Hot on the heels of the Actuaries Institute’s support of the Coalition’s superannuation package last week, financial advisers have now spoken-out against watering down the package, warning that implementing exemptions to the proposed superannuation caps would create perverse incentives to game the system and increase complexity. From The AFR:

Introducing exemptions for “life events”, such as divorce, inheritance or the receipt of a trust payment, would either create perverse incentives to behave dysfunctionally, or would require reams of regulations and red tape to ensure that the system remained robust and in line with its objectives. Or perhaps both.

Granting exemptions for inheritance would presumably favour the wealthy… Granting exemptions for divorce payments would provide a financial incentive for couples to split up in order to pump more money into super… Carving out farming families could lead to city-types who keep a few head of cattle or cultivate a few grapes on their hobby farm having an unfair advantage…

One irate adviser called the carve out suggestion “a total dog’s breakfast”, before later concluding it was “dumb, dumber and dumbest”.

Claire Mackay, of Quantum Financial, was more polite. “As a community I would like to think we are not encouraging divorce. But you can’t blame people looking at strategies to help them have a dignified retirement”…

As I keep arguing, there is absolutely no justification to water-down the Coalition’s superannuation package.

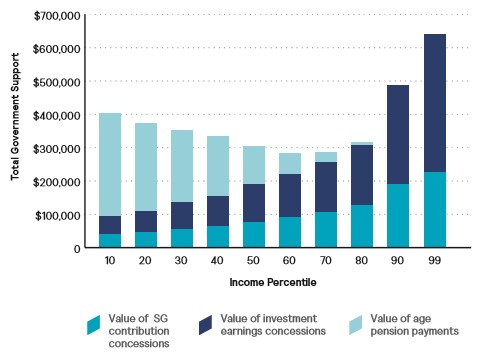

Under the existing arrangements, the top 10% and top 1% of income earners receive more government retirement support than the other 90% – a situation that is both highly inequitable and unsustainable from a budgetary perspective (see below chart):

The latest Household, Income and Labour Dynamics in Australia (HILDA) survey, released last week, also strongly supports the Coalition’s super reforms. As noted today by Professor Helen Hodgson:

The more concerning finding for policy makers is that wealth inequality has increased, and that superannuation holdings and investment properties are factors in this inequality. HILDA data shows that in 2014 the mean superannuation balance of the top 10% of people aged 50 to 69 was $991,268, up from $650,619 in 2002, compared to $210,798 in 2014 for the sixth to ninth decile and $13,719 for the bottom 50% (although a significant number of retirees in this age group do not have any superannuation balance).

There is a strong correlation between high superannuation balances, income and non-superannuation wealth. People in the top decile have access to higher levels of income to make higher levels of concessional contributions, and the ability to find the funds to make non-concessional contributions into a tax preferred investment environment.

As has been noted previously, the current superannuation system allows high income and high wealth individuals to over-accumulate in tax preferred superannuation, which increases wealth inequality as well as intergenerational inequality.

The Government proposals to restrict the level of contributions and to reduce the amount that can be retained in a tax free environment are important tools to address increasing levels of wealth inequality in our community.

Besides, as noted last month by David Ingles and Miranda Stewart from the Tax and Transfer Policy Institute, superannuation would remain ridiculously generous to the wealthy, even after the Coalition’s planned reforms:

Super fund withdrawals and investment income in pension phase became entirely tax-free in 2006 under changes made by Treasurer Peter Costello. It is widely recognised that this was a high water mark in the generosity of the superannuation tax system, unsustainable except for the mining boom with the “rivers of gold” flowing into Government coffers at the time.

The table below shows how extraordinarily generous the superannuation tax system will remain for better-off retirees, even after the imposition of the government’s proposed tax.

For example, a wage earner with a taxable income of $200,000 a year pays tax and Medicare levy totalling $67,947. Under the proposed reforms, a retiree with $200,000 income from super (implying capital of $4 million in the fund, at a 5% return), will pay $18,000 in tax. The retiree is still $49,947 ahead (see Table, column 5). Cries of double taxation cannot be sustained because the whole of the draw-down of the lump sum continues to be tax free – only the future investment income is taxed.

Again, there is little justification for watering-down the Coalition’s superannuation package, whose wealthy constituents will continue to receive a very good deal under these reforms.