By Chris Becker

Higher than expected earnings in the US is pushing the USD higher taking most risk markets with it, as speculation mounts the ECB will step in later tonight and enact further stimulus, following the IMFs downgrade to growth post-Brexit. Currency markets continue to go haywire, with the Turkish Lira falling again after a big sovereign downgrade (or should we ignore that one too Mr Pascoe?), Pound resurging, NZ dollar down on the RBNZ dovish economic outlook and an Australian dollar now in the 74 cent handle against USD. Commodities were mixed, with most industrial metals sold off, including gold/silver on the stronger USD, while oil finished where it started following the better than expected DOE inventory report.

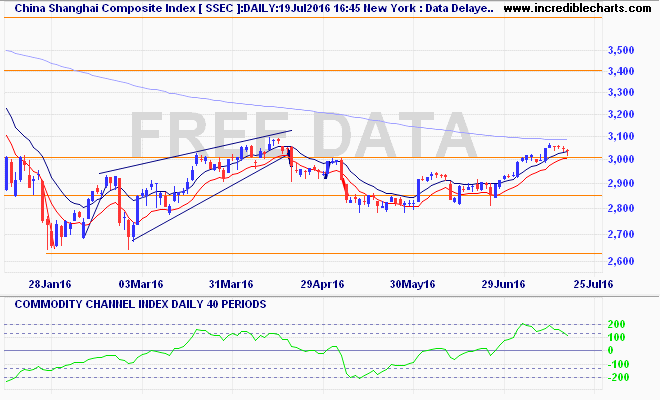

Recapping Asia first where the Shanghai Composite slipping again, down another 0.25% to close at 3026 points, still unable to clear the 200 day moving average. I contend a reversal is on the cards soon on the lack of momentum with price rolling over here: