Report: Abbott/Turnbull worst post-war economic managers

The Australia Institute (TAI) has released a new report, entitled “Jobs and Growth… And a Few Hard Numbers: A Scorecard on Economic Policy and Economic Performance”, which attempts to benchmark the economic performance of Australia’s post-war prime ministers, namely:

The report assesses performance based on a dozen common statistical indicators:

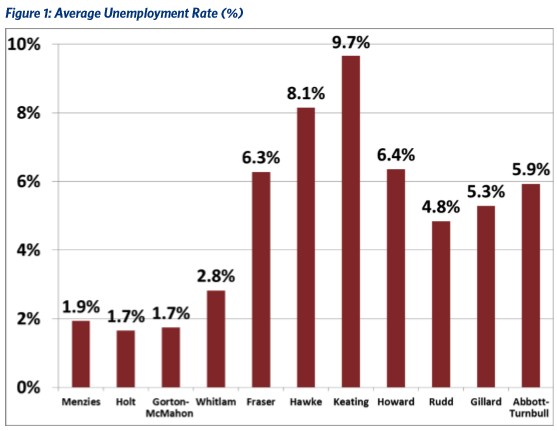

- Average unemployment rate (not working as share of official labour force).

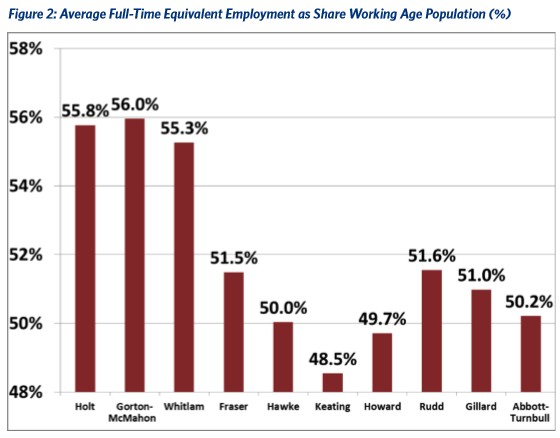

- Average employment rate (full-time equivalent jobs as share of working age population).

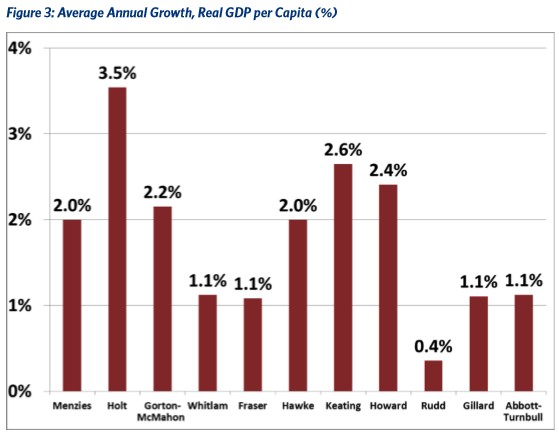

- Average annual real GDP growth (per capita).

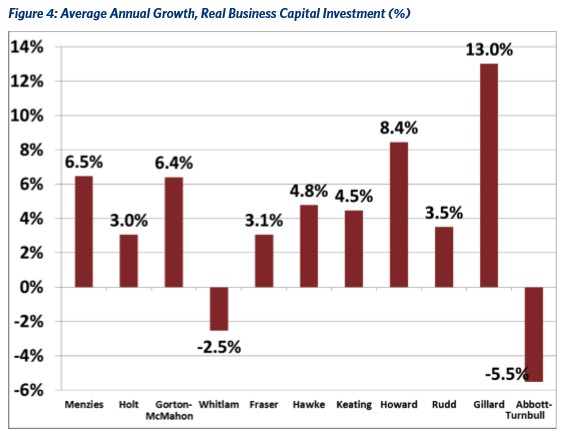

- Average annual growth, real private business capital investment.

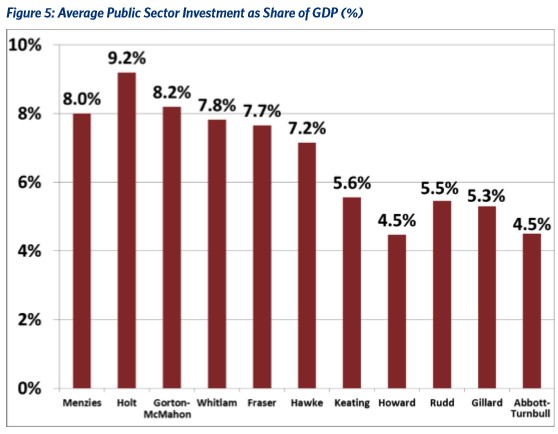

- Average public sector capital investment (as a share of GDP).

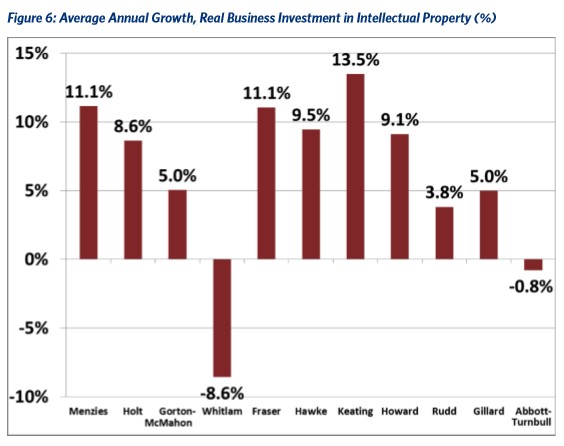

- Average annual growth, real business intellectual property investment.

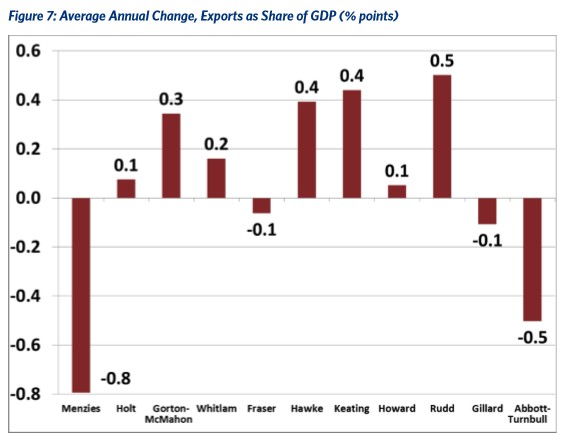

- Average annual change, exports (value, measured as a share of GDP).

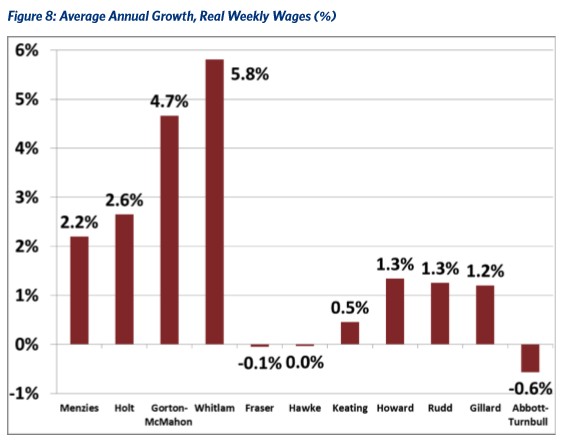

- Average annual growth, real weekly wages.

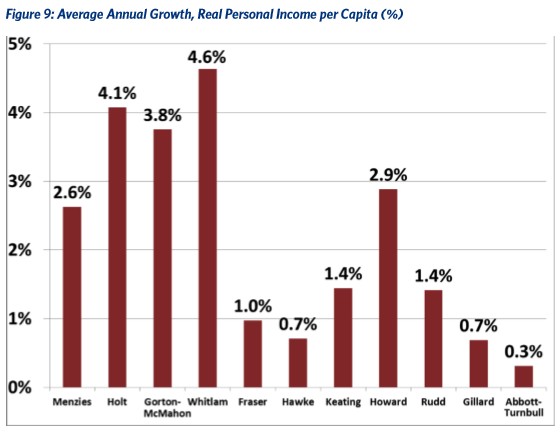

- Average annual growth, real personal incomes (per capita).

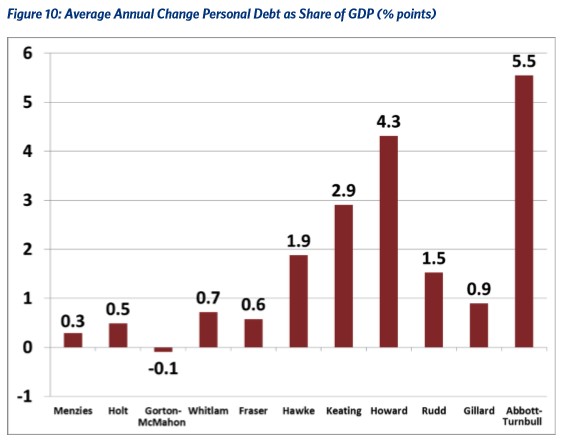

- Average annual change, personal debt (as a share of GDP).

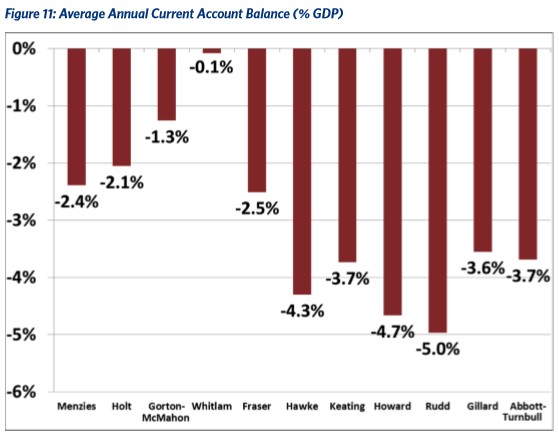

- Average current account balance (as a share of GDP).

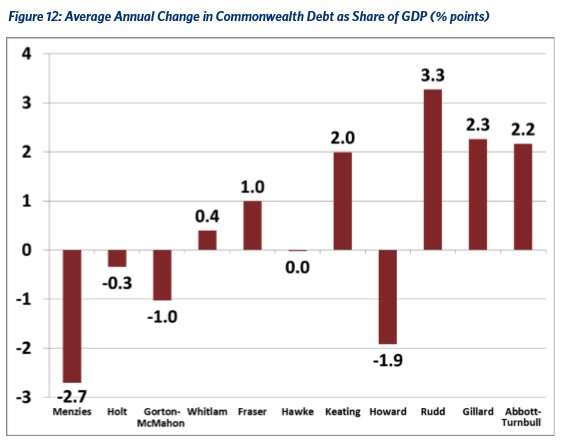

- Average annual change, Commonwealth government debt (as a share of GDP).

The results for each measure are summarised below:

According to the above indicators, the TAI ranks the current Coalition Government as the weakest in the post-war era:

Across all twelve of the indicators, Australia’s economic performance under the current government has ranked well within the bottom half of the eleven postwar Prime Ministerships considered in the analysis. In four cases, the current government ranked last of the eleven governments, and in three more cases it ranked or tied for second-last. Considering all the indicators, the tenure of this government qualifies as the weakest of any government in Australia’s entire postwar economic history.

The report then concludes with the following statement:

During election campaigns, competing politicians tend to exaggerate the potential impact their policies (and their opponents’) are likely to have on the national economy. In reality, Australia’s economy is dependent more on the decisions of private actors (including businesses, consumers, and foreign customers) than on government. It would be folly to ascribe full credit for good economic times to the government that happened to be in power during those years – and by the same token, to blame a government for negative economic events which were clearly beyond its control. (The economic fallout in Australia from the GFC is an obvious example of that latter form of misattribution.)

Politicians on all sides, therefore, should approach economic performance indicators with caution and humility. Government policies clearly have the capacity to influence the broader economic trajectory, for better or worse. But those effects take time, and are muted or even overwhelmed by other developments.

In the context of the current election, the present government’s claims to superior “economic management,” rooted in the alignment of its policies with the preferences of the business community and high-income households, must be considered with particular skepticism. By most of the twelve indicators presented here, national economic performance has clearly deteriorated during its tenure. Again, this deterioration cannot be attributed solely to the actions of the government itself. But it is still far-fetched for the present government to claim “credit” for an economic record that, by concrete statistical measures, is quite poor.

Looking past the election, there are numerous indicators that Australia’s economic performance is likely to get worse, not better, in the absence of strong countervailing measures. Significant risk factors in the economic outlook include:

• A dramatic and continuing contraction in business capital spending, usually the most important driver of economic growth. Recent ABS data indicate that private business investment will decline another 15 percent in 2016.10

• A continuing decline in the value of exports relative to GDP. GDP statistics for the March 2016 quarter reported a decline in the aggregate value of exports (down at an annualized rate of 3 percent), despite an increase in the physical quantity of exports. Exports consequently fell to their lowest share of GDP (18.77 percent) since the GFC.

• Swelling current account deficits reached over 5 percent of GDP (one of the highest levels in postwar history) in the second half of 2015.12 These deficits reflect the falling value of Australian exports, and a widening trade deficit — and translate into an inexorable increase in foreign debt. Financial analysts have expressed concern about the stability of Australia’s foreign debt (especially in the event of a housing market downturn, sharp drop in the value of the Australian dollar, or other shocks).

• Steady increases in consumer debt (now equal to 130 percent of GDP) are being fueled by soaring real estate prices. At the same time, concerns are growing over the quality and stability of Australian mortgage debt, including the growing preponderance of interest-only mortgages.

• Unprecedented stagnation in wages and prices across the broader economy. In fact, both consumer prices and overall output prices declined in the March quarter of 2016. Nominal wage increases are near zero. If deflation becomes entrenched, the impacts on business and consumer expectations, spending, and debt stability could be severe.

Taken together, these negative indicators suggest that Australia’s economy is headed into very challenging times. Invoking vague concepts like “confidence” and “leadership” is hardly a convincing response to those challenges…

Fair enough. In defence of the Coalition, whoever was in Government over the past three years would have struggled given the collapse in commodity prices and mining investment, which has weighed heavily on many of the measures presented above.

A bigger issue in my view is that the Coalition has no plan for the future other than ongoing support of the bubble and Australia’s rent-seeker economy.