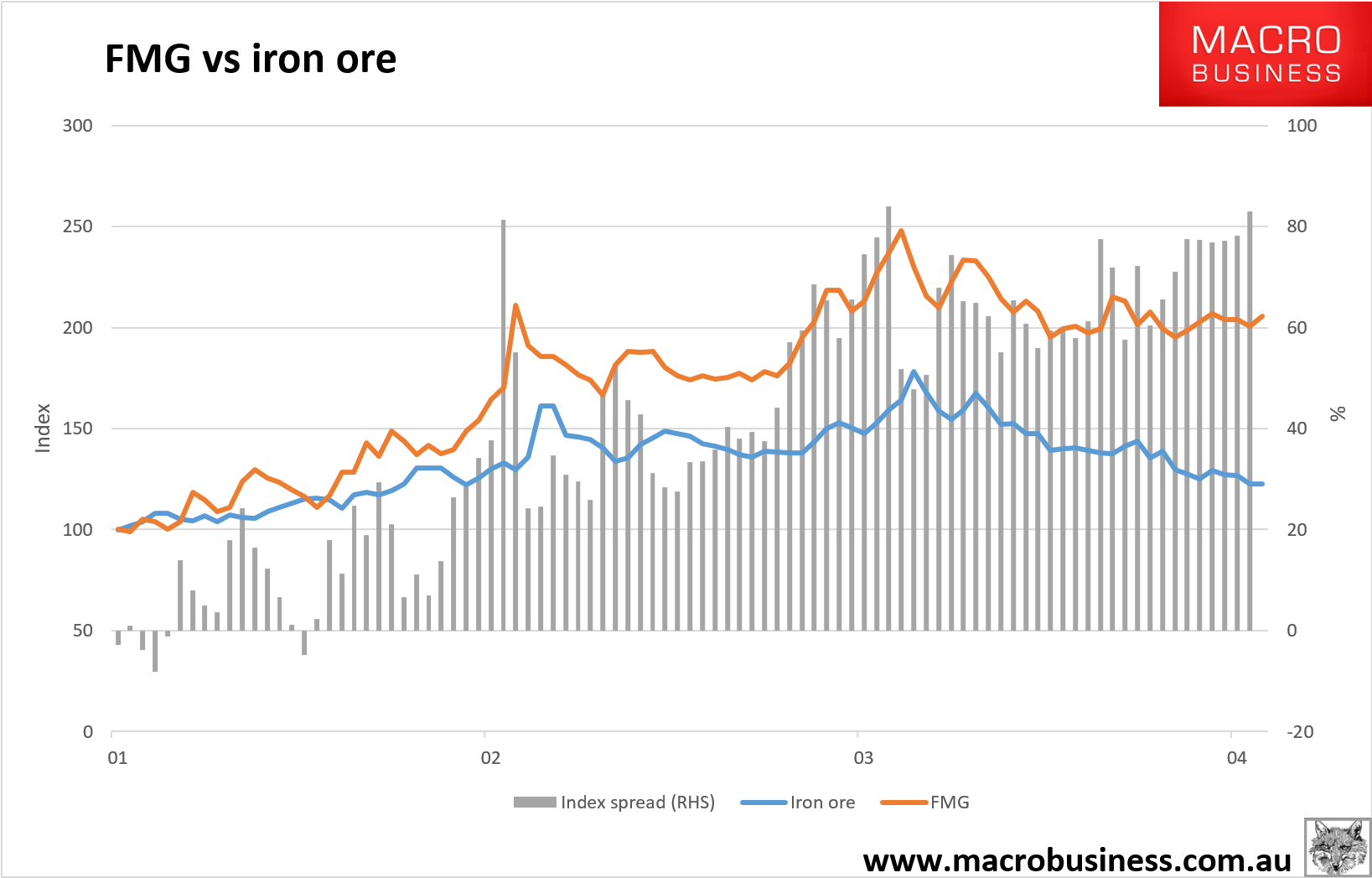

Here’s the chart:

Since the beginning of the little Chinese bubble in iron ore, FMG has re-rated upwards and is no longer trading in line with the price of its only product.

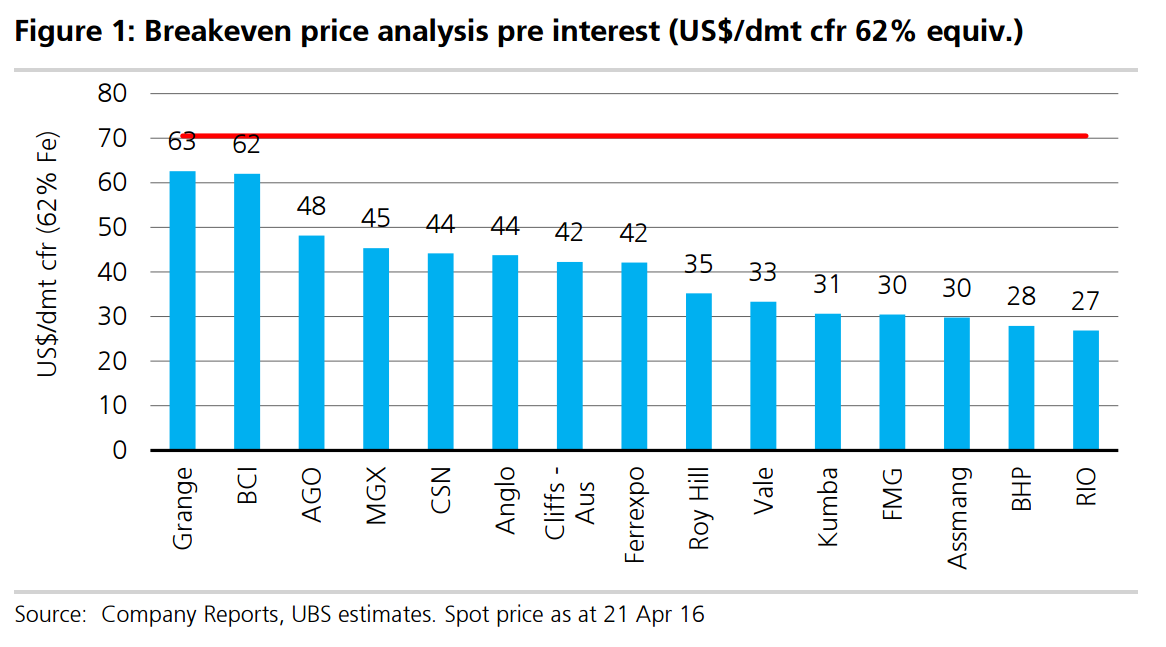

In that time it has paid down some debt and it signed its JV with Vale which will keep its more expensive volumes in production for longer. But as we head into H2 and the balance sheet shakeout for iron ore resumes, FMG is still the emerging marginal cost producer of magnitude as non-traditionals drop out again. In fact, each major drop in the iron price deck has stopped at or just below FMG’s all-in costs which are now at $30 according to UBS (Vale’ costs are about to fall a lot more):

Advertisement