South Korea is planning a Won20tn ($17bn) stimulus package including a Won10tn supplementary budget to boost sluggish economic growth and cushion risks from the UK’s decision to leave the EU.

The government has faced growing calls for stimulus measures, with the corporate restructuring in the shipbuilding and shipping industries expected to spark many lay-offs and the Brexit referendum increasing market volatility this week.

“Unrest in global financial markets has been growing from Brexit,” President Park Geun-hye told economic officials and lawmakers on Tuesday. “Uncertainties over the Chinese economy and geopolitical risks from North Korea are still pressuring our economy.”

BofAML sums it up:

Advertisement

If you are going to panic, panic early – Brexit is here. And so is risk-off sentiment. Our US economists now call for the US Fed funds rate to be lower for longer with the next forecast rate hike pushed out to December this year rather than in September. We suspect that overall global policy is now likely to be easier for longer, with even more unconventional policy possibly more palatable (helicopter money, anyone?). Our views continue to be the same as they were last week.

We also think that Brexit has now possibly opened up more uncertainty about the European Union project and that the already beaten down Asian and EM equity markets could receive asset allocation flows from Europe.

As the move for Britain to leave the EU was largely unexpected (Oddschecker average probability of BREXIT implied from betting odds was only 23% before the referendum day), a majority of investors were caught off-guard. Some of the high frequency sentiment indicators like VIX Index, put/call volume ratio, trading in the S&P500 Index versus its components, etc., are in panic now.

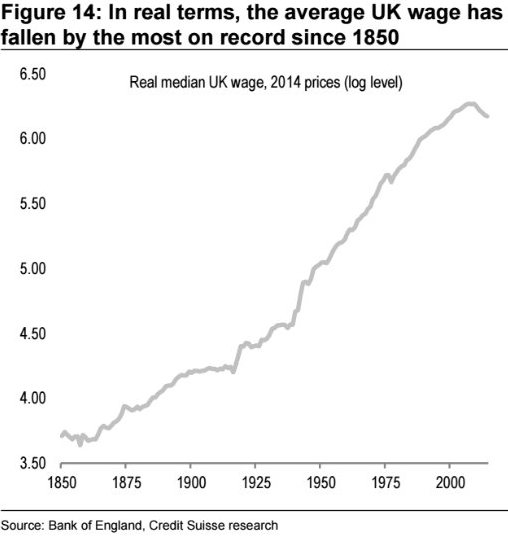

We reiterate our views on the potential deeper message from Brexit. As Figure 4 shows, the past 30 years have seen a silent collaboration between the EM middle classes and global plutonomists, at the expense of the bottom 50% of developed market citizens.

While globalization, immigration and the free market have strong support from the winners of these themes – the plutonomists and the highly educated, in our view they seem to have underestimated the frustration of developed market middle and working classes. We think Brexit could just be the first surprise in a re-calibration of the world away from globalization towards more inward looking policymaking. Away from Wall Street and more towards Main Street. Away from financial asset reflation to more income support and wage inflation. We suspect that few will pay attention to these tectonic shifts – it will require more Brexit-type surprises for the message to sink in.

Bottom-line: It is a bit too late to panic.

That’s a little contradictory, no? If it’ll take more Brexit events to change things then it ain’t too late to panic!

That’s where I’m at. Brexit is not over. Brexit is not the problem. Brexit is only the first appearance of more severe symptoms of an underlying disease that is getting worse and will deteriorate further with any form of stimulus that supports markets over income redistribution. But, any form of income redistribution will hit profits and asset prices! Credit Suisse explains:

The main explanation as we see it is the profit share. This is a global phenomenon leading to political impacts in the UK and to the extent a political reaction is necessary, as we suspect it is, this will be terrible news for financial assets, including credit.

The explanation is not confined to “Brexit” but in our view can be applied to the popularity of Donald Trump as well; we think that understanding what is driving these events is central to understanding their implications. We see them as symptoms, essentially.

Our view is that we are finally seeing the political effects of the profit share having been unsustainably high for too long. It now seems at least possible that it now needs to come down as a political imperative. Driven to a large extent by globalization, this high profit share has concentrated such income gains as there have been in recent years on capital at the expense of labour, with the political results we are seeing. Chief among those political effects is pushback against globalization itself wherever it presents itself as a target.

One reason current political events are such a shock is because two-party political systems with both parties broadly in favour of globalization have provided good cover, preventing that from happening…

…we come back to the underlying profits driver. Attempts to defuse the issues it raises will produce policies which reverse some of the pro free trade and pro-profits policies of recent decades. We do not think that credit markets, after the recovery from the opportunity which presented itself very early on Friday morning, provide adequate compensation for the global political sea change in the long term or for the uncertainty which the UK result opens in the near term. Enough of this uncertainty is of a practical day-to-day variety (what will German car manufacturers’ UK sales do over the next six months, for example) to have an impact, in our view.

Advertisement

Thus now is an ideal time to panic. Before this conundrum implodes upon itself in the next round of European elections. In this sense the quaint faith of markets in their elite policy champions is everyone’s best friend. Blind to the underlying malady and enslaved to the twitches of policy-makers, markets aren’t going to price this in a straight line down. That provides ample opportunity of position in advance: selling the rallies, especially in banks, buying bonds and gold miners on the dips, and exiting the Australian dollar.

In the end, there really is only one cure for the disease that Brexit has exposed that does not itself kill the patient. QE for the people will be needed. Helicopter money to make everyone feel richer and inflate away their debts.

But you can’t just begin that kind of debt jubilee without a crisis. First we’ll need to see much more market wreckage.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.