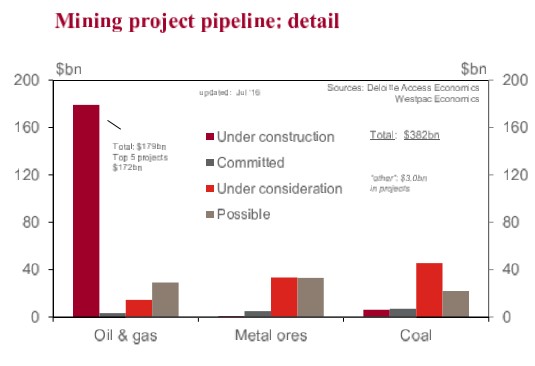

The mining project pipeline, totalling $382bn, of which $202bn is at the definite stage, will thin considerably when the 5 remaining mega gas projects, with a combined value of $172bn, are completed over 2016 and 2017, with potential slippage into 2018.

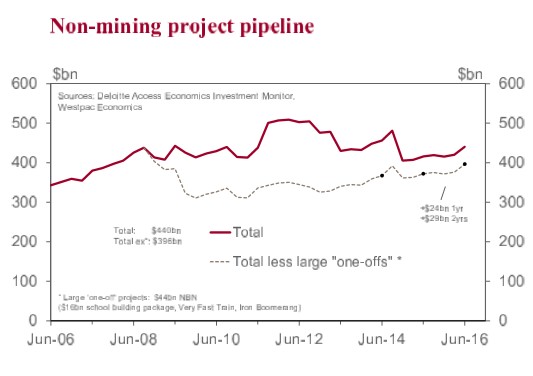

The non-mining investment pipeline (excluding transport and ex the $44bn NBN), is $165bn, unchanged over the past two years. Of that, $80bn is at the committed stage, up $2.4bn on mid-2015. Notably, the investment pipeline of accommodation projects, with the low AUD boosting tourism, is valued at $23bn and while that is unchanged on a year ago there has been some transition to the committed stage, up $3bn over the year to be $5.6bn.